Downloaded 10 times

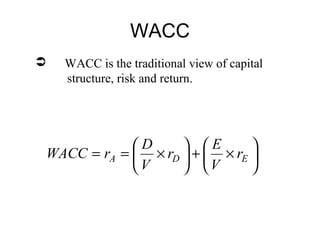

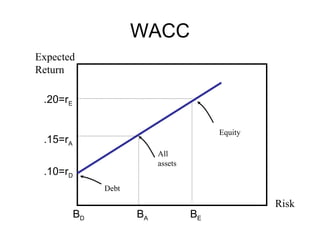

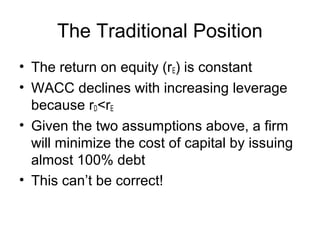

The document discusses capital structure and the tradeoffs between debt and equity financing. It summarizes Modigliani and Miller's seminal work which established that in a perfect capital market without taxes, a firm's value is independent of its capital structure. Specifically, M&M Proposition 1 states that splitting cash flows between debt and equity holders does not change total firm value. Proposition 2 states that the expected return of equity increases with leverage in a way that exactly offsets the reduced risk of debt.