Download as PDF, PPTX

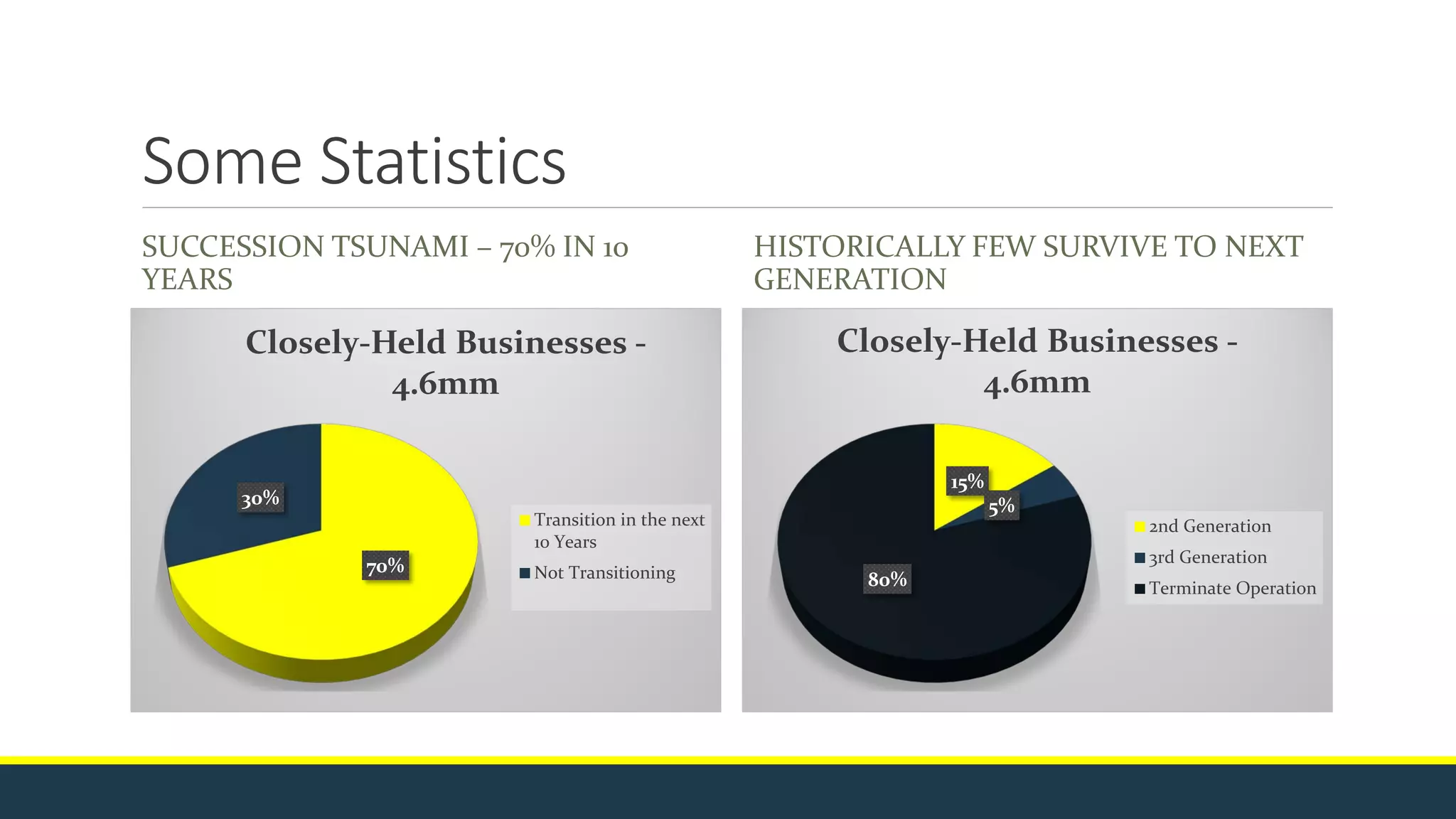

The document discusses business succession planning, focusing on the Employee Stock Ownership Plan (ESOP) model as a tax-efficient mechanism for transferring ownership. It highlights the importance of strategic planning for ownership transfer, management succession, and legacy planning and provides statistics on the significant impact of not having a succession plan. Additionally, it explains the advantages of ESOPs, including employee involvement in company profits and the potential for improved business growth.

![[DIY] Employee Stock Options the right way](https://cdn.slidesharecdn.com/ss_thumbnails/diymakingesopsmatter-190314055510-thumbnail.jpg?width=640&height=640&fit=bounds)