Downloaded 68 times

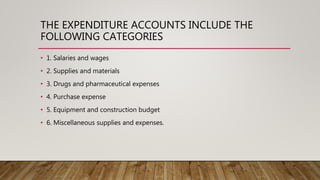

Budget preparation and implementation are important tasks for any hospital pharmacy department. A budget involves developing a financial plan for the upcoming year that takes into account factors like maintenance, development, and strategic planning. It allows hospital administration and departments to comprehensively review services and compare actual results to standards. There are different types of budgets based on duration and division, including short term (2 years), long term (5-10 years), income accounts, expenditure accounts, and capital investment requests. Preparing the budget involves estimating income from things like prescriptions and costs for categories such as salaries, supplies, drugs, equipment, and miscellaneous expenses. Implementation of the approved budget considers requirements, funding availability, item utility, costs, and quantities.