HOSPITALAND COMMUNITY PHARMACY

PresentBy

M Naveenkumar

M Pharm-1st SEM.

Pharmacy Practice

KMCH College of Pharmacy

BUDGET PREPARATION AND IMPLEMENTATION

2.

BUGDET PREPARATION:

Budget:

Budget isdescribed as an instrumental through which hospital administration, management

at the department levels and the governing bodies can review the hospital services in relationship

to the prepared plan in a comprehensive and integrated from expressed in financial terms.

Objectives:

Development of standards

Comprehensive of actual results with standards

Identification of deviation or fluctuation

Analysis of deviation

The responsible person will use the budget

To monitor the hospital financial activities

Estimate the cost of completing objectives identified in proposal

3.

Functions:

To regulate hospitalfinancial activities

For preparing and filling tenders

Smooth the departmental functions

Estimate to completing objectives

Length

Of

Budget

Period

Long Term

Budget

Current

Budget

Short

term

Budget

Classification:

Income Account:

Income iscalculated by maintaining daily/weekly/monthly/annual records.

The average total sum up represents income of the department from various sources.

Pharmacy department or accounts department maintains daily, weekly, monthly & annual

cost of the pharmaceutical issued to the patient services.

Hospital Income further depends upon types of patients ;

No of Prescription

No of Prescription dispensed by each pharmacist

Hours of work put in prescription volume per hour of service

Medication cost per patient day

Average drug cost for Physician visit

Average salary cost for prescription

Average supply cost per requisition

6.

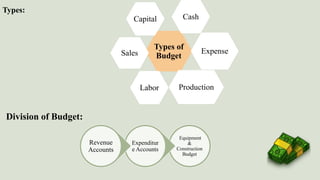

Expenditure Accounts:

Expenditure

Accounts

Salaries &

Wages

Supplies&

Materials

Drugs &

Pharmaceuticals

Purchase

Expense

Miscellaneous

Fixed Expenses is to Sub categorized:

Administrative Expenses

Professional Care of the patients

Out patients & Emergency Expenses

Emergency Expenses

7.

Salaries & Wages:

Salariesand wages include complete break up of all salaries & wages paid to permanent and

temporary staff(Full time & Part time)

The chart should be prepared in tabular form so as to give an overall view at a glance

The chief Pharmacist/administrator should sub divided the staff into three important categories

like administration, professional and non professional staff.

The total of all three expenses constituents the anticipated salary and wages, expenditure for

next year.

Supplies & Materials:

Chief Pharmacist or the responsible person should prepare the financial statement regarding

the requirement of amount in rupees for supplies and materials with the help of the latest

financial budget.

Necessary to show the actual cost of the materials.

8.

Drugs & Pharmaceuticals:

DrugsDispensed by prescriptions

Drugs used in the outpatients and emergency departments

Charges for the latter are submitted to the respective departments

Purchase Expenses:

It includes the cost of prescriptions purchased from an outside Pharmacy.

Miscellaneous:

Miscellaneous Supplies and expenses include glassware, labels, stationary, uniform , repair

and maintenance.

In patients, there should be a close liaison between the chief Pharmacist and accounts

department for maintenance of statistical data.

9.

Equipment & ConstructionBudget:

It requires Major monetary funds

Budget for immediate arrangements of a new model equipment

Budget for remodeling and replacement of equipment.

Construction of Building

Actual Fund Position:

SuccessfulImplementation of the budget will depend on the financial position of

a firm.

The master budget will give insight into the plan.

A cash budget will help to know the cash plan for a specific period.

Overall, all types of budgets are studied at the micro level to implement the

planned budget.

12.

Utility of Particularitem:

This depends upon materials used and expressed in qualities where as the materials purchase budget is

expressed in both ways is quantitative and financial.

This helps in scheduling the purchase of materials to produce a given volume of output during a particular

period.

Study of the cost required to manufacture/purchase a particular product is very important in budget planning.

Cost includes direct costs and indirect costs.it is the production and non production costs required to

manufacture a particular product.

Cost of Products:

13.

Quality of products:

Effectiveinventory management is needed for the successful implementation of a

budget plan.

To avoid stock out and over stock, effective inventory control is needed, as huge

amount of capital is invested in inventory.