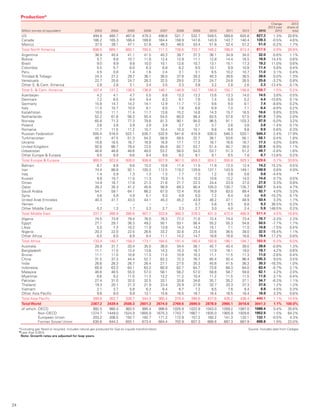

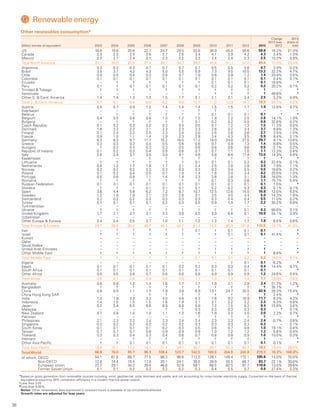

Downloaded 10 times

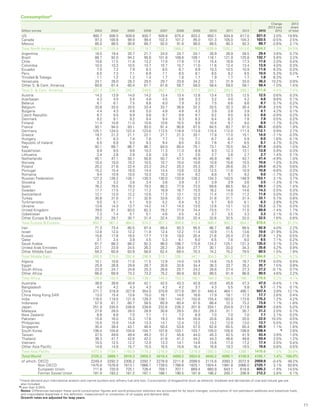

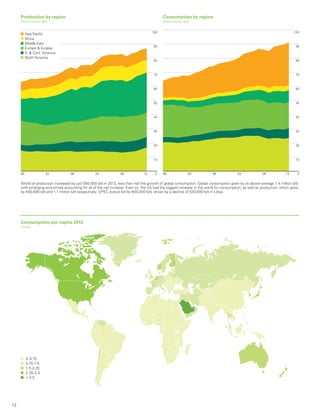

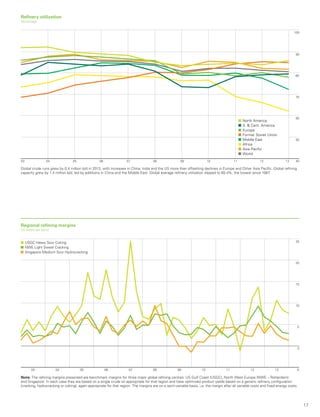

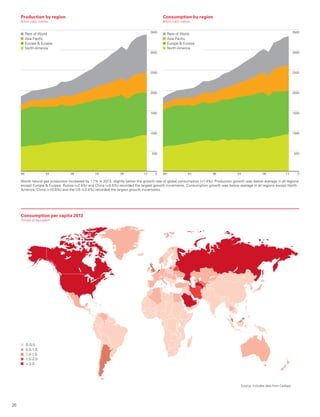

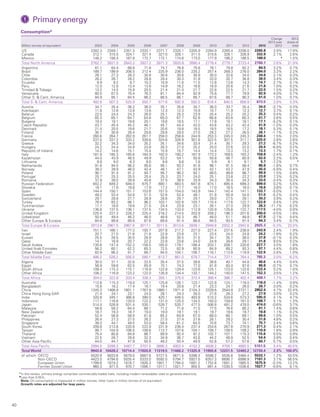

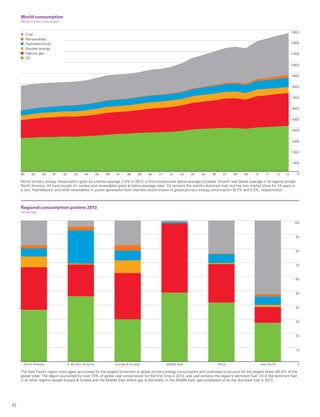

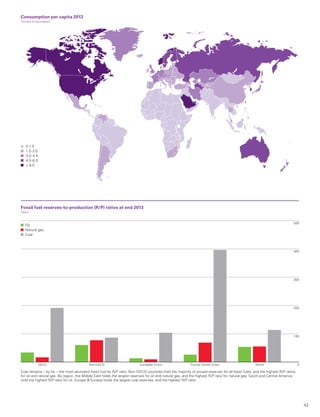

Global energy consumption grew at an accelerated rate in 2013 despite stagnant economic growth. Consumption increased for all fuels except nuclear power and reached record levels. Emerging economies accounted for 80% of growth, led by China, but growth was below the 10-year average in these countries. The US saw the largest increase in oil production in the world and offset supply disruptions elsewhere. Natural gas consumption growth was below average globally except in North America. Coal consumption grew the fastest of the fossil fuels.