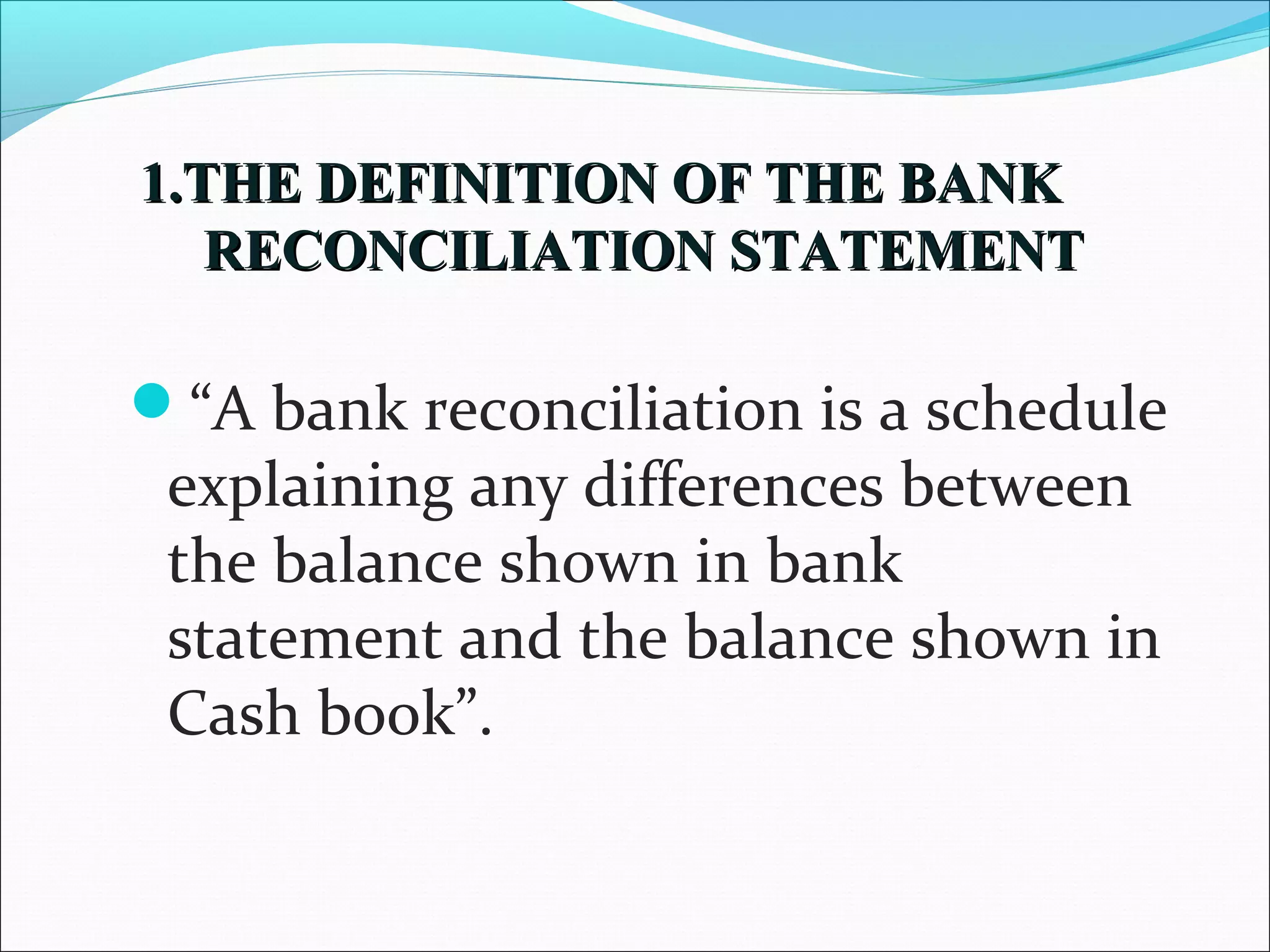

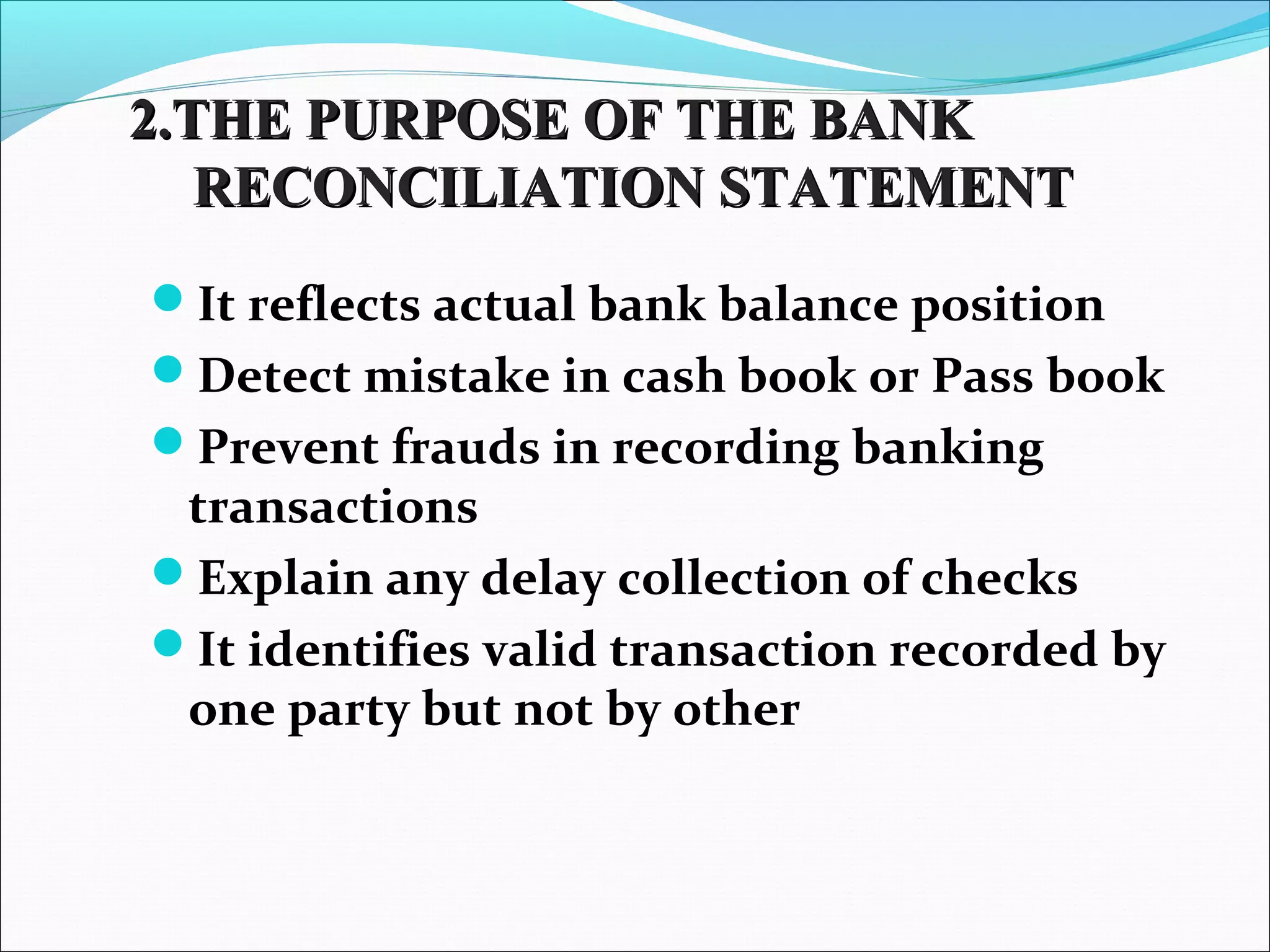

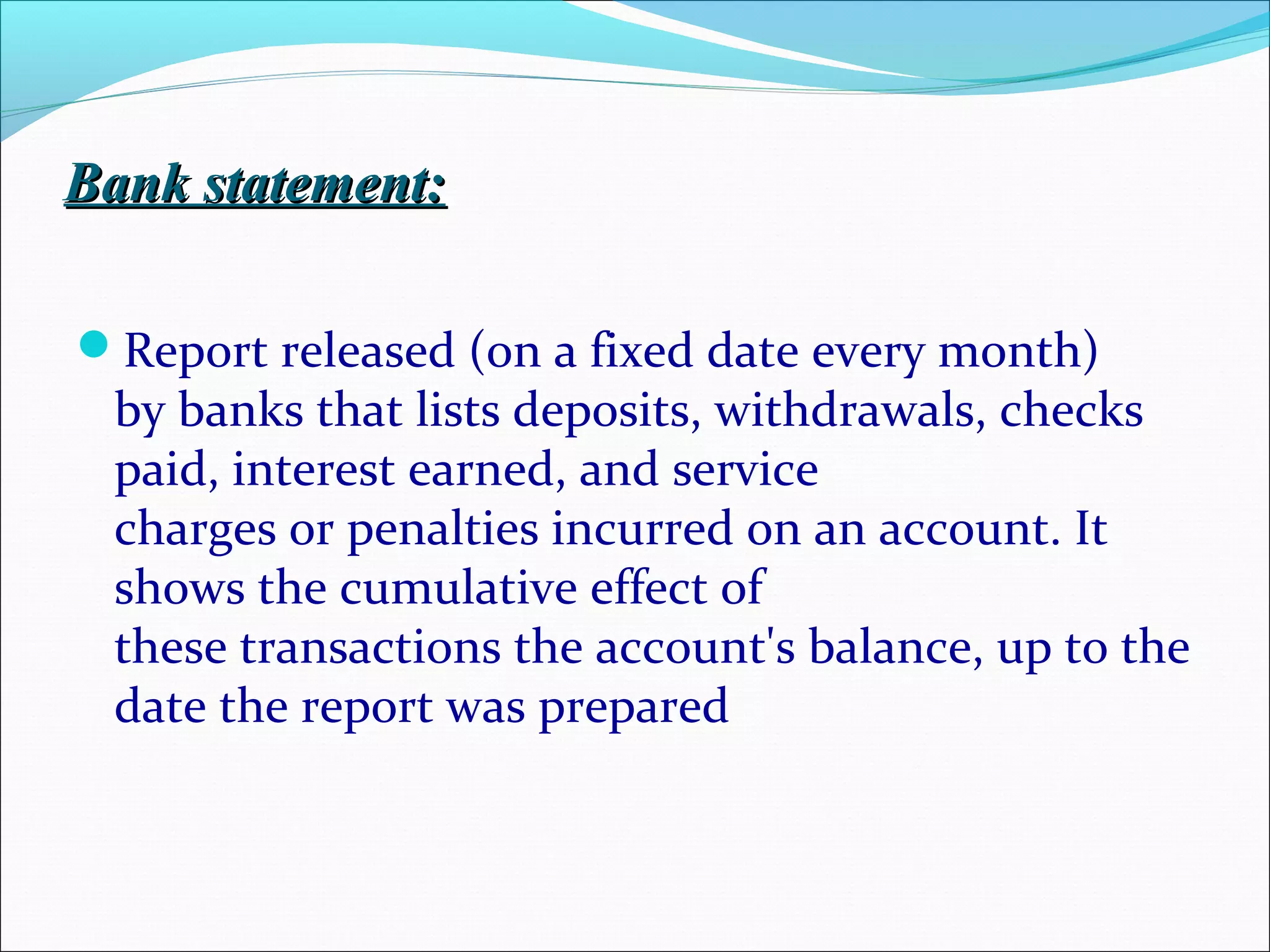

The document discusses bank reconciliation statements. It defines a bank reconciliation statement as a schedule that explains any differences between the balance shown in a bank statement and the balance shown in a cash book. The purpose of a bank reconciliation statement is to reflect the actual bank balance, detect errors, prevent fraud, explain delays in transactions, and identify transactions recorded by one party but not the other. It also discusses the nature of cash books and bank statements, and reasons for differences between the two such as unpresented cheques, uncredited deposits, service charges, dishonored cheques, interest, and miscellaneous charges.