Downloaded 64 times

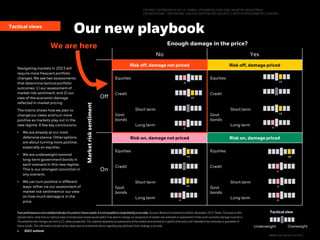

The document discusses a new investment playbook for 2023 in light of a new macroeconomic regime characterized by greater volatility and inflation. Key points: - Central banks are deliberately causing recessions through aggressive rate hikes to reduce inflation, making recession likely. However, inflation will remain above targets. - The first investment theme is "pricing the damage," as what matters most is how much economic damage is already reflected in market prices. Equity valuations do not yet reflect expected damage. - The second theme is "rethinking bonds," as this regime calls for higher yields. Short-term government bonds and mortgage securities are favored for income. - The third theme is "living with inflation," as