This document provides instructions for completing Arizona's 2003 resident personal income tax return (Form 140). It addresses who must file, filing dates and penalties, residency requirements, income exclusions, deductions, credits, and other general questions. Specifically, it notes that:

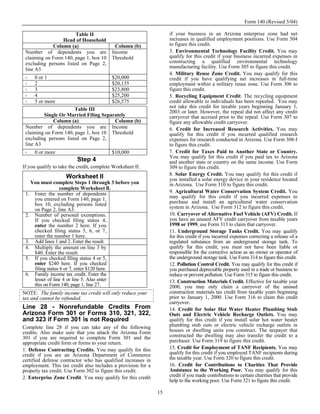

1. Taxpayers must file if their Arizona taxable income is $50,000 or more, regardless of filing status, or if they are making adjustments to income, itemizing deductions, or claiming certain tax credits.

2. The filing deadline is April 15, 2004 for calendar year returns. Late filing or payment penalties may apply. Taxpayers can request an extension but taxes must still be paid by the original deadline to avoid penalties.

3.