Downloaded 207 times

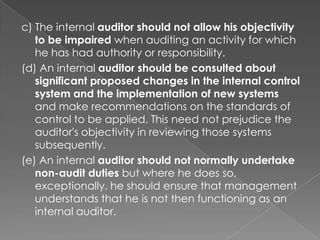

An internal audit is conducted by internal auditors employed by an organization to evaluate its internal controls, risk management, governance processes, and ensure compliance with laws and regulations. The internal audit function is independent and provides assurance and consulting services to add value and improve operations, financial reporting, and asset protection. Internal auditors plan, control, and document their work to obtain sufficient evidence and communicate findings and recommendations to management.