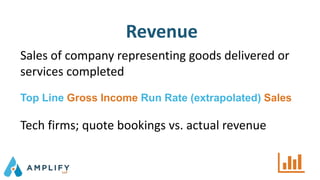

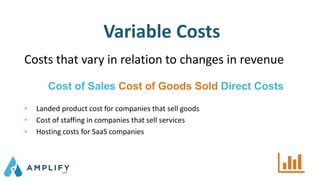

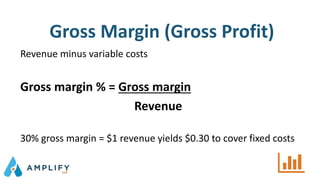

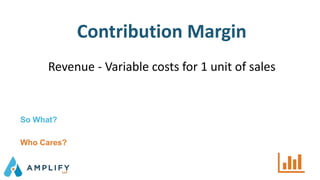

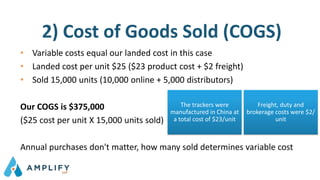

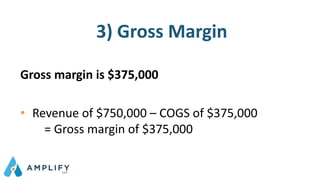

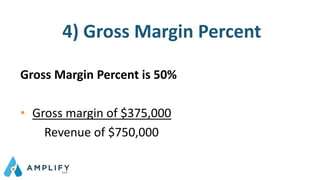

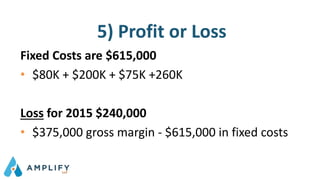

This document provides an overview of key financial concepts and metrics for entrepreneurs. It discusses common mistakes entrepreneurs make related to finances, including a lack of proper documentation and inappropriate draws. The agenda includes reviewing financial terms, metrics like income statements and balance sheets, and accessing financing. Key financial metrics covered are income statements, gross margin, contribution margin, net income, breakeven analysis, and balance sheet basics. Accessing financing through traditional debt is discussed alongside factors like debt ratios, while venture capital is presented as trading equity for funding to meet milestones.