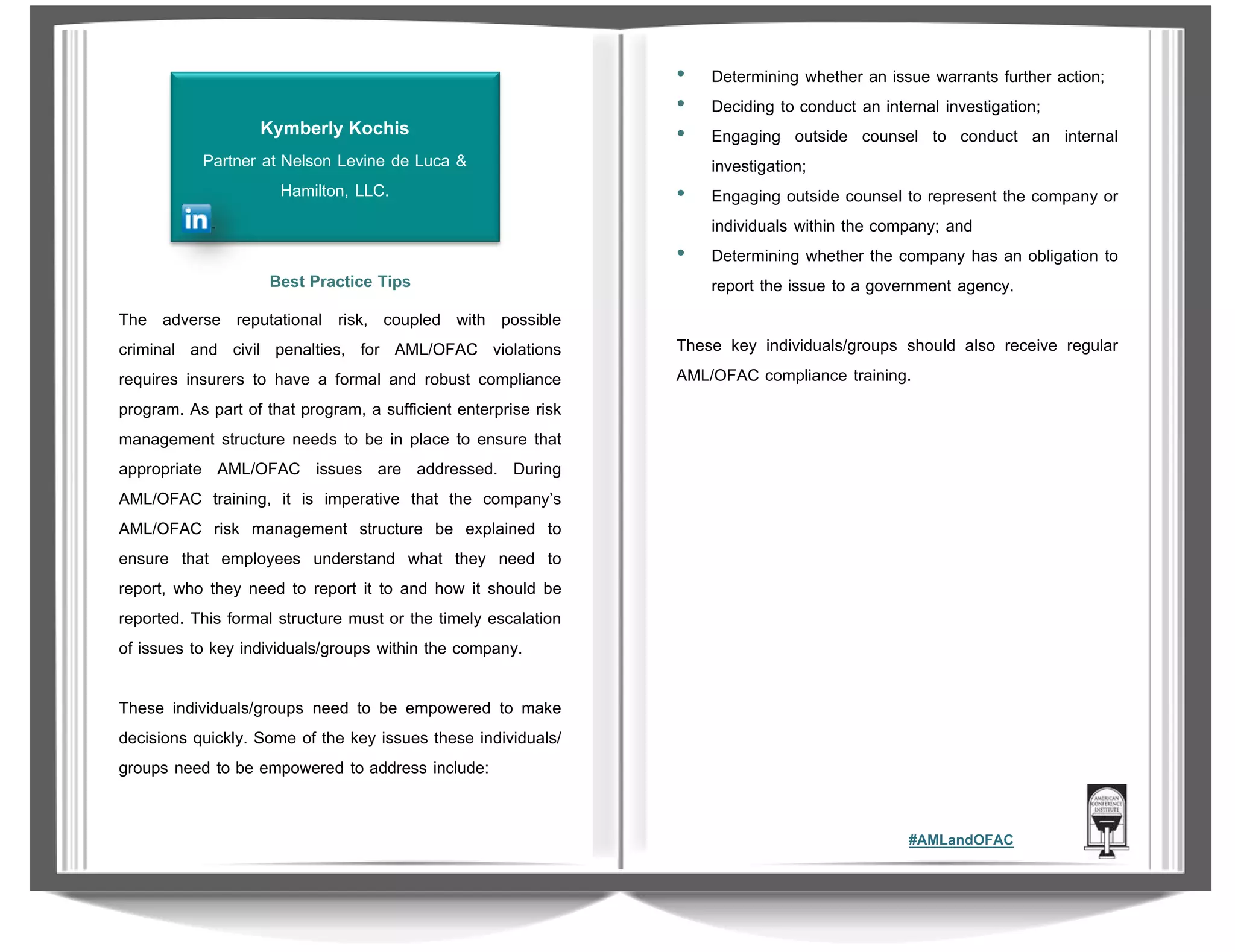

This document contains best practice tips from several experts on anti-money laundering (AML) and sanctions compliance. Some of the key tips discussed include developing a standardized framework for assessing risks and controls across different business units; tailoring compliance training to specific roles and business areas; understanding business operations in depth to design effective screening processes; and clearly communicating compliance risks and implications to senior management.