Download as PDF, PPTX

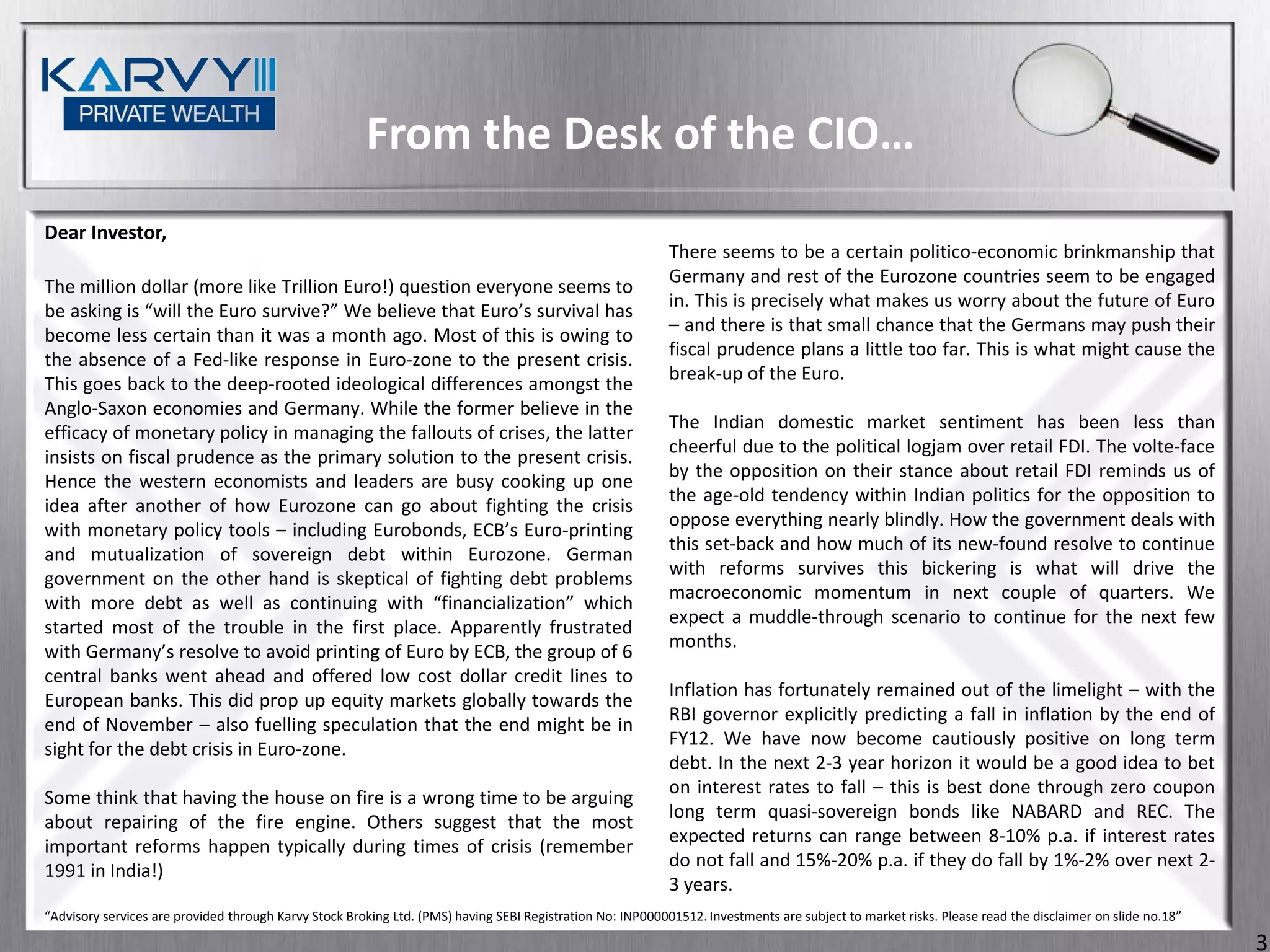

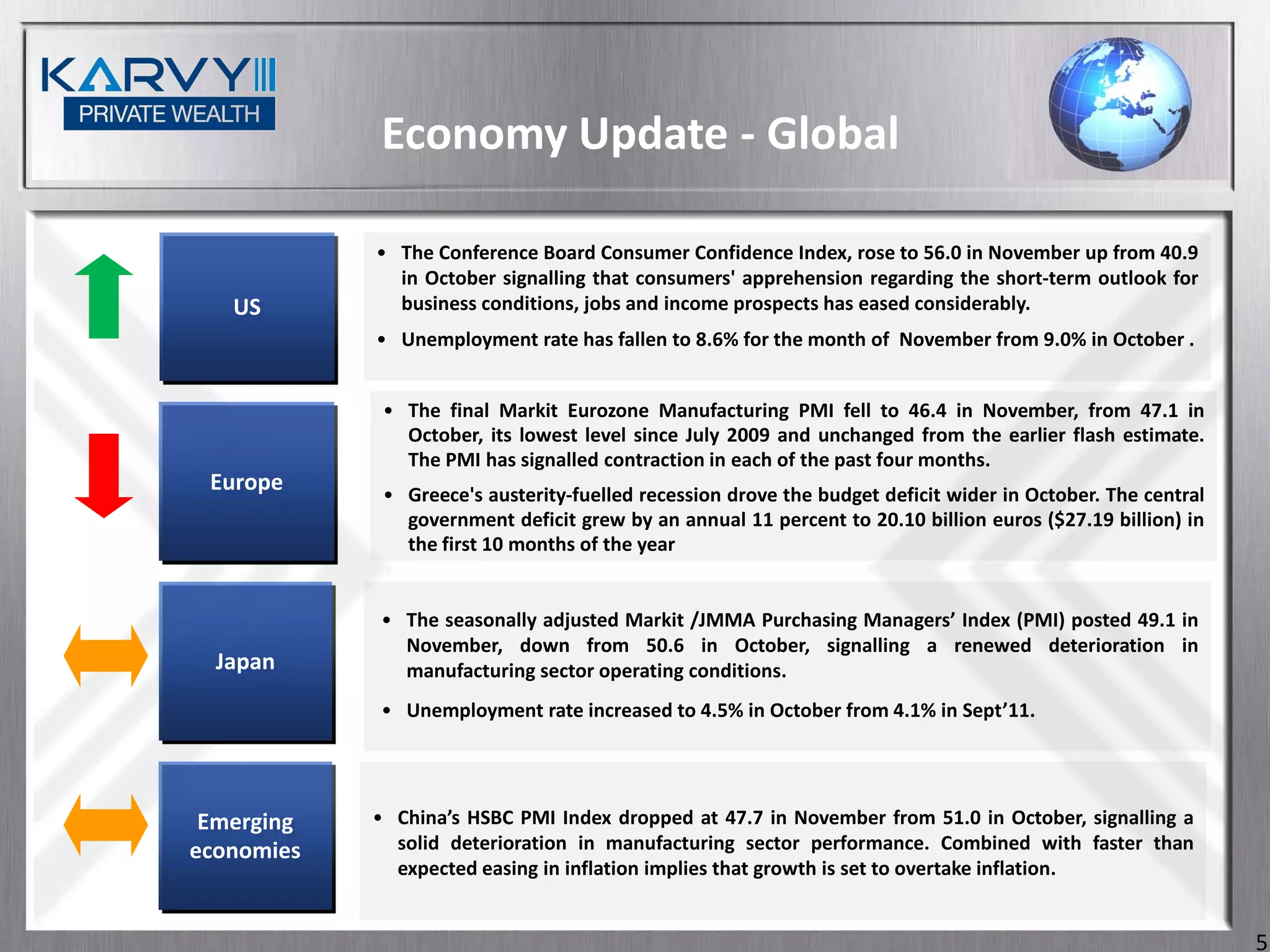

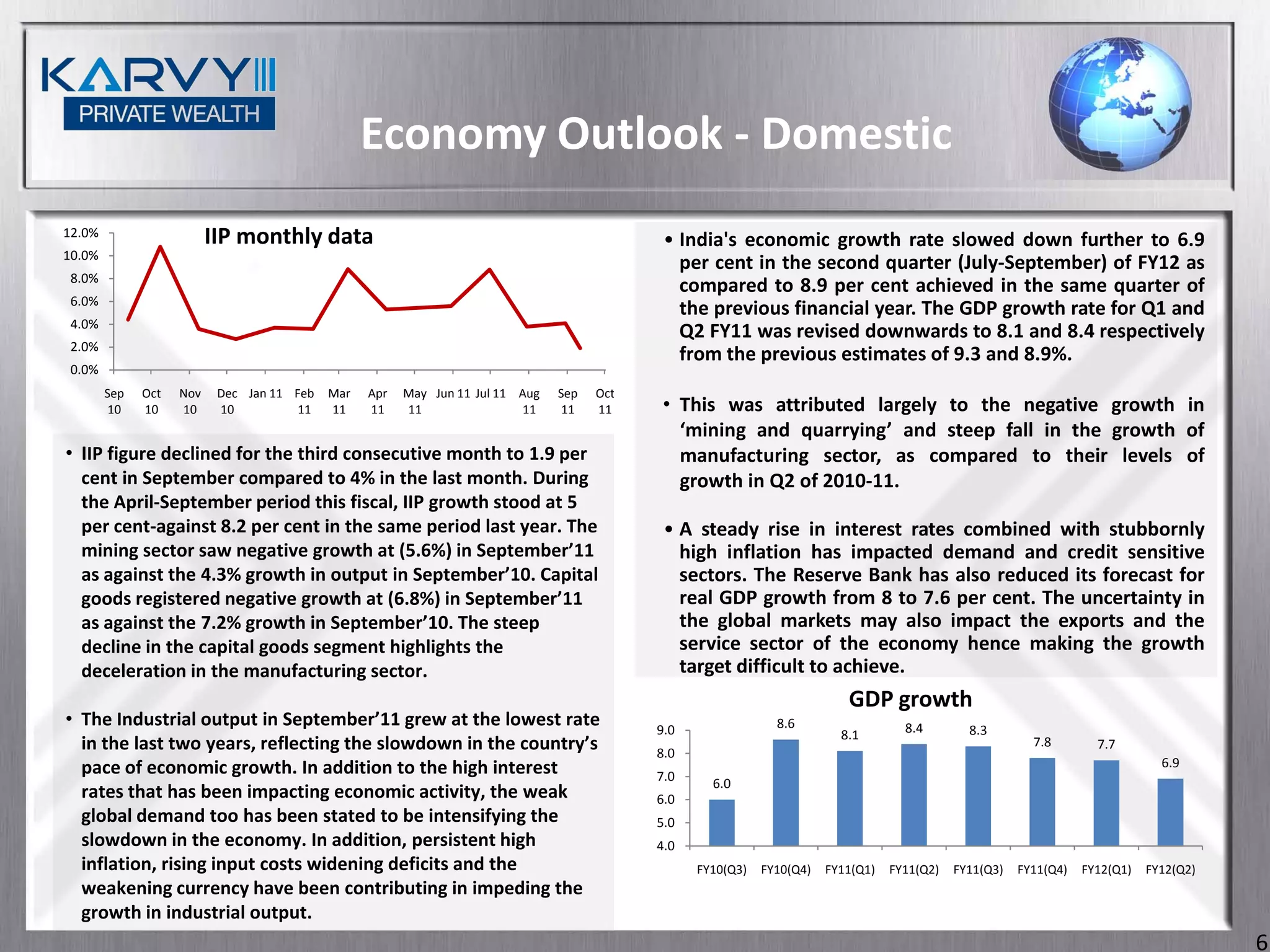

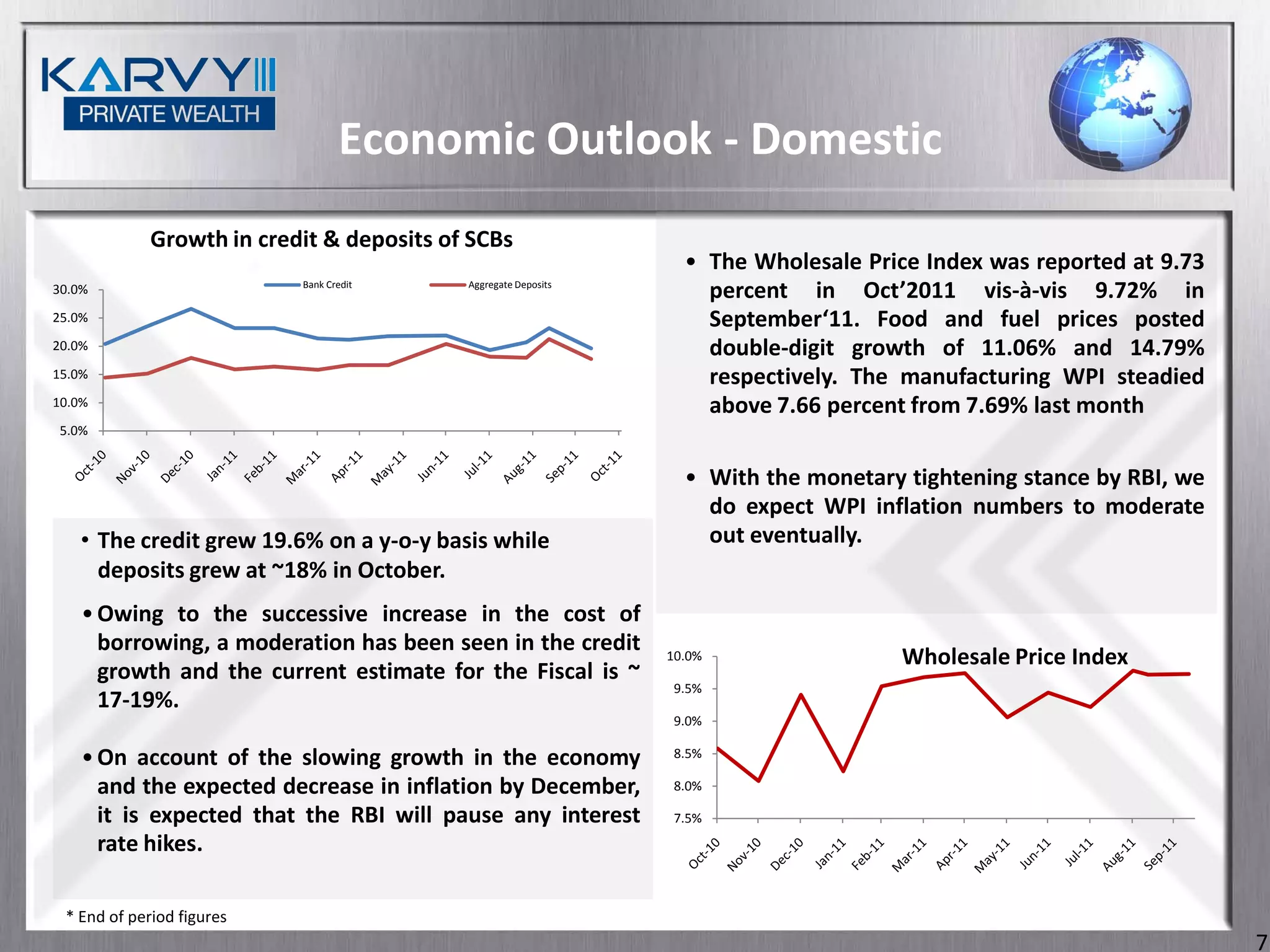

The document provides an economic update and outlook for December 2011. It discusses the ongoing debt crisis in the Eurozone and whether the Euro will survive. It notes the ideological differences between Germany and other countries in their approaches to dealing with the crisis. Domestically, it comments on the reversal in stance by the Indian opposition on retail FDI and the potential impact on economic momentum. Inflation is expected to fall by the end of the fiscal year. The outlook is cautiously positive on long-term debt as interest rates may fall over the next 2-3 years.