Download to read offline

![DISCLAIMER

Karvy Investment Advisory Services Limited [KIASL] is a SEBI registered Investment Advisor and provides advisory services. The information in this newsletter has been prepared by KIASL based on information obtained from

public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed and the same are subject to change without any notice. This newsletter and

information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe to the securities mentioned. The securities discussed and opinions

expressed in this newsletter may not be taken in substitution for the exercise of independent judgment by any recipient as the same may not be suitable for all investors, who must make their own investment decisions, based on

their own investment objectives, financial positions and needs of specific recipient. The information given in this document is for guidance only. Final investment decisions have to be made by the recipients themselves after

independent evaluation of the investment risk. Recipients are advised to consult their respective tax advisers to understand the specific tax incidence applicable to them. Affiliates of KIASL may from time to time, be engaged in

any other transaction involving such securities/commodities and earn brokerage or other compensation or act as a market maker in the securities/commodities discussed herein or have other potential conflict of interest with

respect to any recommendation and related information and opinions. Wherever products offered by the Karvy Group entities may be recommended, it is to be noted that KIASL does not provide execution services and further

KIASL does not receive any monetary or non monetary benefit as regards such recommendations made. This newsletter and information contained herein is strictly confidential and meant solely for the selected recipient and may

not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of KIASL. Past performance is not necessarily a guide

to future performance. KIASL and its Group companies or any person connected with it accepts no liability whatsoever for the content of this newsletter, or for the consequences of any actions taken on the basis of the information

provided therein or for any loss or damage of any kind arising out of the use of this newsletter.

Nothing in this newsletter constitutes investment, legal, accounting and tax advice or a representation that any of the investment mentioned is suitable or appropriate to your specific circumstances. The information given in this

document on tax is for guidance only, and should not be construed as tax advice. Investors are advised to consult their respective tax advisers to understand the specific tax incidence applicable to them. While we would

endeavor to update the information herein on reasonable basis, KIASL , its associated companies, their directors and employees (“Karvy Group”) are under no obligation to update or keep the information current. Also, there may

be regulatory, compliance or other reasons that may prevent KIASL from doing so. KIASL will not treat recipients as customers by virtue of their receiving this newsletter. The value and return of investment may vary because of

changes in interest rates or any other reason. Karvy Group may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this newsletter. Recipients are advised to see

the offer documents provided by the Issuers/ Product Providers to understand the risks associated before making investments in the products mentioned. Recipients are cautioned that any forward-looking statements are not

predictions and may be subject to change without notice. KIASL operates from within India and is subject to Indian regulations. This newsletter is not directed or intended for distribution to, or use by, any person or entity who is a

citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject KIASL and affiliates to any

registration or licensing requirement within such jurisdiction. Certain category of investors in certain jurisdictions may or may not be eligible to invest in securities mentioned in the newsletter. Persons in whose possession this

document may come are required to inform themselves of and to observe such restriction. Entities of the Karvy Group provide execution services in the capacity of being stock broker, depository participant, portfolio managers

and the like. Recipients may choose to execute their transactions through entities of the Karvy group and pay applicable charge for the same.

Registered office Address: Karvy Investment Advisory Services Limited, ‘Karvy House’, 46, Avenue 4, Street No. 1, Banjara Hills, Hyderabad – 500034

SEBI Registration No: INA200001959](https://image.slidesharecdn.com/adviceforthewise-october2016-161123085303/85/Advice-for-the-Wise-October-2016-33-320.jpg)

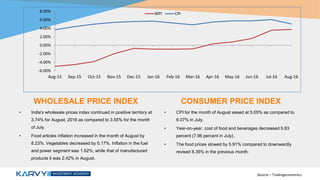

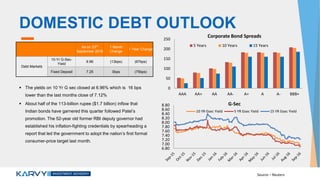

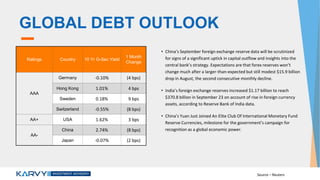

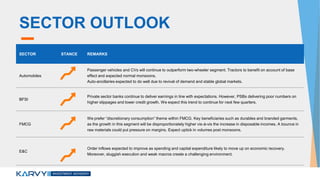

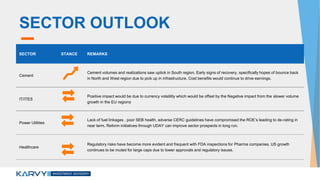

The document provides an overview and outlook across various asset classes and sectors in India and globally. Some key points: - Domestic equity markets have seen modest gains of around 8.5% year-to-date despite recent volatility due to political tensions. Bond yields have fallen in India on expectations of further rate cuts. - Global central banks like the Fed and ECB appear less accommodative but the US economy remains resilient. Growth has slowed in Japan and parts of Europe. - Automobiles, banks, FMCG and infrastructure sectors are expected to perform well in India, while cement may see a recovery. Select domestic sectors and stocks still appear attractive relative to other emerging markets.