The document discusses recent market volatility and the economic outlook. It notes that markets have declined due to ongoing issues with European debt and weakening global growth. While the risk of a US recession has risen, the US is expected to avoid a severe recession as key economic indicators remain above levels seen during the financial crisis. The document advocates for long-term investment strategies and cautions against abandoning equities due to short-term volatility, noting that markets have already priced in a significant drop in corporate earnings.

The impact of the current recession on the world economies, as presented by B.V.Raghunandan to MBA students at SDM College of Business Management, Mangalore in Karnataka state in India on February 26, 2009

"Show me the incentive and I'll show you the outcome" – Veripath Farmland Funds Q4 Investor Letter: Investing in a World of Financial Repression, Negative Real Rates, Valuation “Challenges” and Inflationary Forces.

Do G7 governments have an incentive to attempt to keep inflation higher for longer and real rates lower for longer? Negative real rates across a broad spectrum of credit assets are a graphic sign that we inhabit a world of financial repression orchestrated by central banks at the formal/informal behest of sovereign borrowers. In a normally functioning market, lenders do not provide capital to borrowers for negative yields – i.e., they do not pay for the privilege of lending. It goes without saying we are not in a normally functioning market.

Analysis Of Credit Crisis of 2008 - 2010Robert Malvin

An analysis of the credit crisis of 2008 - 2011. In depth look into key causes of the crisis, and why the Federal Reserve policies are not going to help. Analyzes the effects and implications of the monetary policy leading up to the crisis and current policy during the crisis. Reflects on the impacts of the current policies and where they might lead and offers alternative policies that would be better from the American and Global economies.

IN THIS SUMMARY

Economists and business leaders alike are still trying to understand the forces that led to the United States’ current economic woes. Some believe it is a down financial cycle or a recession, but in Aftershock, David Wiedemer, Robert Wiedemer, and Cindy Spitzer detail why they believe that neither explanation is correct. They describe what they have termed a Bubblequake–a popping of the real estate bubble, the private debt bubble, the stock market bubble, and the discretionary spending bubble. More alarming is that the economy is not going back to the way it was before because there are still more economic bubbles waiting to burst.

SUBSCRIBE TODAY

http://www.bizsum.com/summaries/aftershock

What we would like to consider is the price of taming inflation and how that will affect peoples, work, investments, and lives in the coming years.

https://youtu.be/0RuIunNvvKI

European Monetary Policy & Implications for US Markets, M.-O. Strauss-Kahn, N...Soledad Zignago

Presentation of Marc-Olivier Strauss-Kahn, Banque de France, at the Global Implications of Europe’s Redesign Conference, organized by SUERF, CGEG/COLUMBIA/SIPA, EIB and Société Générale, New York, October 5-6, 2016: "European Monetary Policy and Implications for US Markets" http://www.suerf.org/ny2016

http://www.eib.org/infocentre/events/all/global-implications-of-europes-redesign.htm

The impact of the current recession on the world economies, as presented by B.V.Raghunandan to MBA students at SDM College of Business Management, Mangalore in Karnataka state in India on February 26, 2009

"Show me the incentive and I'll show you the outcome" – Veripath Farmland Funds Q4 Investor Letter: Investing in a World of Financial Repression, Negative Real Rates, Valuation “Challenges” and Inflationary Forces.

Do G7 governments have an incentive to attempt to keep inflation higher for longer and real rates lower for longer? Negative real rates across a broad spectrum of credit assets are a graphic sign that we inhabit a world of financial repression orchestrated by central banks at the formal/informal behest of sovereign borrowers. In a normally functioning market, lenders do not provide capital to borrowers for negative yields – i.e., they do not pay for the privilege of lending. It goes without saying we are not in a normally functioning market.

Analysis Of Credit Crisis of 2008 - 2010Robert Malvin

An analysis of the credit crisis of 2008 - 2011. In depth look into key causes of the crisis, and why the Federal Reserve policies are not going to help. Analyzes the effects and implications of the monetary policy leading up to the crisis and current policy during the crisis. Reflects on the impacts of the current policies and where they might lead and offers alternative policies that would be better from the American and Global economies.

IN THIS SUMMARY

Economists and business leaders alike are still trying to understand the forces that led to the United States’ current economic woes. Some believe it is a down financial cycle or a recession, but in Aftershock, David Wiedemer, Robert Wiedemer, and Cindy Spitzer detail why they believe that neither explanation is correct. They describe what they have termed a Bubblequake–a popping of the real estate bubble, the private debt bubble, the stock market bubble, and the discretionary spending bubble. More alarming is that the economy is not going back to the way it was before because there are still more economic bubbles waiting to burst.

SUBSCRIBE TODAY

http://www.bizsum.com/summaries/aftershock

What we would like to consider is the price of taming inflation and how that will affect peoples, work, investments, and lives in the coming years.

https://youtu.be/0RuIunNvvKI

European Monetary Policy & Implications for US Markets, M.-O. Strauss-Kahn, N...Soledad Zignago

Presentation of Marc-Olivier Strauss-Kahn, Banque de France, at the Global Implications of Europe’s Redesign Conference, organized by SUERF, CGEG/COLUMBIA/SIPA, EIB and Société Générale, New York, October 5-6, 2016: "European Monetary Policy and Implications for US Markets" http://www.suerf.org/ny2016

http://www.eib.org/infocentre/events/all/global-implications-of-europes-redesign.htm

Trekking markets & more with InvestrekkInves Trekk

The report presents a summary of the Indian market activity during the week ended 27 June 2021. It also provides some important insights about the global market trends and Indian Market outlook for the Week beginning 28 June 2021.

No bubble trouble; stocks are still reasonably priced. This credit cycle has unique characteristics that continue to make high-yield bonds attractive. Interest-rate volatility poses greater risk than higher rates themselves.

US Fed rate hike in September 2015: Who will be the top 4 winners and losers?Aranca

The much hyped US Fed rate hike likely to be in September 2015 will mark the end of an era of free money. While it brings the good news that the most powerful economy of the world is back on track and can sustain a rate hike, there may be certain repercussions for the global markets. Here’s our take on who may win, and who may lose.

1. SEPT. 23, 2011

Recent market volatility

Markets took it on the chin this week as investors shunned assets they considered risky – equities, commodities,

etc. – and markets are reflecting this bias. Looking at the big picture, there hasn’t necessarily been any major ‘new’

news since mid-summer. The most recent market volatility has stemmed from more of the same issues; European

debt and fears about weakening global growth. Much of the current market sell-off can be attributed to a lack of

consumer and business confidence, which have been further exacerbated by less-than-hoped-for policy responses

to financial problems in the Eurozone.

As we’ve stated over the past couple of months, our outlook is that higher than normal volatility will persist as these

two issues are not ones that can be fixed quickly or easily. That’s clearly what we are experiencing and we expect

more of the same.

WHERE WE ARE TODAY

The risk of a recession in the U.S. has risen; however, we continue to feel that the U.S. will avoid a full-blown or

severe recession. In support of our view, we point out we are not in the same economic conditions we were in

during the financial crisis. Recent releases of some major economic indicators put them well above early 2009

levels, granted, coming off of higher levels in the past year. There remains a significant improvement in economic

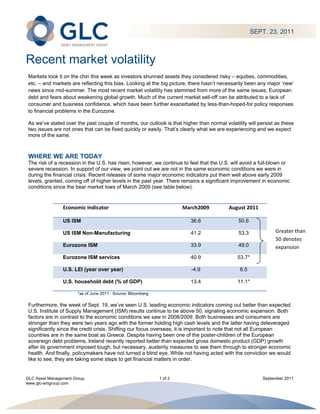

conditions since the bear market lows of March 2009 (see table below).

Economic Indicator March2009 August 2011

US ISM 36.6 50.6

US ISM Non-Manufacturing 41.2 53.3 Greater than

50 denotes

Eurozone ISM 33.9 49.0 expansion

Eurozone ISM services 40.9 53.7*

U.S. LEI (year over year) -4.9 6.5

U.S. household debt (% of GDP) 13.4 11.1*

*as of June 2011. Source: Bloomberg

Furthermore, the week of Sept. 19, we’ve seen U.S. leading economic indicators coming out better than expected.

U.S. Institute of Supply Management (ISM) results continue to be above 50, signaling economic expansion. Both

factors are in contrast to the economic conditions we saw in 2008/2009. Both businesses and consumers are

stronger than they were two years ago with the former holding high cash levels and the latter having deleveraged

significantly since the credit crisis. Shifting our focus overseas, it is important to note that not all European

countries are in the same boat as Greece. Despite having been one of the poster-children of the European

sovereign debt problems, Ireland recently reported better than expected gross domestic product (GDP) growth

after its government imposed tough, but necessary, austerity measures to see them through to stronger economic

health. And finally, policymakers have not turned a blind eye. While not having acted with the conviction we would

like to see, they are taking some steps to get financial matters in order.

GLC Asset Management Group 1 of 2 September 2011

www.glc-amgroup.com

2. Dave Gill, Senior Vice-President, Equities (London Capital), stresses that when markets capitulate, it tends to be a

sentiment-driven reaction in which investors overshoot to the downside and the proverbial baby gets thrown out

with the bathwater. That’s when you see great buying opportunities emerge. That said, he cautions that attractive

valuations (prices) on their own are not enough. Dave emphasizes, “You have to do your homework and that has

to be part of your daily process, not just on the big volatility days. We start everyday knowing the companies we

want to watch, so when opportunities present themselves, our homework is done, our research is up to the minute,

and we’re ready to act.”

GOING FORWARD

As Patricia Nesbitt, Senior Vice-President, Equities (GWLIM) describes it, “The fallout from equity market losses is

going to have to put the policymakers feet to the fire before investors believe the economy is ready to turn around,

and that hasn’t quite happened yet.” We believe both consumer and business confidence will need to gain traction

before we see a turnaround in investor sentiment and thus a turnaround in market performance. We’ll be watching

that carefully as this remains the linchpin to economic recovery.

We realize many investors will have questions and may be tempted to move from equities to the sidelines for a few

months to avoid market volatility. We caution against this kind of market timing. Markets are forward-looking and

have already priced in a significant drop in future corporate earnings. Estimates currently suggest a 20 to 25 per

cent drop in U.S. corporate earnings has already been priced-in. It’s the forward-looking nature of equity markets

that makes market bottoms difficult to predict. Your best chance to take advantage of the markets when they turn

around is to stay in the markets.

Market volatility is never easy to stomach, but cooler heads prevail. GLC’s professional portfolio managers don’t

abandon a well-thought-out investment strategy on short-term market volatility; rather part of the investment

strategy is to have well-defined processes that allow us to capitalize on market volatility. For investors, we also

stress the importance of not abandoning long-term investment strategies which, for most investors, will include a

diversified combination of equity (domestic and foreign) and fixed income investments.

Copyright GLC, You may not reproduce, distribute, or otherwise use any of this article without the prior written consent of GLC Asset Management Group

The views expressed in this commentary are those of GLC Asset Management Group Ltd. (GLC) as at the date of publication and are subject to

change without notice. This commentary is presented only as a general source of information and is not intended as a solicitation to buy or sell

specific investments, nor is it intended to provide tax or legal advice. Prospective investors should review the offering documents relating to any

investment carefully before making an investment decision and should ask their advisor for advice based on their specific circumstances.

GLC Asset Management Group 2 of 2 September 2011

www.glc-amgroup.com