Download as PDF, PPTX

+1)

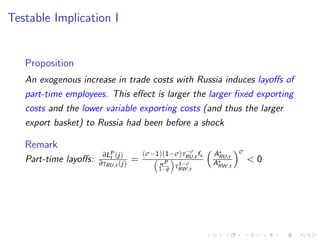

Since:

(1 − ψ) φ σ−1

σ − 1 0, σ−1

σ 0, and − 1

σ ([1 − φ + ψφ] (σ − 1) + 1) 0, the

layoffs of full-time labor are more likely, i.e. a decrease in LF−

t+1 (j), the higher

are variable firm’s costs to trade with the rest of the world and the smaller is

part-time employment](https://image.slidesharecdn.com/povilaslastauskasboe1dec2022-230117102054-41287e9a/85/Adjusting-to-Economic-Sanctions-32-320.jpg)

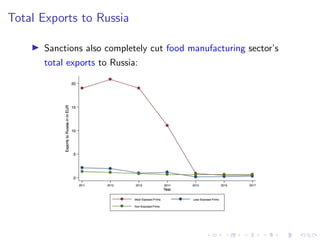

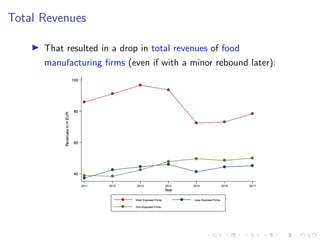

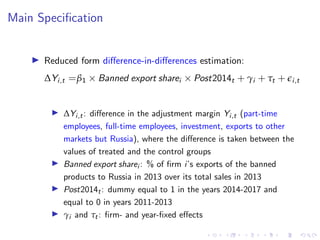

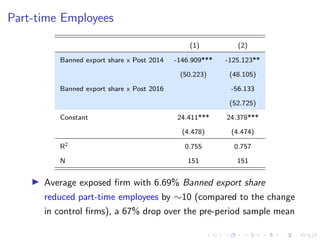

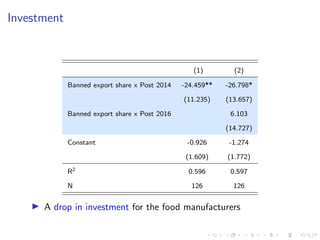

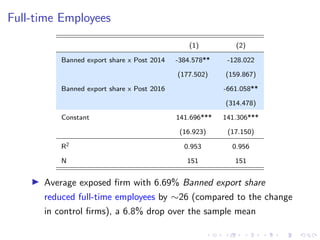

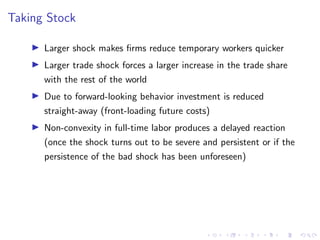

The document summarizes a study examining how Lithuanian food manufacturing firms adjusted to trade sanctions imposed by Russia in 2014 that banned many agricultural imports from the EU. The main adjustments included: - Reducing part-time employment as the most flexible margin of adjustment. Larger reductions occurred for firms more exposed to the Russian market. - Increasing exports to other countries to compensate for lost Russian exports. More exposed firms increased other exports more. - Decreasing investment and full-time employment for more exposed firms, though full-time employment adjustments took longer. A conceptual framework is presented predicting this sequence of adjustments, with part-time labor adjusting first due to lower costs, followed by exports, investment,