Download to read offline

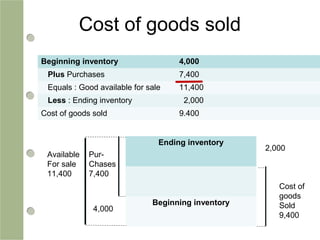

This document provides an overview of key accounting concepts like debits and credits, balance sheets, income statements, and cash flow statements. It includes examples of trial balances, income statements, cash flow statements, and balance sheets for a sample company called Barca. Worked examples are provided to illustrate calculating cost of goods sold.