Downloaded 37 times

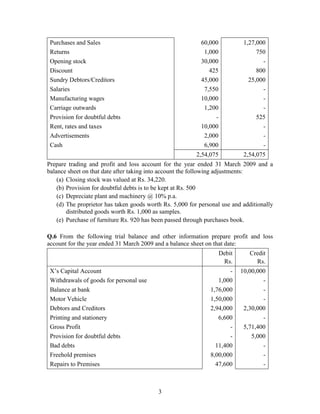

The document contains 8 questions asking to prepare final accounts (trading account, profit and loss account, balance sheet) for various businesses based on trial balance information and additional adjustments provided. Details include opening/closing stock, purchases, sales, expenses, assets, liabilities, depreciation, provisions etc. to derive the net profit/loss for the year and financial position as on the balance sheet date.

![Financial_statement_for_the_company[1].pdf](https://cdn.slidesharecdn.com/ss_thumbnails/financialstatementforthecompany1-241017204922-2fcfacd7-thumbnail.jpg?width=640&height=640&fit=bounds)

![Working and functions_of_rbi[1]](https://cdn.slidesharecdn.com/ss_thumbnails/workingandfunctionsofrbi1-110522002449-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac10[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac101-p-110520054545-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac08[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac081-p-110520054521-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac05[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac051-p-110520054504-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac14[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac141-p-110520054443-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac06[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac061-p-110520054419-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)