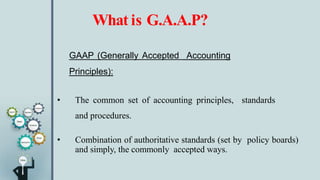

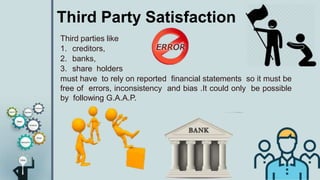

GAAP (Generally Accepted Accounting Principles) are the common set of accounting principles, standards and procedures that ensure financial statements are accurate, consistent, and transparent. Key principles include separate entity, money measurement, dual aspect, and going concern concepts. Adhering to GAAP allows for long-term decision making, financial analysis, record keeping, and comparison between companies. It also satisfies third parties like creditors and shareholders who rely on accurate financial reporting. Accounting conventions like prudence, consistency, full disclosure, and materiality help address transactions not fully covered by standards.