Learning Objectives

1. Describethe nature of partnership

2. Identify the different kinds of partners

3. Identify the classifications of partnership

4. Record the contributions of partners into the partnership

5. Account for the conversion of single proprietorship into partnership

6. Prepare a statement of financial position for the partnership

immediately after its formation

Partnership

is a formalagreement between two or more individuals or entities

to manage and operate a business together, with the intention of

sharing profits and losses.

Legal Basis:

· Civil Code of the Philippines (Title IX, Art. 1767–1867)

· Accounting Standards: CFAS, PFRS, PAS 1 (for general-purpose FS)

5.

The Nature ofPartnership

Co-ownership of Property

Assets contributed are shared by

all partners as common property.

Mutual Agency

Each partner acts as an agent,

binding the partnership in

normal business.

Unlimited Liability

Partners are personally

responsible for all debts, even

from personal assets.

Limited Life

The partnership ends after

changes like death, bankruptcy,

or goal completion.

Profit Division

Profits are shared per

agreement, emphasizing profit

as the main purpose.

6.

Articles of Co-Partnership

KeyContract Details

• Partnership name and

partners' identities

• Business nature, purpose,

and principal office

• Capital contributions and

their agreed values

Partner Rights and

Duties

• Profit and loss sharing

• Bookkeeping procedures

• Additional investments

and withdrawals

Dispute and Dissolution

• Procedures for dissolving the partnership

• Arbitration provisions for settling disputes

7.

Capitalist Partner

Contributes capitalas money

or property to finance

partnership operations.

Industrial Partner

Offers labor, skills, or

professional services essential

to the business.

Capitalist-Industrial

Partner

Invests capital and participates

actively through services or labor.

Kinds of Partners

By Contribution

8.

General Partner

Holds unlimitedliability,

responsible beyond their

capital contribution.

Limited Partner

Liability limited to capital

contribution, usually not involved in

management.

Kinds of Partners

By Liability

9.

Managing Partner

Directs day-to-daybusiness operations

and decisions actively.

Invests or manages discreetly

without public disclosure.

Silent Partner

Known to outsiders but not involved

in daily management.

Dormant Partner

Neither publicly known nor active;

typically, an investor only.

Ostensible Partner

Seen by outsiders as a partner and

may be liable to third parties.

Secret Partner

Kinds of Partners

By Role

10.

Classification of

Partnerships byLiability

General Partnership

All partners have unlimited liability extending to

personal assets.

Limited Partnership

Includes one or more general partners and

limited partners; firm name includes “Limited”

or “Ltd.”

11.

Classification by Objectof Partnership

Universal Partnership of All

Present Property

Partners contribute all their current

property to a common fund to share

profits and assets.

Universal Partnership of

Profits

Partners share all profits acquired

through their industry or work during

the partnership.

Particular Partnership

Formed for specific things,

undertakings, or professional

exercise.

12.

Classification by Duration

Partnershipat Will

No fixed period; can be terminated anytime by

mutual agreement or partner’s will.

Partnership with Fixed Term

Exists for a specified period or objective agreed

upon by partners.

13.

Classification by Purpose

Commercial/TradingPartnership

Organized to conduct business

transactions like merchandising or

manufacturing.

Professional Partnership

Formed for practicing professions such as

law, accounting, or medicine.

14.

Advantages and Disadvantagesof Partnerships

Advantages

• Combines skills and talents of multiple

individuals

• Generates more capital than sole

proprietorship

Disadvantages

• Potential conflicts from decision-making

differences

• Limited life due to partner changes

• Mutual agency risks liability for wrongful acts

• Unlimited liability risks personal assets

15.

Accounting for Partnership

Formation

AccountingProcedures

Similar to sole proprietorship but with separate

capital and drawing accounts for each partner.

Recording Contributions

Assets contributed are recorded by crediting

the contributing partner’s capital account.

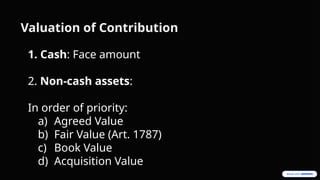

Valuation of Contribution

1.Cash: Face amount

2. Non-cash assets:

In order of priority:

a) Agreed Value

b) Fair Value (Art. 1787)

c) Book Value

d) Acquisition Value

18.

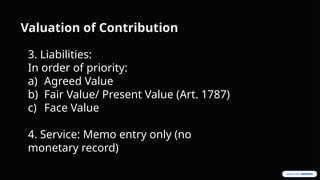

Valuation of Contribution

3.Liabilities:

In order of priority:

a) Agreed Value

b) Fair Value/ Present Value (Art. 1787)

c) Face Value

4. Service: Memo entry only (no

monetary record)

19.

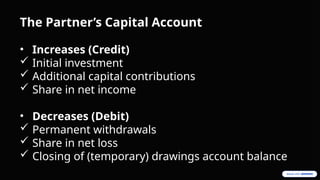

The Partner’s CapitalAccount

• Increases (Credit)

Initial investment

Additional capital contributions

Share in net income

• Decreases (Debit)

Permanent withdrawals

Share in net loss

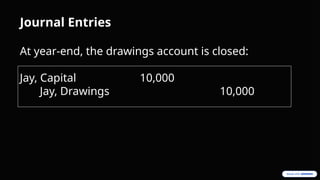

Closing of (temporary) drawings account balance

20.

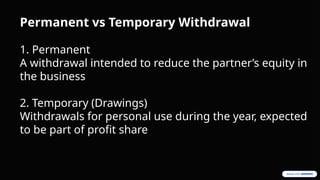

Permanent vs TemporaryWithdrawal

1. Permanent

A withdrawal intended to reduce the partner’s equity in

the business

2. Temporary (Drawings)

Withdrawals for personal use during the year, expected

to be part of profit share

21.

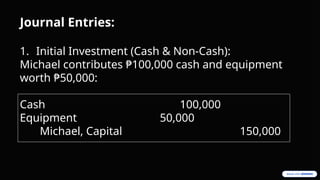

Journal Entries:

1. InitialInvestment (Cash & Non-Cash):

Michael contributes ₱100,000 cash and equipment

worth ₱50,000:

Cash 100,000

Equipment 50,000

Michael, Capital 150,000

22.

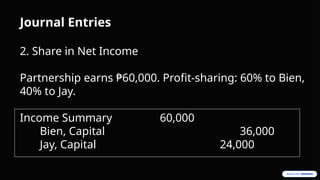

Journal Entries

2. Sharein Net Income

Partnership earns ₱60,000. Profit-sharing: 60% to Bien,

40% to Jay.

Income Summary 60,000

Bien, Capital 36,000

Jay, Capital 24,000

23.

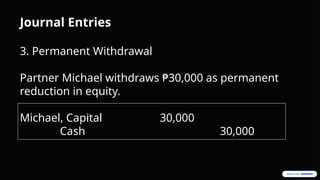

Journal Entries

3. PermanentWithdrawal

Partner Michael withdraws ₱30,000 as permanent

reduction in equity.

Michael, Capital 30,000

Cash 30,000

24.

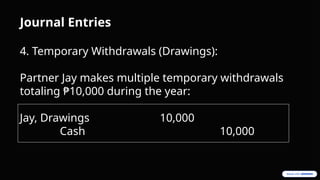

Journal Entries

4. TemporaryWithdrawals (Drawings):

Partner Jay makes multiple temporary withdrawals

totaling ₱10,000 during the year:

Jay, Drawings 10,000

Cash 10,000

#1 This chapter covers the essentials of partnership formation. You will learn to describe the nature of partnerships, identify different kinds of partners, and classify partnerships. Additionally, you will understand how to record partner contributions, convert a sole proprietorship into a partnership, and prepare a statement of financial position after formation.

These foundational skills are critical for managing and accounting for partnerships effectively.

#4 It's a business structure where partners contribute resources, which can include money, property, labor, or

skills, to a common fund and collectively oversee the business

operations.

#13 a locally grown coffee chain in the Philippines, was founded by Steve Benitez and Carmen Benitez. Beginning as a small coffee cart in 1996, this company has burgeoned into a flourishing chain boasting over 100 branches nationwide