THE OWNER JOSEMERCADO, INVESTED PHP 10 000 AND BORROWED PHP 50

000 TO START HIS BUSINESS. HE PURCHASED PHOTOCOPYING MACHINE FOR

PHP 30 000 AND SUPPLIES FOR PHP 10 000, SALARY FOR PHP 4000, AND

BUSINESS PERMIT FOR PHP 2000. THE BUSINESS CONSUMED ELECTRICITY

FOR PHP 2 500 PAYABLE THE FOLLOWING MONTH. DURING THE FIRST

MONTH OF BUSINESS OPERATIONS, THE PHOTOCOPYING SERVICE

GENERATED PHP 10 000 REVENUE

WHICH OF THE AMOUNTS CITED ABOVE DO YOU THINK WILL BE INCLUDED

IN THE BUSINES’S FINANCIAL REPORTS? WHAT IS YOUR REASON FOR

INCLUDING SAID AMOUNTS?

OPENING CASE

3.

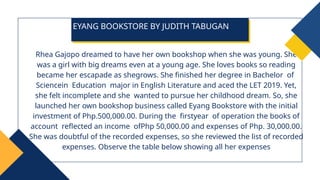

Rhea Gajopo dreamedto have her own bookshop when she was young. She

was a girl with big dreams even at a young age. She loves books so reading

became her escapade as shegrows. She finished her degree in Bachelor of

Sciencein Education major in English Literature and aced the LET 2019. Yet,

she felt incomplete and she wanted to pursue her childhood dream. So, she

launched her own bookshop business called Eyang Bookstore with the initial

investment of Php.500,000.00. During the firstyear of operation the books of

account reflected an income ofPhp 50,000.00 and expenses of Php. 30,000.00.

She was doubtful of the recorded expenses, so she reviewed the list of recorded

expenses. Observe the table below showing all her expenses

EYANG BOOKSTORE BY JUDITH TABUGAN

5.

• As accountingis considered as

language of business, it has rules or

concepts and principles to follow,

much like grammar of any

language. It communicates the

financial condition and performance

of a business to interested users for

decision making purposes

• A widely accepted set of rules,

concepts, and principles referred to as

the Generally Accepetd Accounting

Principles (GAAP) governs the

application of accounting procedures.

6.

• Examples: Mr.Alex, the owner of Bilis

Serbisyo Repair Shop, bought

supplies for the school project of his

son using his own money.

• It assumes that all of the business transactions are

separate from the business owner’s personal

transactions. A business is considered a distinct

entity from the owner and thereof the two should

be treated separately. Any personal transaction of

its owner should not be recorded in the company’s

accounting book, and vice versa, unless the

owner’s personal transactions investing or

withdrawing resources from t

1. ECONOMIC ENTITY ASSUMPTION

7.

• Example: Whena painter finishes

performing his services, he should

record it as revenue even if his

professional fee is still uncollected.

When the painter has to pay his

studio rent, he should record it as an

expense even if it is unpaid.

• It requires that all business transactions

and other events are recognized in the

accounting records when they occur,

rather than when the cash or equivalent

is received or paid.

ACCURAL BASIS ASSUMPTION

8.

• Example: Mr.Clark’s sushi business is

experiencing difficulty, but he is still

expecting it to continue that is why he

still updates his books of account.

• It gives the pretense that a business will

continue to operate in the foreseeable

future and will not be liquidated for

atleast 12mos. This entails that

operations will continue and settle its

obligations rather than sell its assets at

low prices. This means that the business

is expected to continue indefinitely.

GOING CONCERN ASSUMPTION

9.

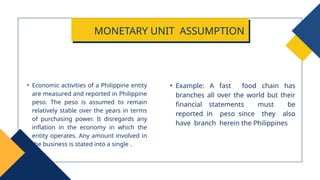

• Example: Afast food chain has

branches all over the world but their

financial statements must be

reported in peso since they also

have branch herein the Philippines

• Economic activities of a Philippine entity

are measured and reported in Philippine

peso. The peso is assumed to remain

relatively stable over the years in terms

of purchasing power. It disregards any

inflation in the economy in which the

entity operates. Any amount involved in

the business is stated into a single .

MONETARY UNIT ASSUMPTION

10.

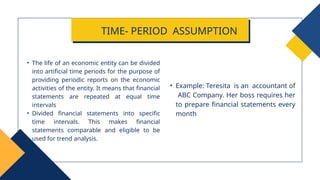

• Example: Teresitais an accountant of

ABC Company. Her boss requires her

to prepare financial statements every

month

• The life of an economic entity can be divided

into artificial time periods for the purpose of

providing periodic reports on the economic

activities of the entity. It means that financial

statements are repeated at equal time

intervals

• Divided financial statements into specific

time intervals. This makes financial

statements comparable and eligible to be

used for trend analysis.

TIME- PERIOD ASSUMPTION

11.

• The basicaccounting principles are detailed accounting

rules and guidelines that entities must follow when

measuring, recording and reporting financial data.

BASIC ACCOUNTING

PRINCIPLES

12.

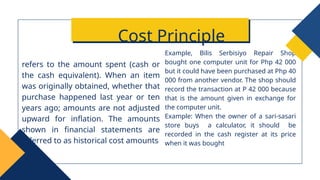

Example, Bilis SerbisiyoRepair Shop

bought one computer unit for Php 42 000

but it could have been purchased at Php 40

000 from another vendor. The shop should

record the transaction at P 42 000 because

that is the amount given in exchange for

the computer unit.

Example: When the owner of a sari-sasari

store buys a calculator, it should be

recorded in the cash register at its price

when it was bought

refers to the amount spent (cash or

the cash equivalent). When an item

was originally obtained, whether that

purchase happened last year or ten

years ago; amounts are not adjusted

upward for inflation. The amounts

shown in financial statements are

referred to as historical cost amounts

Cost Principle

13.

• Example: Aleenabought a computer

for her computer shop. She made

sure that it was recorded on the

financial reports

The account should include sufficient

information. To permit the

stakeholders to make an informed

judgement about financial condition

of the enterprise

FULL DISCLOSURE PRINCIPLE

14.

• Example:Siony soldthe goods to her

customers, the revenue increases

and the inventories decrease. The

reduction of the inventories in

relation to revenues is called the cost

of goods sold and it should be

recorded in the period in which the

revenues were earned

Requires that expenses be matched

with revenues. It means that in given

accounting period, the revenue

recorded should have its

corresponding expense recorded in

order to show true profit of the

business

MATCHING PRINCIPLE

15.

Are recognized assoon as goods

have been sold or a service has been

rendered, regardless of when the

money is actually received. Revenue

is recognized when the earnings

process is virtually complete and an

exchange transaction has occurred

REVENUE RECOGNITION PRINCIPLE

16.

• Example: Robi,an accounting clerk,

purchased a friction pen. She

estimated it to have a useful life up

the three months. Since a friction pen

is immaterial relative to assets, it

should be recorded as an expense

Business transactions that may affect

the decisions of a user of financial

information are considered

important or material, and thus must

be reported properly

MATERIALITY PRINCIPLE

17.

• Example:Suppose anasset owned by Mico,

like inventory was bought for Php 20,000.00

but can now be bought for Php 15,000.00.

Then the company must immediately write

down the value of the asset to at Php

15,000.00 because of the lower cost in the

market. But if the inventory was bought for

Php 20,000.00 and now has a market value

of Php 25,000.00, it must still be shown a

Php 20,000.00 on the books because the

gain is only recorded when the inventory or

asset is sold

Focuses on the idea of prudence that

income assets should not be

overstated while liabilities and

expenses are not understands. Lower

revenue and higher expenses may

result to lower reported income.

Helps the accountant break a tie

while remaining unbiased and

objective.

CONSERVATISM PRINCIPLE

18.

This principle requiresbusiness

transactions to have so e form of

impartial supporting evidence or

documentation.

OBJECTIVITY PRINCIPLE

![Theory Base of Accounting [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/theorybaseofaccountingautosaved-230923134922-7fdbd224-thumbnail.jpg?width=640&height=640&fit=bounds)