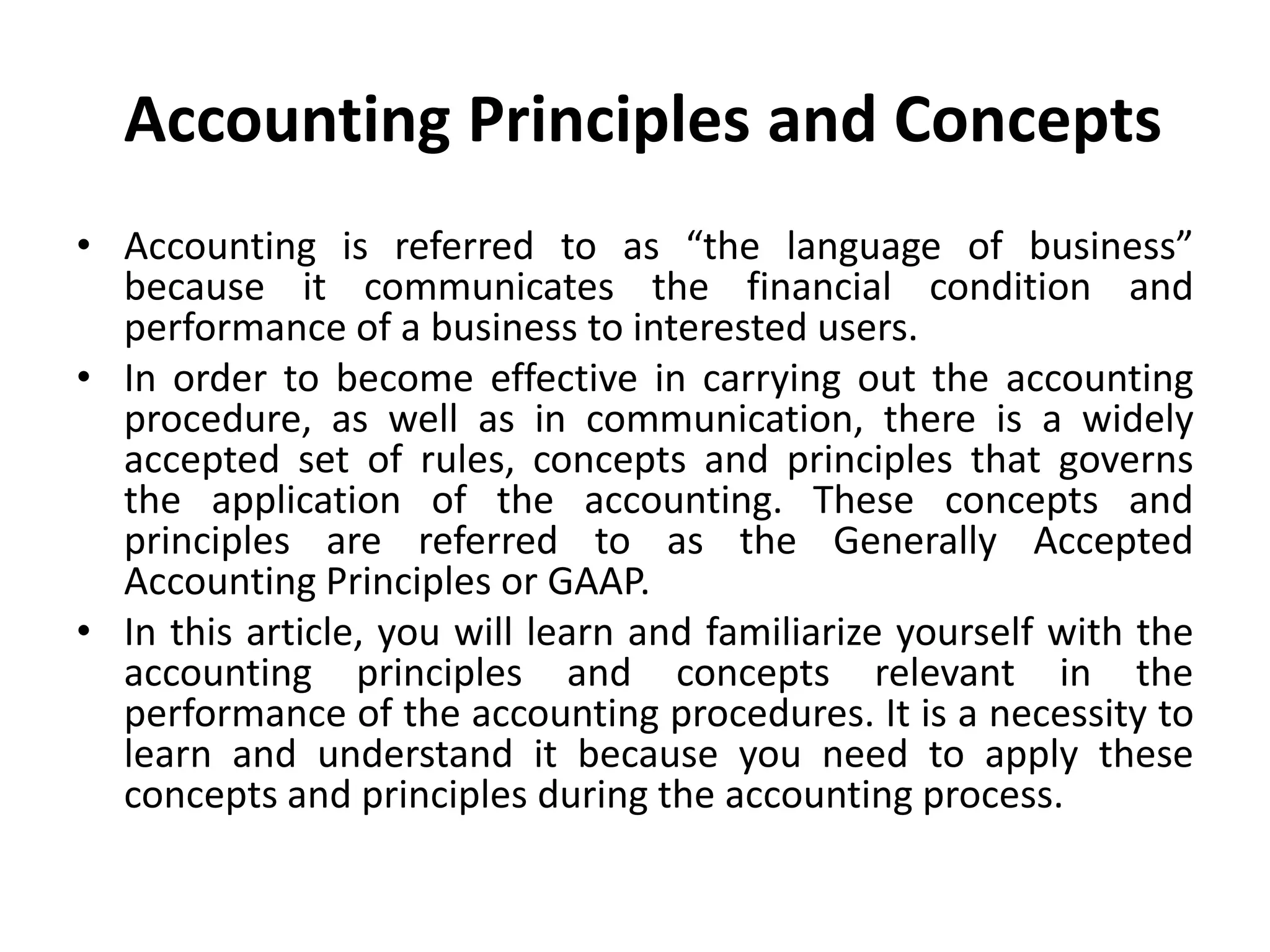

1. Accounting communicates the financial condition and performance of a business to interested users through financial reports.

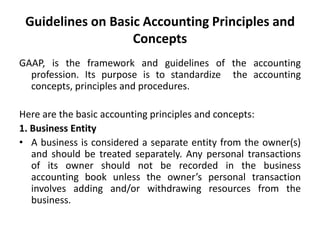

2. Generally Accepted Accounting Principles (GAAP) are the widely accepted set of rules, concepts and principles that govern financial accounting and reporting.

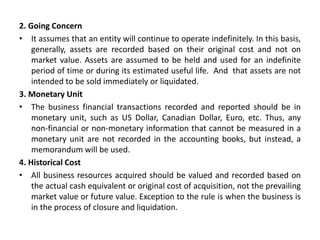

3. This document discusses 11 basic accounting principles and concepts that form the framework for GAAP, including business entity, going concern, monetary unit, historical cost, matching, accounting period, conservatism, consistency, materiality, objectivity, and accrual accounting.