Lesson Objectives:

At theend of this lesson, the learners will be

able to:

• enumerate the principles and concepts of

accounting;

• identify generally accepted accounting principles,

and

• apply the accounting principle in a various

business setting

3.

Accounting concepts, principlesand

assumptions

1.Accounting/Business entity principle/assumption

2.Going concern principle/assumption

3.Time period principle/assumption

4.Accrual Accounting

5.Cash basis of accounting/objectivity principle

6.Matching Principle

7.Prudence or materiality principle

8.Monetary unit principle (also known as money measurement

concept)

9.Cost Principles

10. Disclosure Principles

4.

Accounting concepts, principlesand

assumptions

Accounting concepts, principles and assumptions are

essential in the practice of accountancy.

Financial statements become more comparable and

more useful to users if these concepts, principles and

assumptions are followed by business.

These serves as foundation of accounting in order to

avoid misunderstanding and enhance the understanding

and usefulness of financial statements.

5.

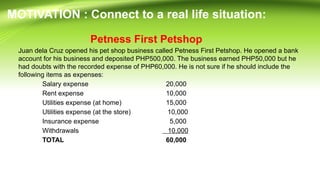

MOTIVATION : Connectto a real life situation:

Petness First Petshop

Juan dela Cruz opened his pet shop business called Petness First Petshop. He opened a bank

account for his business and deposited PHP500,000. The business earned PHP50,000 but he

had doubts with the recorded expense of PHP60,000. He is not sure if he should include the

following items as expenses:

Salary expense 20,000

Rent expense 10,000

Utilities expense (at home) 15,000

Utilities expense (at the store) 10,000

Insurance expense 5,000

Withdrawals 10,000

TOTAL 60,000

6.

Accounting concepts, principlesand

assumptions

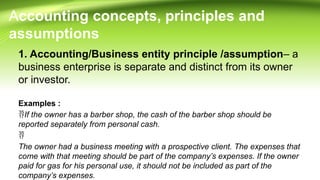

1. Accounting/Business entity principle /assumption– a

business enterprise is separate and distinct from its owner

or investor.

Examples :

If the owner has a barber shop, the cash of the barber shop should be

reported separately from personal cash.

The owner had a business meeting with a prospective client. The expenses that

come with that meeting should be part of the company’s expenses. If the owner

paid for gas for his personal use, it should not be included as part of the

company’s expenses.

7.

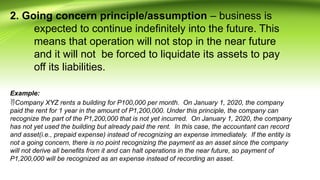

2. Going concernprinciple/assumption – business is

expected to continue indefinitely into the future. This

means that operation will not stop in the near future

and it will not be forced to liquidate its assets to pay

off its liabilities.

Example:

Company XYZ rents a building for P100,000 per month. On January 1, 2020, the company

paid the rent for 1 year in the amount of P1,200,000. Under this principle, the company can

recognize the part of the P1,200,000 that is not yet incurred. On January 1, 2020, the company

has not yet used the building but already paid the rent. In this case, the accountant can record

and asset(i.e., prepaid expense) instead of recognizing an expense immediately. If the entity is

not a going concern, there is no point recognizing the payment as an asset since the company

will not derive all benefits from it and can halt operations in the near future, so payment of

P1,200,000 will be recognized as an expense instead of recording an asset.

8.

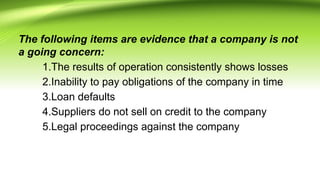

The following itemsare evidence that a company is not

a going concern:

1.The results of operation consistently shows losses

2.Inability to pay obligations of the company in time

3.Loan defaults

4.Suppliers do not sell on credit to the company

5.Legal proceedings against the company

9.

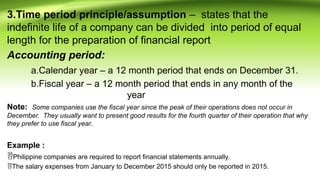

3.Time period principle/assumption– states that the

indefinite life of a company can be divided into period of equal

length for the preparation of financial report

Accounting period:

a.Calendar year – a 12 month period that ends on December 31.

b.Fiscal year – a 12 month period that ends in any month of the

year

Note: Some companies use the fiscal year since the peak of their operations does not occur in

December. They usually want to present good results for the fourth quarter of their operation that why

they prefer to use fiscal year.

Example :

Philippine companies are required to report financial statements annually.

The salary expenses from January to December 2015 should only be reported in 2015.

10.

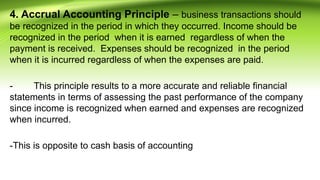

4. Accrual AccountingPrinciple – business transactions should

be recognized in the period in which they occurred. Income should be

recognized in the period when it is earned regardless of when the

payment is received. Expenses should be recognized in the period

when it is incurred regardless of when the expenses are paid.

- This principle results to a more accurate and reliable financial

statements in terms of assessing the past performance of the company

since income is recognized when earned and expenses are recognized

when incurred.

-This is opposite to cash basis of accounting

11.

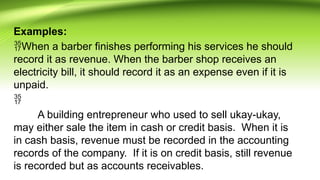

Examples:

When a barberfinishes performing his services he should

record it as revenue. When the barber shop receives an

electricity bill, it should record it as an expense even if it is

unpaid.

A building entrepreneur who used to sell ukay-ukay,

may either sale the item in cash or credit basis. When it is

in cash basis, revenue must be recorded in the accounting

records of the company. If it is on credit basis, still revenue

is recorded but as accounts receivables.

12.

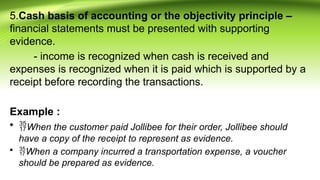

5.Cash basis ofaccounting or the objectivity principle –

financial statements must be presented with supporting

evidence.

- income is recognized when cash is received and

expenses is recognized when it is paid which is supported by a

receipt before recording the transactions.

Example :

• When the customer paid Jollibee for their order, Jollibee should

have a copy of the receipt to represent as evidence.

• When a company incurred a transportation expense, a voucher

should be prepared as evidence.

13.

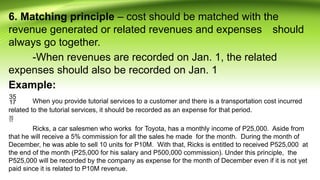

6. Matching principle– cost should be matched with the

revenue generated or related revenues and expenses should

always go together.

-When revenues are recorded on Jan. 1, the related

expenses should also be recorded on Jan. 1

Example:

When you provide tutorial services to a customer and there is a transportation cost incurred

related to the tutorial services, it should be recorded as an expense for that period.

Ricks, a car salesmen who works for Toyota, has a monthly income of P25,000. Aside from

that he will receive a 5% commission for all the sales he made for the month. During the month of

December, he was able to sell 10 units for P10M. With that, Ricks is entitled to received P525,000 at

the end of the month (P25,000 for his salary and P500,000 commission). Under this principle, the

P525,000 will be recorded by the company as expense for the month of December even if it is not yet

paid since it is related to P10M revenue.

14.

7. Prudence ormateriality principle – also known as

conservatism which means in case of doubt, record any

loss and do not record any gain

-used by accountants to ensure that income and assets

and liabilities and expenses are not overstated.

-Accountants apply this concept when transactions are

sometimes uncertain like warranty expenses

Example :

When an accountant is unsure whether or not to recognize as an expense, the

concept of prudence states that he or she should recognized it in the accounting

records. On the other hand, if an accountant is unsure whether or not to recognize

income, prudence states that he or she should not recognize it.

15.

8. Monetary unitprinciple (also known as money

measurement concept)

- states that only those events and transactions are

recorded in books of accounts of the business which can be

measured and expressed in monetary terms. Amounts should

only be stated into a single monetary unit. Therefore, an

information that cannot be expressed in terms of money is

useless for financial accounting purpose and is therefore not

recorded.

Example:

Jollibee should report financial statements in pesos even if they have a

store in the United States.

16.

9. Cost principle- is an accounting principle that records

assets at their respective cash amounts at the time the

asset was purchased or acquired. Assets that are recorded

can include short-term and long-term assets, liabilities and

any equity, and these assets are always recorded at their

original cost.

Example:

When Jollibee buys a cash register, it should record the

cash register at its price when they bought it.

17.

10. Disclosure principle(Substance over form) - is a

concept that requires a business to report all necessary

information about their financial statements and other

relevant information to any persons who are

accustomed to reading this information.

In other words, all relevant and material information

should be reported.

Example:

The company should report all relevant information.

18.

Generally Accepted AccountingPrinciples (GAAP)

-Consists of accounting principles, standards, rules and

guidelines that companies follow to achieve consistency and

comparability of a company’s financial statements.

-Help management in understanding trends persistent in

the company by comparing past and current performance to

check the weal and strong points of the company’s operations.

-Created by individuals in the accountancy profession

19.

International Financial ReportingStandards (IFRS)

-Are pronouncement issued by the International Accounting

Standard Board (IASB) that intend to enhance the comparability

of the financial statements of all companies around the world

Note:

In the past, the function of IASB is performed by International Accounting

Standards Committee (IASC).

The pronouncement of IASC are called International Accounting

Standards (IAS). Up to this day, the IASB still adheres to the IAS in

addition to their own pronouncement- the IFRS.

Philippines – follows standards of both IAS and IFRS

USA – follows the guidelines provided by the GAAP

20.

Philippine Financial ReportingStandards (PFRS)

The Philippine Financial Reporting Standards Council (FRSC)

issues standards to be used in the Philippines in the form of the

Philippines Financial Reporting Standards (PFRS) which includes the ff.:

1.Philippines Financial Reporting Standards (PFRS) which

corresponds to International Financial Reporting Standards (IFRS)

2.Philippine Accounting Standards(PAS) which corresponds to

International Financial Reporting Standards (IFRS)

3.Interpretations of accounting standards issued by the Philippine

Interpretations Committee in accordance with interpretations of the

International Financial Reporting Interpretations Committee (IFRIC)

and the Standing interpretations Committee

21.

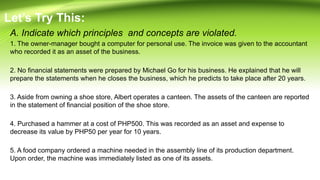

A. Indicate whichprinciples and concepts are violated.

1. The owner-manager bought a computer for personal use. The invoice was given to the accountant

who recorded it as an asset of the business.

2. No financial statements were prepared by Michael Go for his business. He explained that he will

prepare the statements when he closes the business, which he predicts to take place after 20 years.

3. Aside from owning a shoe store, Albert operates a canteen. The assets of the canteen are reported

in the statement of financial position of the shoe store.

4. Purchased a hammer at a cost of PHP500. This was recorded as an asset and expense to

decrease its value by PHP50 per year for 10 years.

5. A food company ordered a machine needed in the assembly line of its production department.

Upon order, the machine was immediately listed as one of its assets.

Let’s Try This:

22.

6. The statementof financial position of a company included an equipment purchased from Japan for

350,000 yen. It was reported at that amount in the statement of financial position while all the other

assets were reported in Philippine pesos.

7. Ace Company purchased a large printing machine for Php1,000,000 (a material amount) and

recorded the purchase as an expense.

8. ABC Company purchased land two years ago at a price of Php300,000. Because the value of the

land has appreciated to Php500,000, the company has valued the land at Php500,000 in its most

recent balance sheet.

9. XYZ Corporation has not prepared financial statements for external users for over three years.

10. At the end of each year, King Company reports its economic resources on a liquidation basis even

though it is likely to operate in the future.

11. A school purchased an eraser with an estimated useful life of three years. Since an eraser is

immaterial relative to assets, it was recorded as an expense.

23.

B.Identify what accountingprinciple, concept and assumption is used in each statement

1. The accountant return to the employees the receipts of the personal transaction they made during working hours.

2. The accountant finishes the financial statement for the year after the 12- month fiscal period and begins with the new

fiscal year.

3. Company X purchased a piece of property, and are now the current owners. A passing pedestrian had a terrible fall on the

property and got badly injured. This pedestrian is now suing Company X for a significant amount of money for

negligence. The pedestrian is likely to win the lawsuit in the following year.

4. The accountant receives the utility billing statements for June and includes them in the financial statement for the same

month.

5. The accountant compute the depreciation on the basis of expected economic life of fixed assets rather than their current

market value.

6. The accountant receives the utility billing statements for June and includes them in the financial statement for the same

month.

7. The accountant records contingent liability that the company might incur in a legal battle with its employees to indicate

that the company might have to pay out employees.

8. The accountant records income as soon as the sales people report the delivery of goods to the clients.

9. The accountant records the value of the acquired computer units at its prevailing price.

10. The accountant gathers all the official receipts, vouchers, and invoices for a particular period and records them

objectively.

Editor's Notes

#2 Accounting is called the language of business. It communicates the financial condition and performance of a business to interested users for decision-making purposes. The Generally Accepted Accounting Principles (GAAP) is a widely accepted set of rules, concepts and principles that governs the application of accounting procedures. The GAAP has been developed by the accounting professionals to guide preparers of financial statements in

recording and reporting financial information regarding a business enterprise, hence aiding in the effective execution of the accounting procedure and in communicating the financial condition of the business.

#5 Analyze the business transaction below. Remember that in the normal course of business, accounting principles are sometimes violated in which owners must be aware of it.

Among the expenses enumerated, which of the following should not be included as expenses. Explain why.

Note: The activity is an application of the Accounting Entity Principle/Assumption which is one of the most important principles in accounting.

#13 Note: Without the matching principle, company will record as an expenses to the month when it is paid.

#14 Albeit prudence – is the preferred course of action when making judgements; deliberately being too conservative is not an allowed practice. Why? Because there are some company used to exercise prudence when recognizing expense for the main reason of bloating expenses to lower tax payments.

Example: ➢ In case of doubt, expenses should be recorded at a higher amount. Revenue should be recorded at a lower amount.