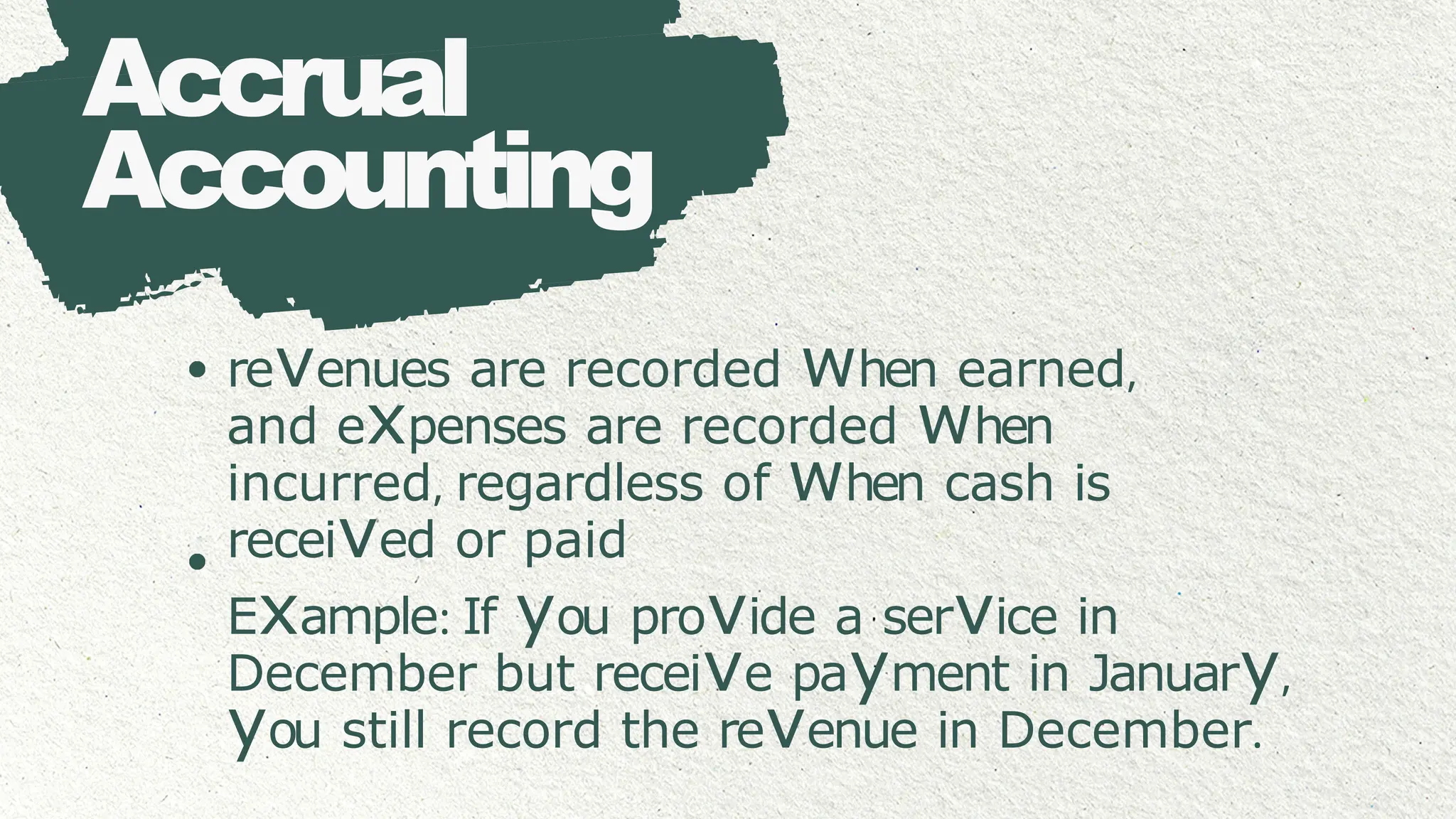

Accrual

Accounting

revenues are recordedwhen earned,

and expenses are recorded when

incurred, regardless of when cash is

received or paid

Example: If you provide a service in

December but receive payment in January,

you still record the revenue in December.

4.

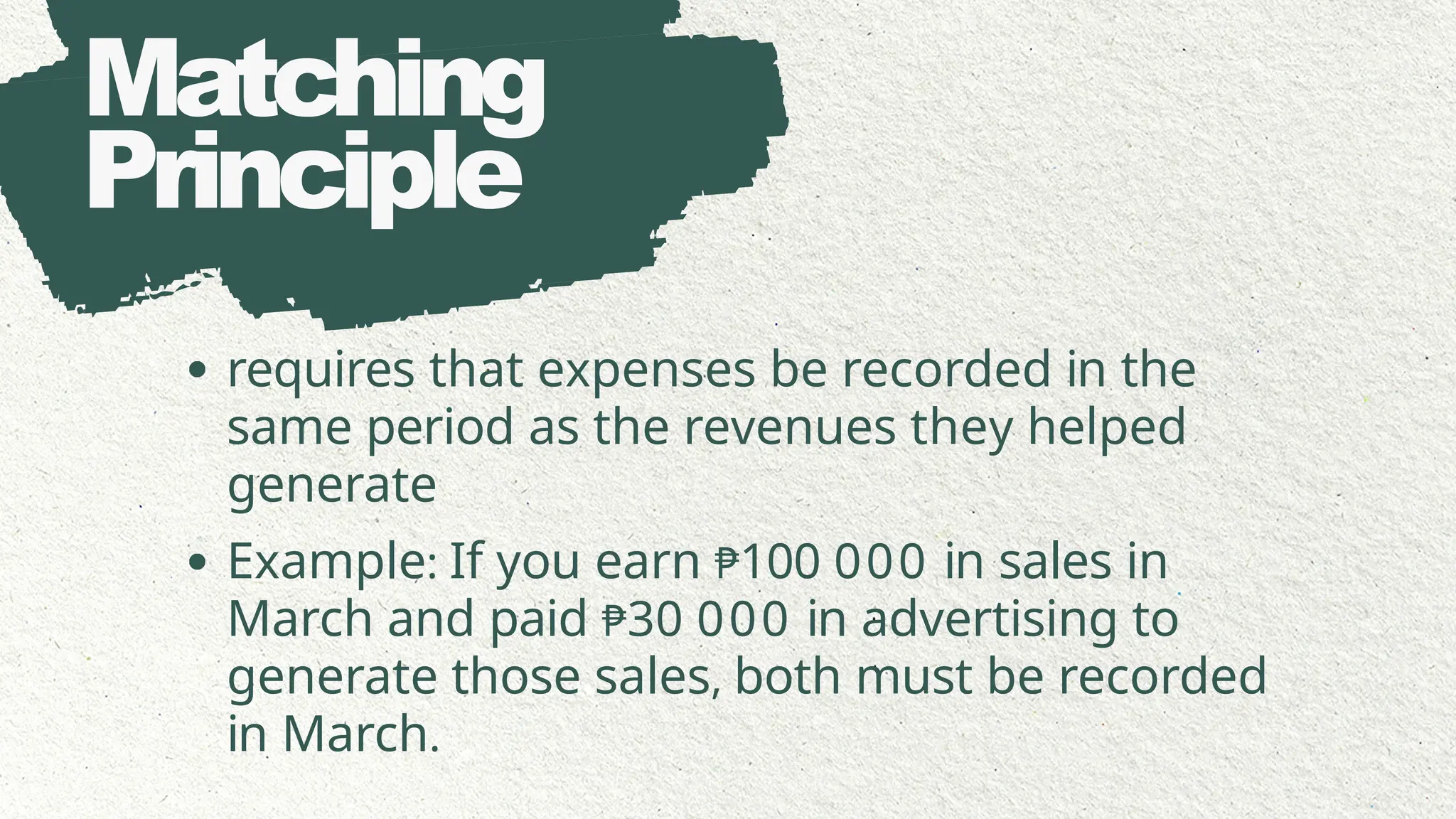

Matching

Principle

requires that expensesbe recorded in the

same period as the revenues they helped

generate

Example: If you earn ₱100 000 in sales in

March and paid ₱30 000 in advertising to

generate those sales, both must be recorded

in March.

5.

Use of

Judgment &

Estimates

Accountantsoften make reasonable

estimates when exact data isn’t available

and must exercise professional judgmentin

areas like depreciation, bad debts, or

inventory valuation.

Example: Estimating useful life of

equipment

or expected percentage of

uncollectible receivables.

6.

Prudence

(Conservatism

)

requires accountants toanticipate no profit

but recognize all possible losses

Example: If there's a chance that inventory

is obsolete, it should be written down even

if the loss hasn’t occurred yet.

7.

Substance

Over Form

Transactions mustbe recorded according

to their true economic substance, not just

their legal form.

Example: A lease that effectively

transfers ownership should be recorded

as an asset, even if legally it’s a rental.

Time Period

Assumption

assumes thata business's financial life can be

divided into specific, consistent periods

Example: Companies prepare monthly

income statements to monitor short-term

performance.

IFRS & PFRS

InternationalFinancial Reporting Standards

(IFRS) - global standards developed by the

International Accounting Standards Board

(IASB)

Philippine Financial Reporting Standards

(PFRS) - the Philippine version of IFRS,

adopted and issued by the Financial

Reporting Standards Council (FRSC)

#1 These are the “rules of the game” that guide how accountants record and report financial information. Just like sports has rules to make the game fair, accounting also has principles to make financial reports accurate and reliable.

#3 Accrual Accounting

Revenues are recorded when earned, and expenses when incurred, not when cash is received or paid.

Example: If you give a service in December but get paid in January, the income is still recorded in December.

Why? To show the real performance of the business in the correct time period.

#4 Matching Principle

Expenses should be recorded in the same period as the revenues they helped generate.

Example: Sales in March = ₱100,000, Advertising in March = ₱30,000 → Both are recorded in March.

👉 This helps us see the true profit.

#5 Judgment & Estimates

Accountants sometimes use reasonable estimates when exact data isn’t available.

Example: Estimating bad debts, or the useful life of equipment.

#6 Prudence (Conservatism)

“Expect losses, not profits.”

Possible losses are recognized early, but profits are only recorded when certain.

Example: If inventory might become obsolete, write it down even before the loss happens.

#7 Substance Over Form

Record transactions based on their real meaning, not just legal form.

Example: A lease that acts like ownership should be recorded as an asset.

#8 Going Concern Assumption

Assumes the business will continue operating in the future and not shut down soon.

#9 Accounting Entity Assumption

Business is separate from the owner.

Example: The owner’s grocery expenses are not part of business expenses.

#10 Time Period Assumption

A business’s financial life can be divided into periods (months, quarters, years).

Example: Monthly income statements.

#11 GAAP, IFRS & PFRS

GAAP – Generally Accepted Accounting Principles, used in preparing statements.

#12 IFRS – International Financial Reporting Standards, global rules.

PFRS – Philippine version of IFRS.