Downloaded 42 times

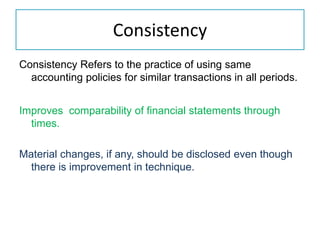

Accounting assumptions are fundamental principles that underlie the preparation of financial statements, which include the going concern, consistency, and accrual concepts. These assumptions ensure logical consistency in recording transactions and adherence to established accounting practices. They help improve the comparability of financials over time and address expected future cash transactions.