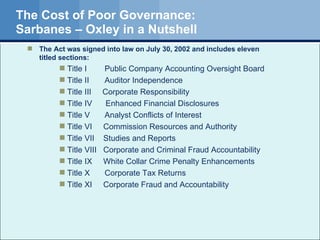

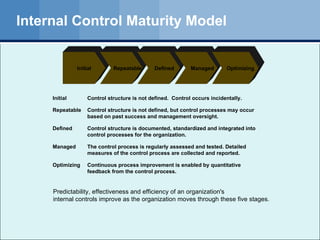

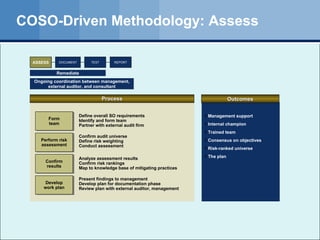

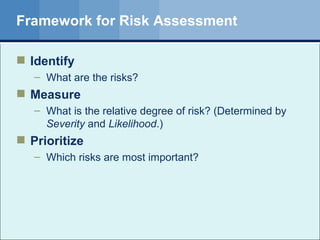

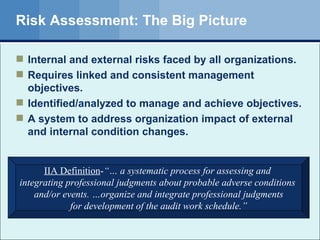

The document discusses the significance of governance in the context of the Sarbanes-Oxley Act, emphasizing the need for strong internal controls to mitigate risks arising from human behavior. It highlights the evolution of governance frameworks, the responsibilities of management, and the financial implications of compliance. The document also outlines a risk-based approach to governance, emphasizing ongoing monitoring and the necessity for continuous improvement in control processes.