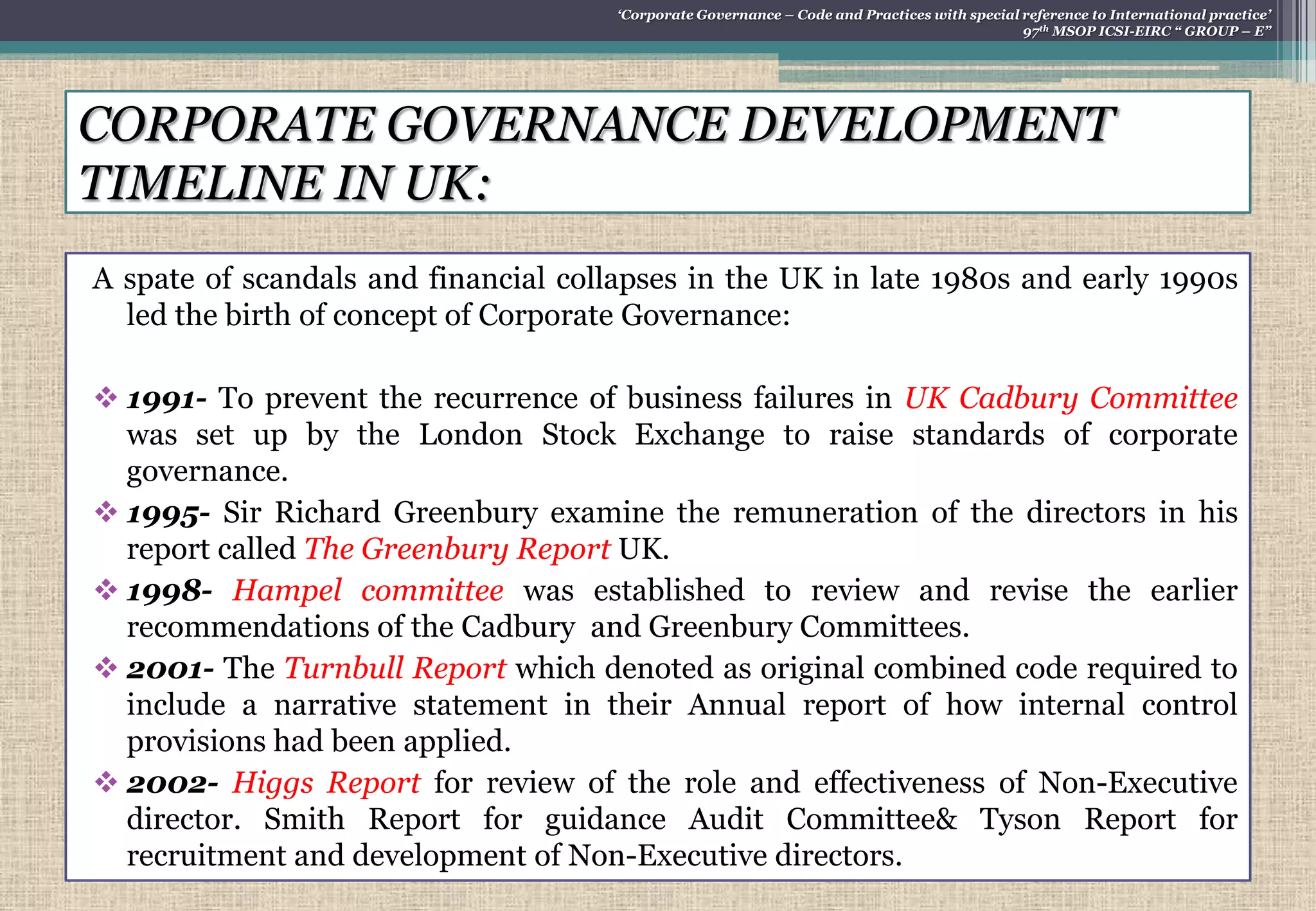

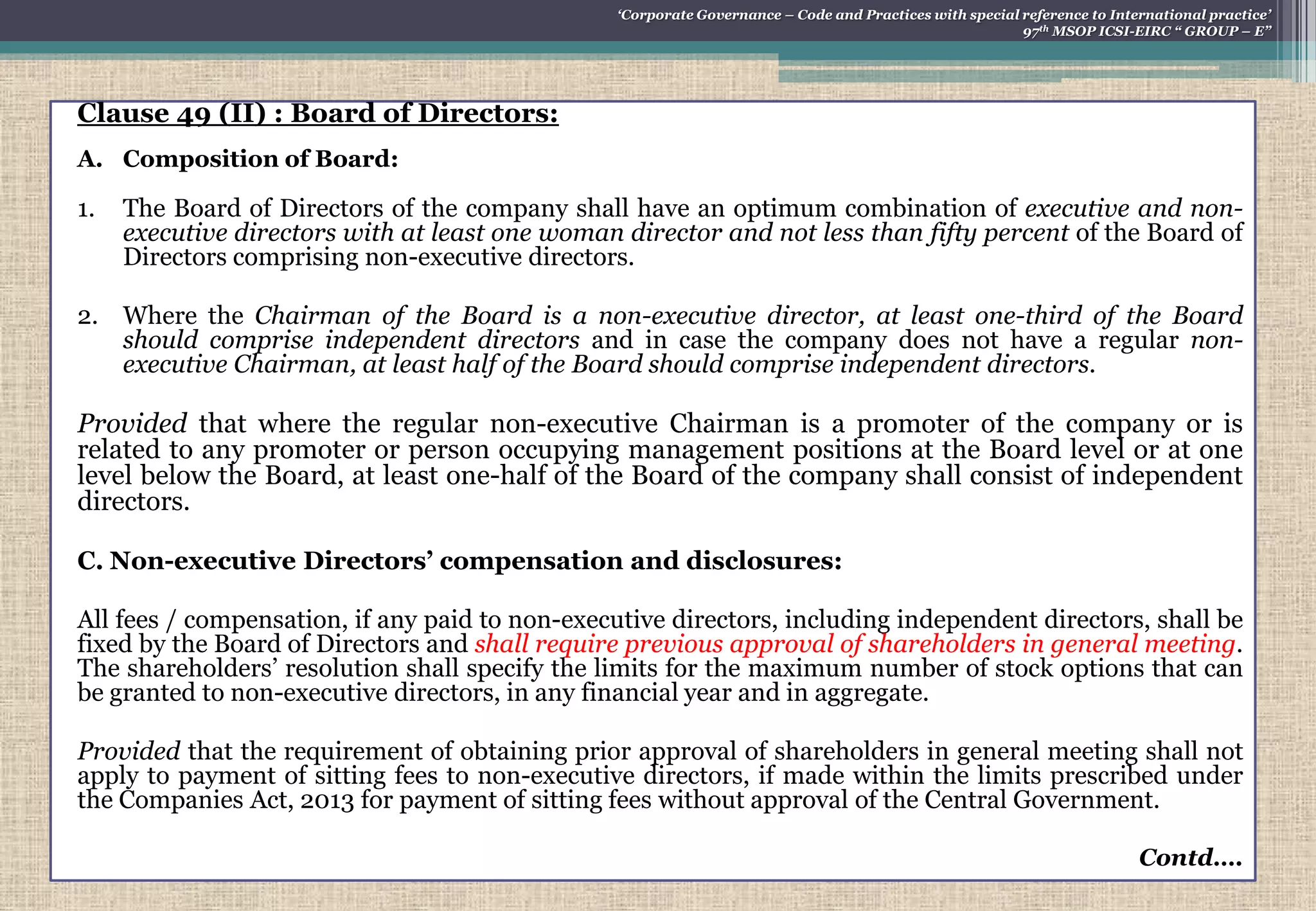

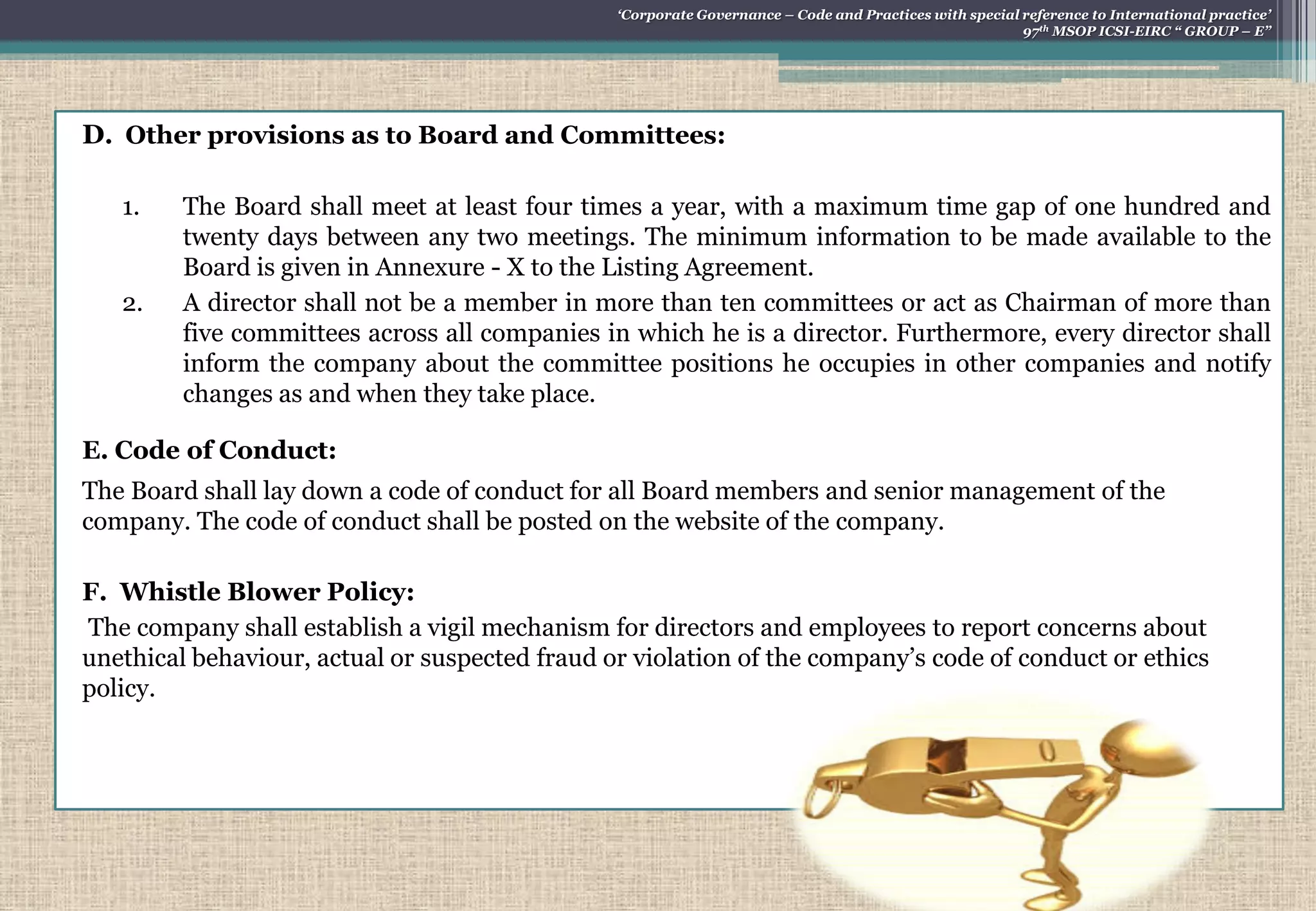

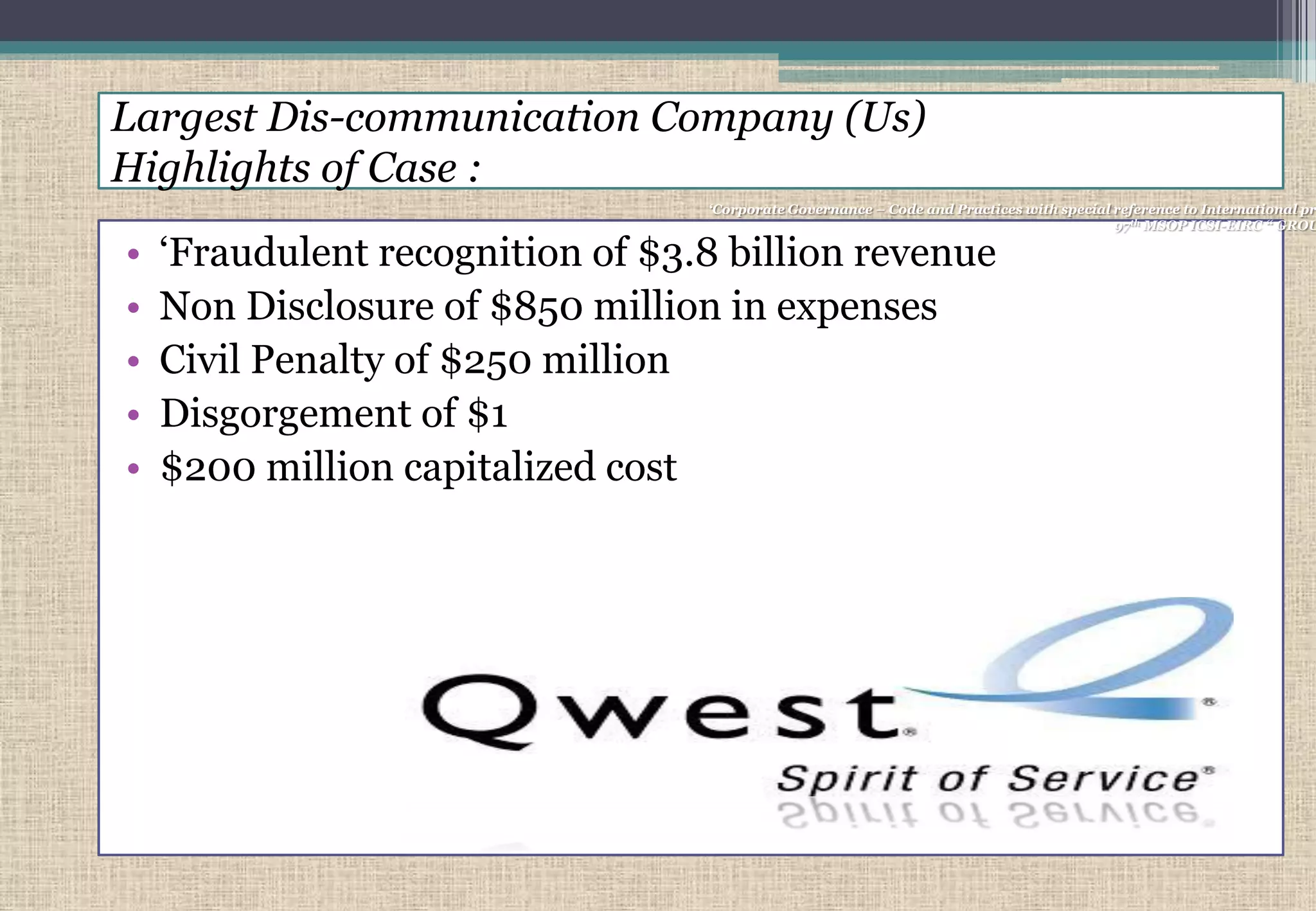

The document discusses corporate governance principles and practices with reference to international standards. It provides definitions of corporate governance, lists its key principles like sustainable stakeholder development and social responsibility. It outlines the four pillars of corporate governance as accountability, transparency, responsibility and fairness. The document then traces the historical development of corporate governance codes in the US, UK and India and highlights various committee recommendations that shaped governance standards. Finally, it discusses key aspects of Clause 49 of the Indian listing agreement on board composition, disclosure and transparency requirements.