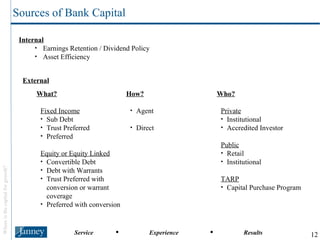

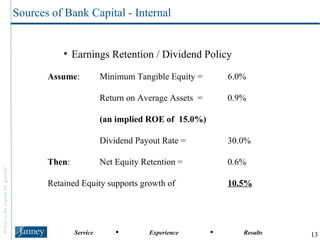

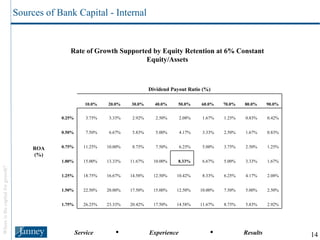

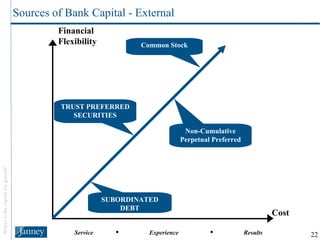

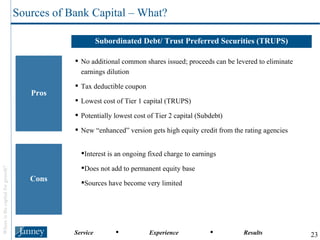

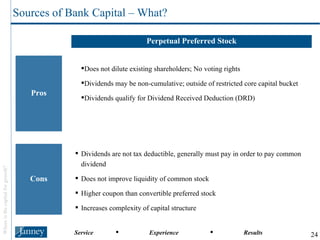

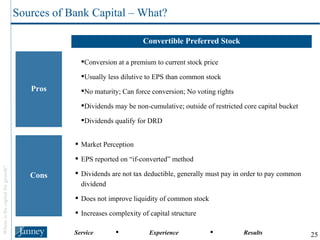

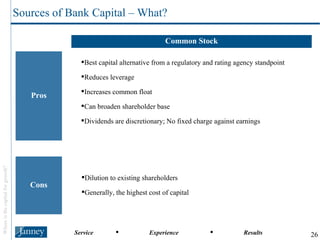

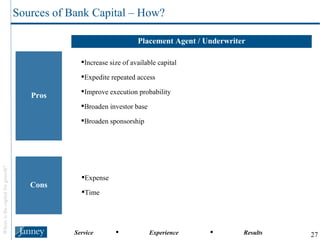

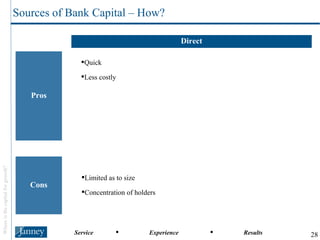

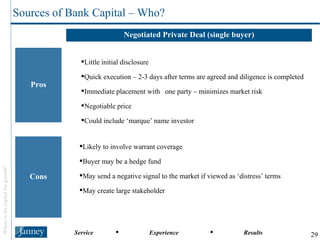

The document discusses various sources of capital for banks, both internal and external. It covers retaining earnings, asset efficiency, and dividend policy as internal sources, as well as fixed income, trust preferred securities, preferred stock, convertible preferred stock, and common equity as external sources. It also discusses placement agents, private placements, PIPE transactions, and public offerings as methods to raise external capital.