Downloaded 65 times

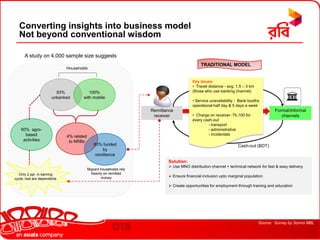

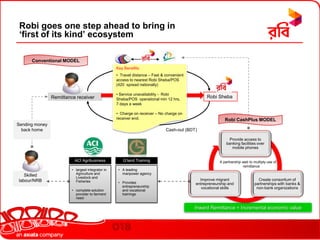

This document summarizes Robi CashPlus, a mobile money service in Bangladesh that aims to improve the lives of migrant families through remittances. The key points are: 1) Robi CashPlus allows migrant workers to easily send money back home through Robi's nationwide network, benefiting families who previously faced barriers like travel distances and bank operating hours. 2) The service forms partnerships to promote productive spending of remittances on agriculture through ACI Agribusiness and vocational skills training through Greenland Group. 3) By integrating remittances with financing, goods, and services, Robi CashPlus creates an ecosystem to multiply the economic impact of money sent home by migrant workers.