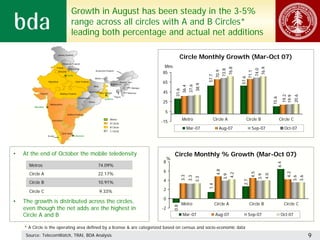

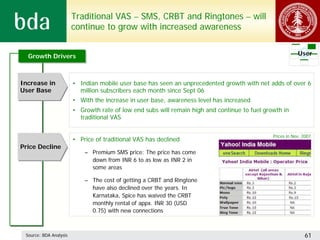

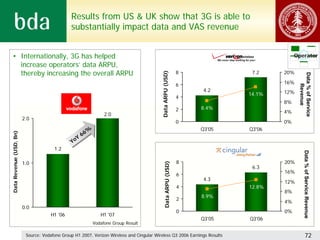

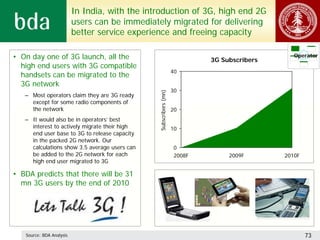

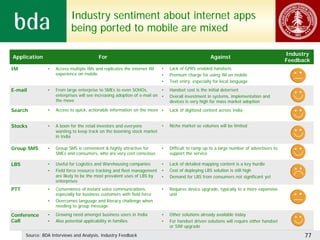

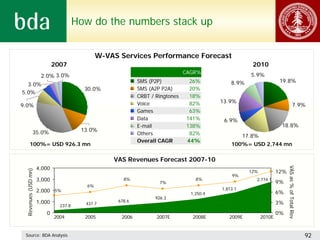

The document provides an overview of the future of mobile value-added services (VAS) in India. It notes that India's mobile subscriber base has grown explosively to over 217 million subscribers as of October 2007, though penetration is still only 23% of the population. Traditional VAS has been SMS-based with Bollywood and cricket as major content drivers, contributing around 7% of wireless revenues. However, VAS growth faces challenges including revenue sharing between operators and providers, lack of payment mechanisms, low awareness, and lack of localized content and devices. The outlook projects addressing these challenges could push VAS revenues to $2.7 billion by 2010, with traditional VAS declining and services like mobile music and internet applications growing.

![Ba Mvas In India Research Report 10 07[1]](https://cdn.slidesharecdn.com/ss_thumbnails/bamvasinindiaresearchreport10071-1231773260184145-2-thumbnail.jpg?width=640&height=640&fit=bounds)