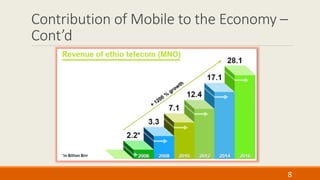

Downloaded 23 times

![Mobile Sector

The market structure of Ethiopian communication sector is monopoly. ethio telecom is the

monopoly network operator(MNO).

It describes itself as an ‘Integrated Telecommunication Solutions Provider’. It provides mobile,

fixed, internet services.

ethio telecom launched

⁻ 2G (GSM900) in April 1999,

⁻ 3G (WCDMA & HSPA 2100) in January 2009, and

⁻ 4G (LTE 1800) in March 2015

Its aggregate mobile network area coverage has now reached 92% of the country. The population

coverage is even higher than this and is close to 100%.

The subscriber number has been growing at a rate of 49% CAGR for the last decade. It reached

38.8m in 2015 [National Bank of Ethiopia]

4](https://image.slidesharecdn.com/mobileinethiopia1-161216084935/85/Mobile-in-ethiopia-1-4-320.jpg)

![The Mobile Ecosystem

There is no strong collaboration and coordinated (symbiotic)

evolution among the mobile ecosystem components. However, the

following businesses could be considered constituting the

ecosystem.

Following the MNO, The second most visible component of the

mobile ecosystem are handset manufacturers or more precisely

assemblers.

There are now 8 mobile assembly plants in the country, out of

which three-Tecno [TV Report of Expansion] , Tana and Smadl- are

the dominant ones.

Companies that specialize in Software development are less than

500. Further, those that have proven mobile native or hybrid

development capabilities are even less.

An emerging trend of collaboration between handset manufacturers

and developers is the mobile App challenge like the one sponsored

by Tecno.

mobile retailers: according to the operator there are 75,000 device

and accessory retailors all over the country.

6](https://image.slidesharecdn.com/mobileinethiopia1-161216084935/85/Mobile-in-ethiopia-1-6-320.jpg)

![Mobile Financial Services

Financial services of any kind are restricted to financial

institutions only (meaning banks and microfinance

institutions)

However, according Directive No. FIS /01/2012[NBE] which

regulates ‘Mobile and Agent Banking Services’, financial

institutions can procure the technological services from a

third party and provide mobile banking

As a result some banks have their own mobile banking

service while others use a service provider to provide

mobile banking service.

There are now two successful mobile banking technology

service providers: M-Birr and HelloCash.

M-Birr plans to reach #### agents and 1.5 million active

accounts by 2016

HelloCash estimates to build a customer base with active

accounts of 2-3 million by 2016 and 10 million by 2018.

11](https://image.slidesharecdn.com/mobileinethiopia1-161216084935/85/Mobile-in-ethiopia-1-11-320.jpg)

![mAgriculture

Various technologies are implemented in the agriculture

sector that are based on mobile. To enhance productivity,

and benefit smallholder farmers.

One developed by the exchange market called ECX has

been lauded as successful by several experts.

This application uses mobile IVR, SMS and website to

provide live market information to farmers.

About 60,000 farmers use the App daily [GSMA mFarm].

Overall, 1.365 million farmers have subscribed to the

service.

The App is initiated and developed by ECX in cooperation

with USAID & Melinda Gates Foundation.

It aims to benefit farmers set their price right and avoid

middlemen. Earning good price is also expected to be an

effective incentive in enhancing farm productivity.

13](https://image.slidesharecdn.com/mobileinethiopia1-161216084935/85/Mobile-in-ethiopia-1-13-320.jpg)

![Other Mobile Services

MGOV

Mobile Apps for 20 government offices were specified

by the Ministry of Communication and Information

Technology and a contract awarded to a private

company called Avado.

This is a decisive move by the government to employ

the advantage of mobile prevalence for the benefit of

citizens.

Some of the existing eGov services also function on

mobile. But dedicated mobile Apps have the advantage

of better performance both on mobile and desktop.

Developments of mobile governance or mGov is bound

to expand in the future.

To produce impact on the socioeconomic progress of

the country, the government needs to ensure reliable

operation of the platforms & avoid frequent

unavailability.

MLEARNING / MEDUCATION

The governments main thrust has been to ensure 100%

basic education enrollment through traditional school

expansion. To date the nation has achieved basic

education net enrollment of 80%+.[Ministry of Education]

Thus there is no big scale mLearning development.

However, many private schools and the government use

several mobile based education management services. In

addition, evaluation of the education sector lists some

major challenges such as teacher quality, teaching material

shortage, etc. Mobile can help overcome this problems.

Thus the government should give due attention to

mLearning services development.

The national examination agency has for example

deployed an SMS App for result notification. That has been

particularly useful to people in remote areas to easily and

instantly know their results and get ready to the next level.

14](https://image.slidesharecdn.com/mobileinethiopia1-161216084935/85/Mobile-in-ethiopia-1-14-320.jpg)

![Other Mobile Services

MHEALTH

A number of services are initiated in the health sector

which are either public sponsored or market oriented

One good example is the maternal advise provided

through mobile. This pilot project was initiated by

Dutch Health[e]Foundation and TTC Mobile in

cooperation with Ministry of Health and Medical

Professional Associations. Initially, it planned to reach

4,000 expectant mothers.

Maternal health is one of the priority policy areas

because of international commitments and national

goals.

Market oriented health advisory services provide

medical advise for a certain charge by calling with a

short code 8896 on the mobile. One example is

HelloDoctor.

15](https://image.slidesharecdn.com/mobileinethiopia1-161216084935/85/Mobile-in-ethiopia-1-15-320.jpg)

Ethiopia has a developing mobile sector that, while an early adopter of telecommunication technologies, lags behind many African nations in mobile ecosystem development and digital economy growth. The majority of mobile services are provided by the state-owned Ethio Telecom, which has achieved significant coverage but maintains a monopoly that limits competition and innovation. The mobile banking sector shows promise, with initiatives like m-birr and hellocash, but challenges remain in fostering a robust digital culture and collaboration among ecosystem participants.