Download to read offline

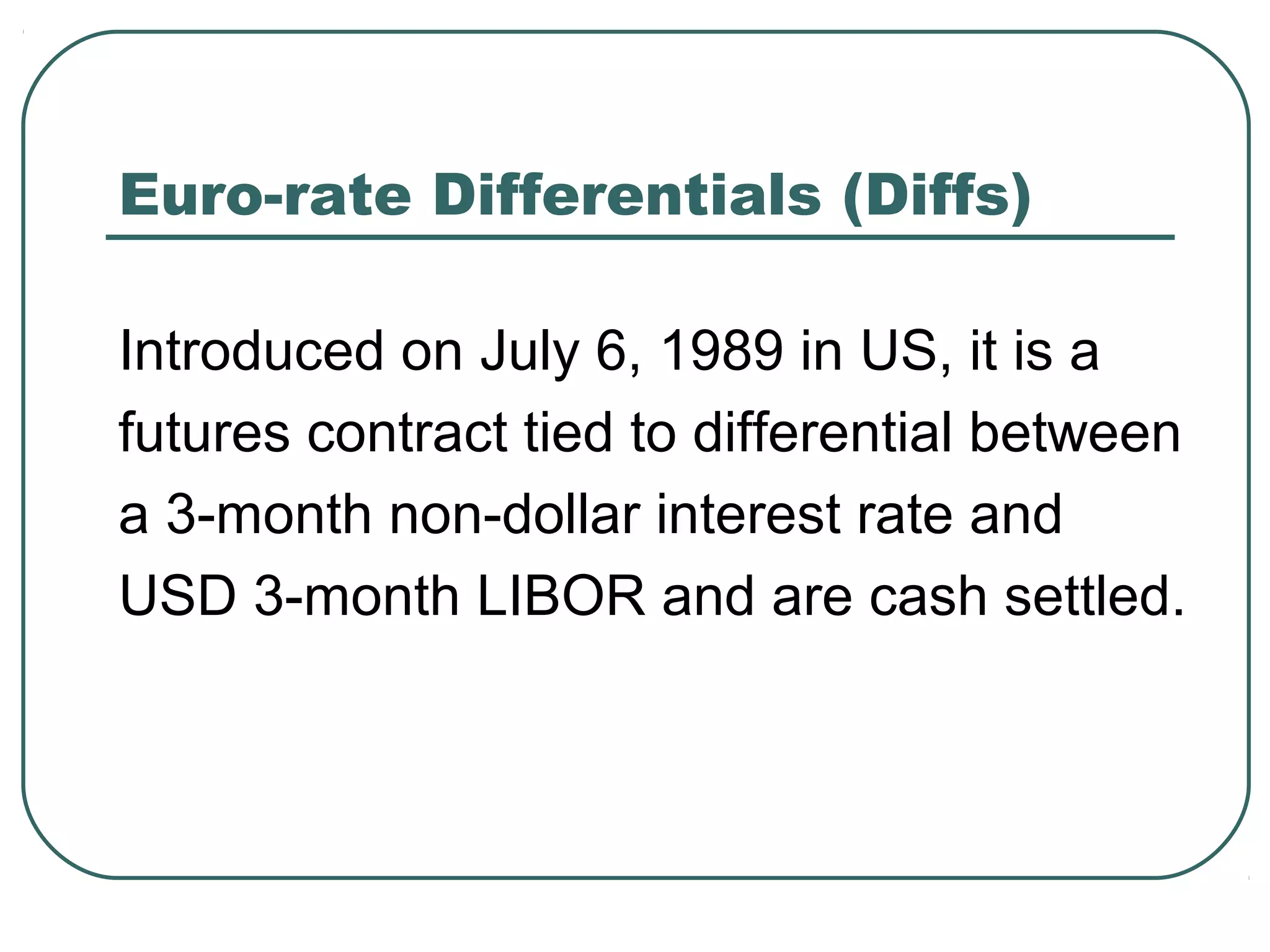

![Hedging Interest Rate Risk

Hence, FVh= FVc × [PV01c / PV01h] × βy

= 50 × [0.096585 / 0.098891] × 0.45

= Rs.21.98 Crores

If FV of a single T-Bond Future is Rs.10,00,000

then, Number of Futures (Nf) = 21.98/0.1

= 219.8 Futures](https://image.slidesharecdn.com/8-150725171025-lva1-app6891/75/8-futures-and-forwards-11-2048.jpg)

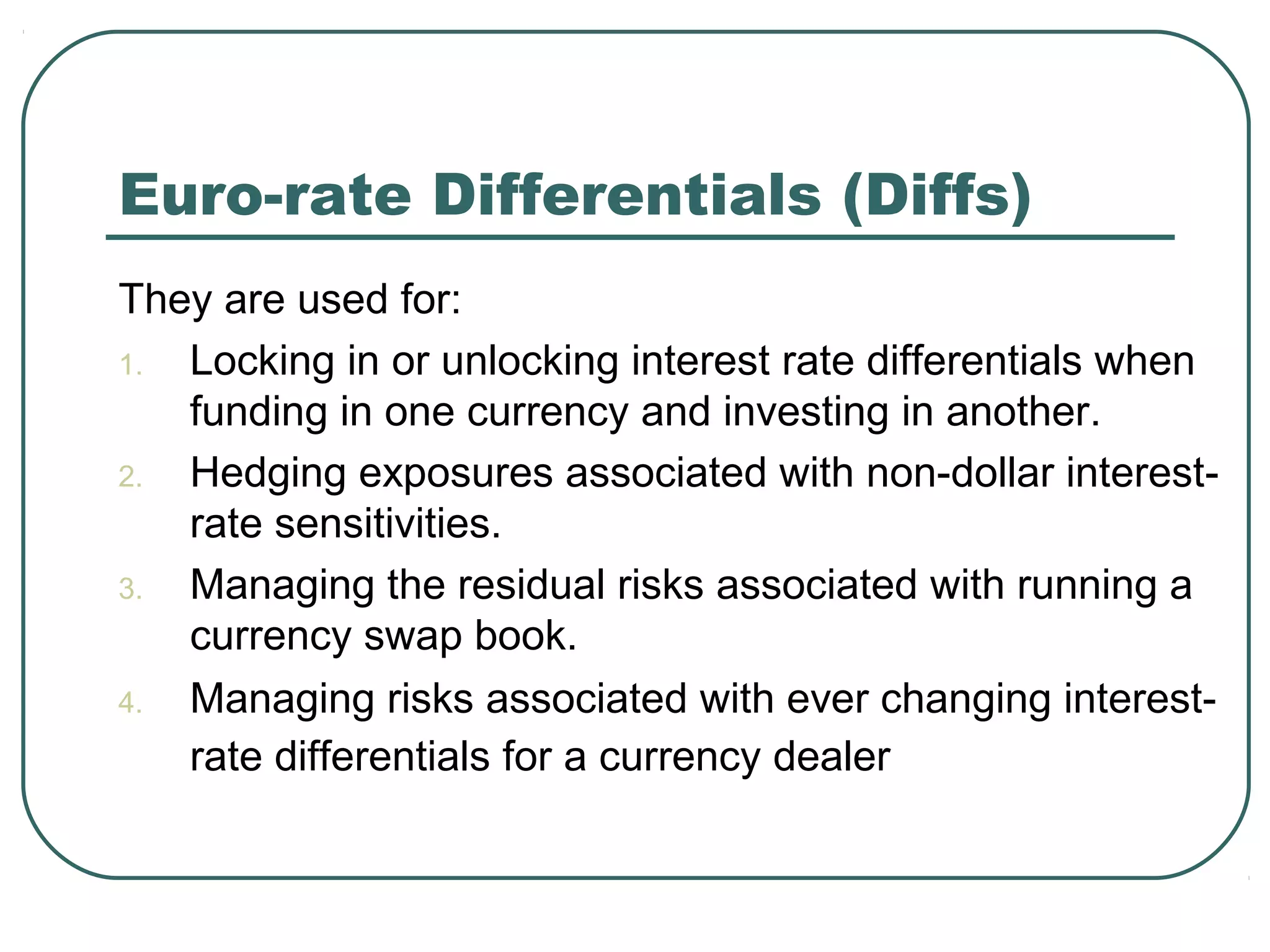

![Stock Index Arbitrage: Illustration

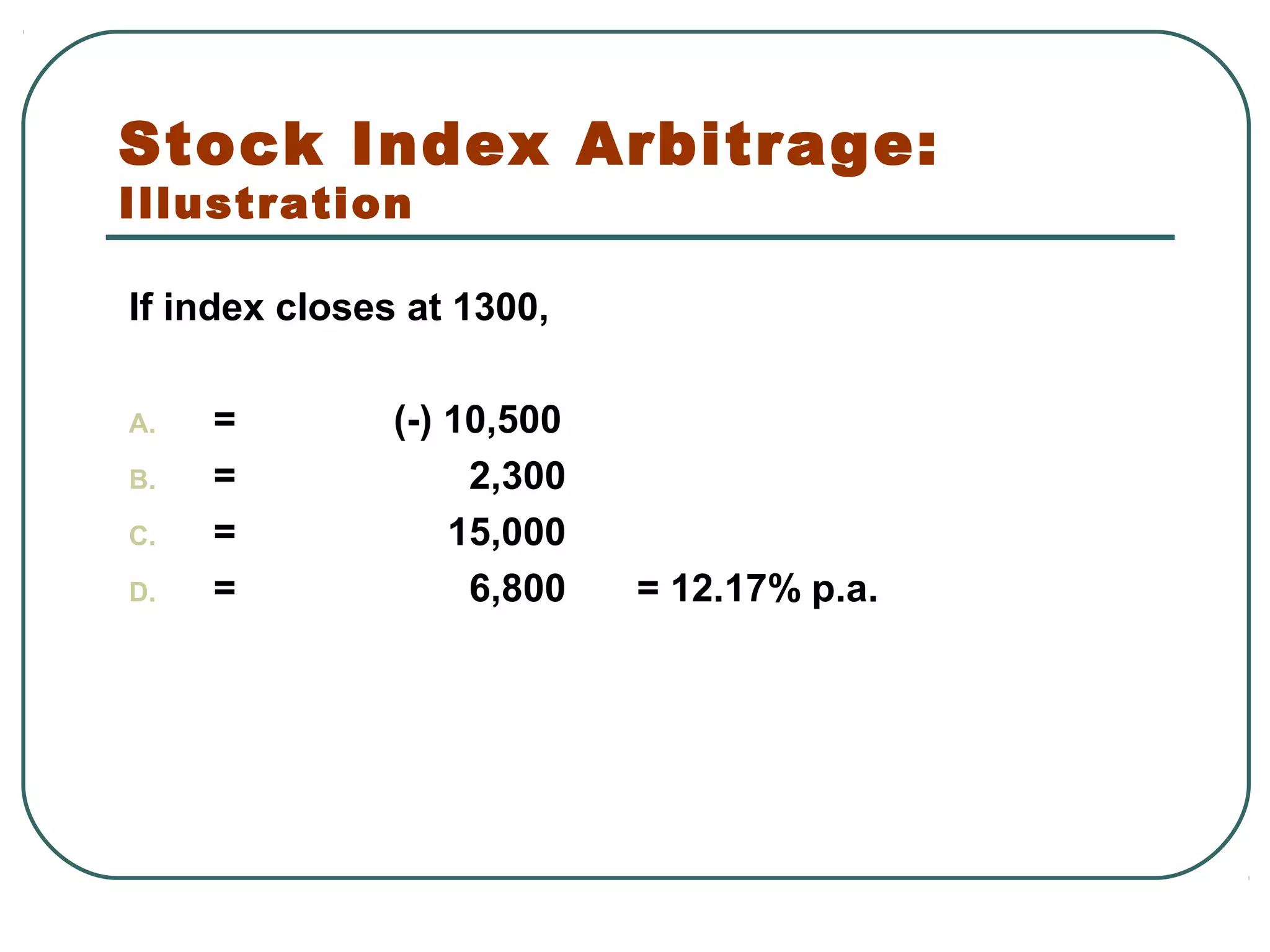

Fair price of index future

FC = IC + (RF – D)

= 1150 + [(1150×0.10×0.5)-(1150×0.04×0.5)]

= 1150 + 34.5 = 1184.5 (hence it is overpriced)

Investor can buy a portfolio identical to index and

short-sell futures on index.

If index closes at 850 on expiration date, then

A. Profit on short sale of futures (1195 – 850) ×100 = Rs.34,500

B. Cash Div recd on port. (1150 × 0.04 × 0.5 × 100 = Rs. 2,300

C. Loss on sale of port. (1150 – 850) ×100 = ( - ) Rs.30,000

D. Net Profit = 34,500 +2,300 – 30,000 = Rs.6,800

E. Half yearly return = 6800 ÷ (1150×100)=0.0591 = 5.91%

F. Annual return (1.0591)2

– 1 = 0.1217 = 12.17%](https://image.slidesharecdn.com/8-150725171025-lva1-app6891/75/8-futures-and-forwards-30-2048.jpg)

Futures and forwards are contracts that require deferred delivery of an underlying asset or cash settlement at a future date. A future is traded on an exchange and has standardized terms, while a forward is a customized over-the-counter contract. Forwards are useful when futures do not exist for a commodity or financial or when standard futures terms differ from needs. Euro-rate differentials futures contracts are tied to interest rate differentials between currencies and used to hedge currency exposures. Foreign exchange agreements allow hedging of exchange rate movements through a single cash settlement without a currency swap.