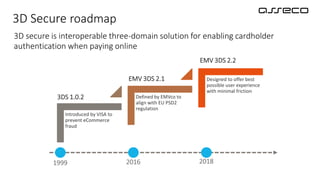

The webinar discusses the benefits and challenges of 3D Secure and highlights new features in version 2.2 that aim to improve the user experience. Key points include:

- 3D Secure provides benefits like liability shift but can create friction for cardholders during online transactions.

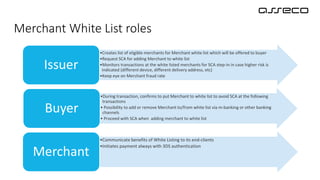

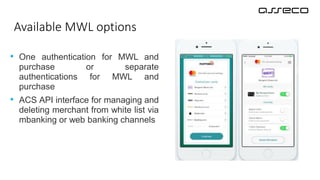

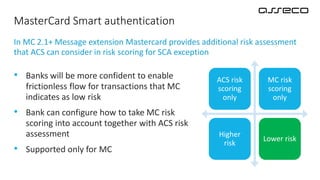

- Version 2.2 focuses on minimizing user actions and authentication through tools like merchant white listing, risk-based exemptions, and decoupled authentication.

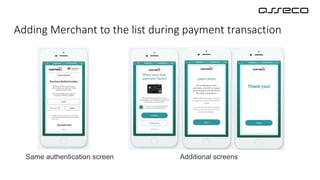

- Merchant white listing allows cardholders to add trusted merchants to their own list and skip authentication for future purchases from those merchants.

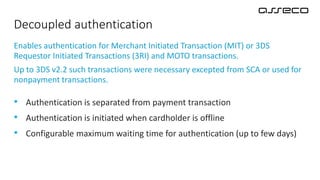

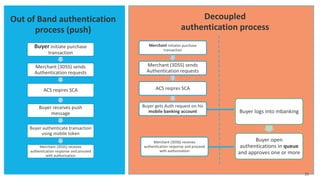

- Decoupled authentication separates authentication from payment, allowing it to occur offline through mobile notifications within a configurable time window.

![谷歌留痕技术教程[ 𝙩𝙤𝙥 𝟮𝟯𝟯. 𝙘 𝙤𝙢 ]](https://cdn.slidesharecdn.com/ss_thumbnails/top233-260130173900-2eb784f9-thumbnail.jpg?width=640&height=640&fit=bounds)

![20260201 [FOSDEM] gomodjail - library sandboxing for Go modules.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/20260201fosdemgomodjail-librarysandboxingforgomodules-260201225659-76609ec4-thumbnail.jpg?width=640&height=640&fit=bounds)