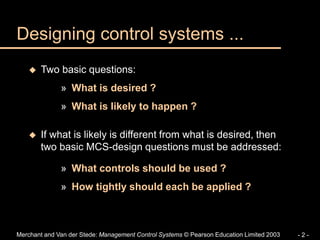

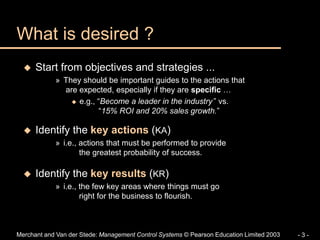

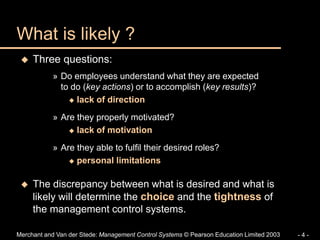

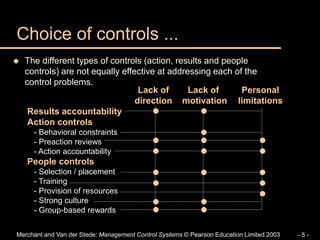

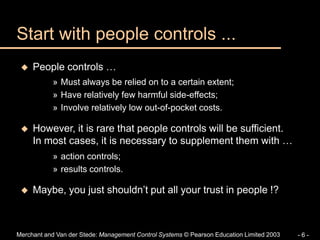

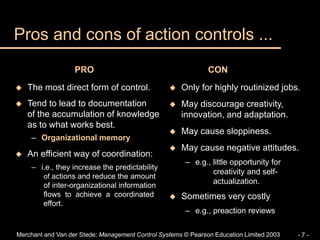

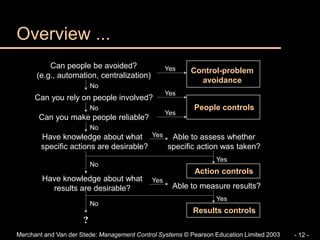

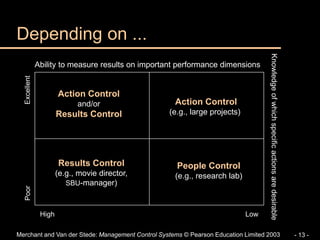

The document discusses designing and evaluating management control systems (MCS). It addresses two questions when designing controls: what is desired and what is likely to happen. If what is likely differs from what is desired, controls and their tightness must be determined. People, action, and results controls are examined in terms of addressing lack of direction, motivation, and personal limitations. The choice of controls depends on being able to measure results and knowing which actions are desirable. Controls also evolve as firms grow toward increased formalization and information systems. The focus should remain on impacts of controls on employee behavior.