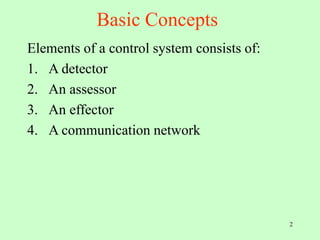

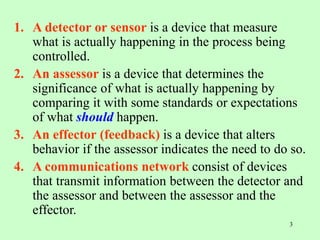

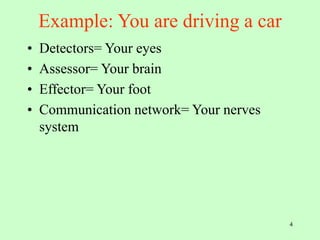

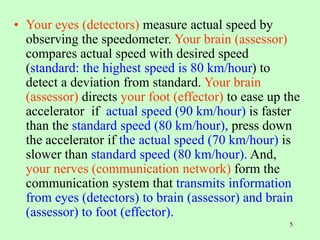

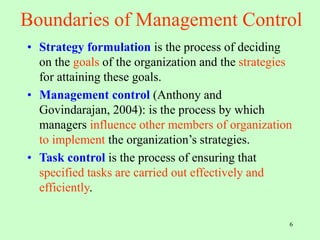

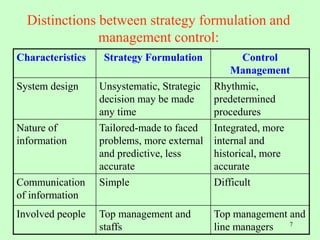

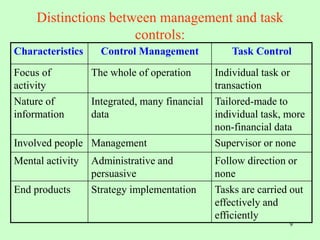

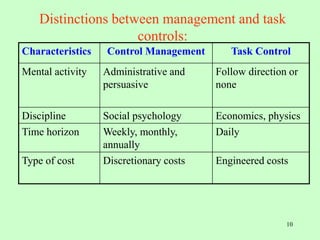

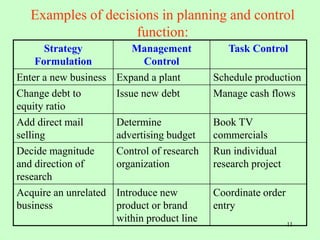

The document outlines the fundamental components of management control systems, including detectors, assessors, effectors, and communication networks. It distinguishes between strategy formulation, management control, and task control, emphasizing their different focuses, processes, and time horizons. The text also provides practical examples to illustrate how these concepts are applied in real-world situations, particularly in the context of driving a car as an analogy.