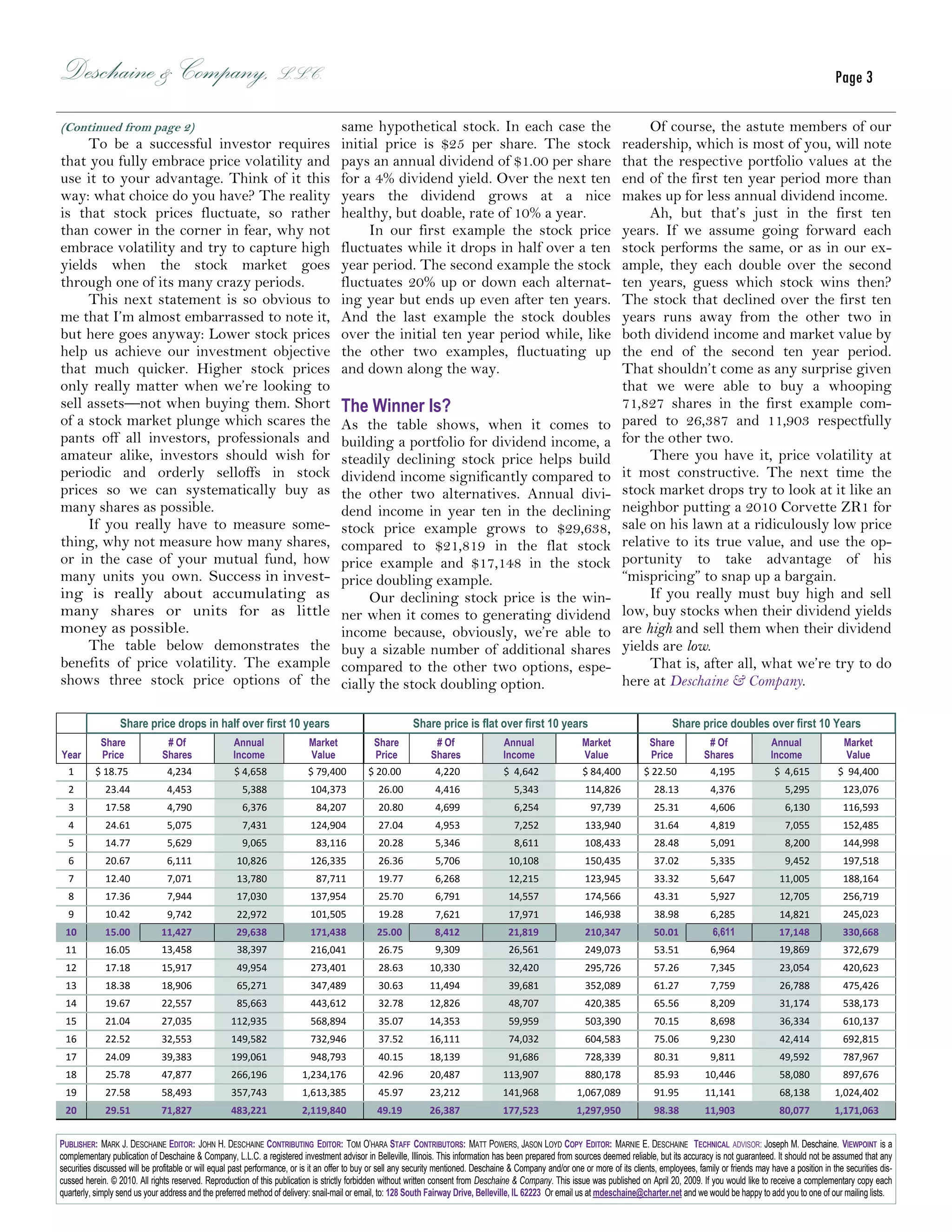

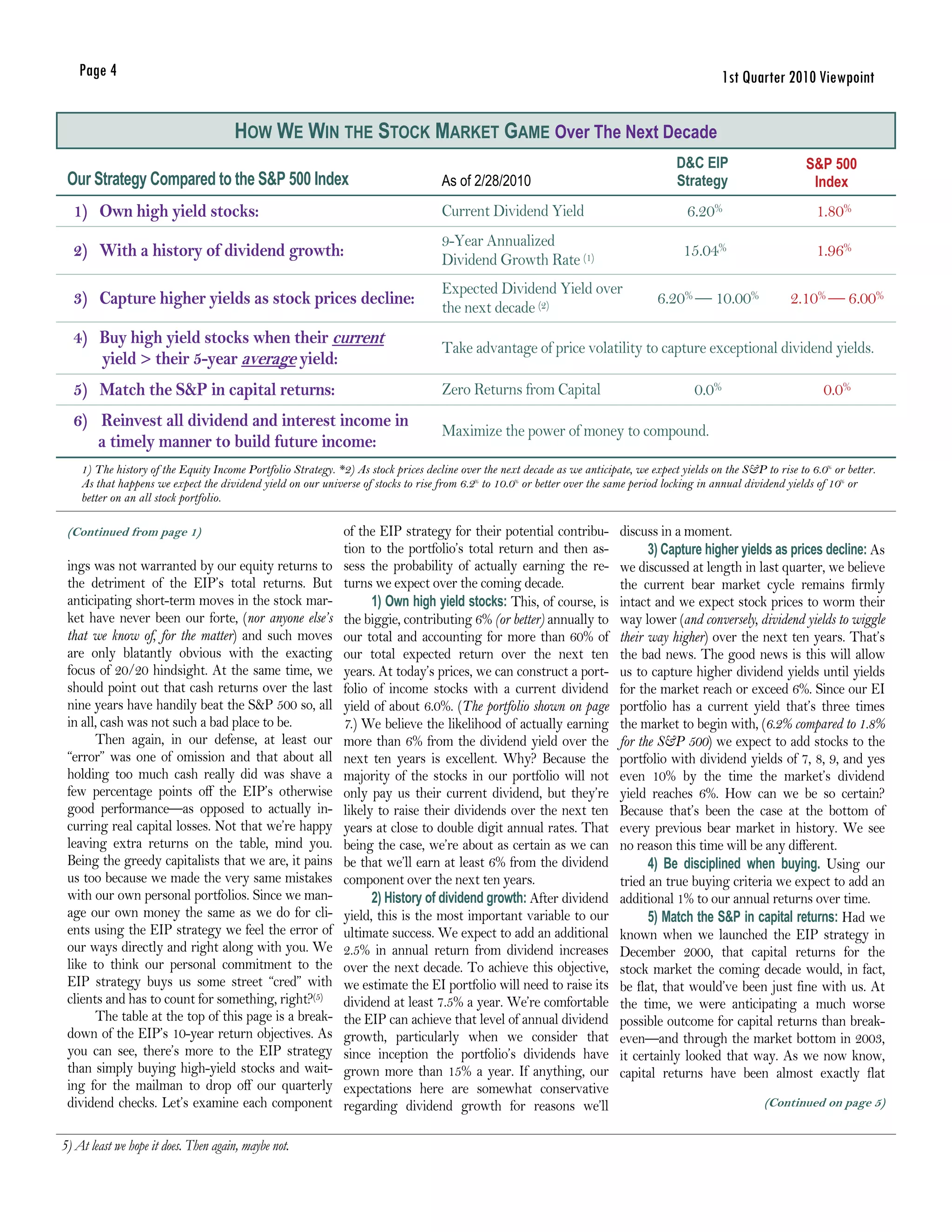

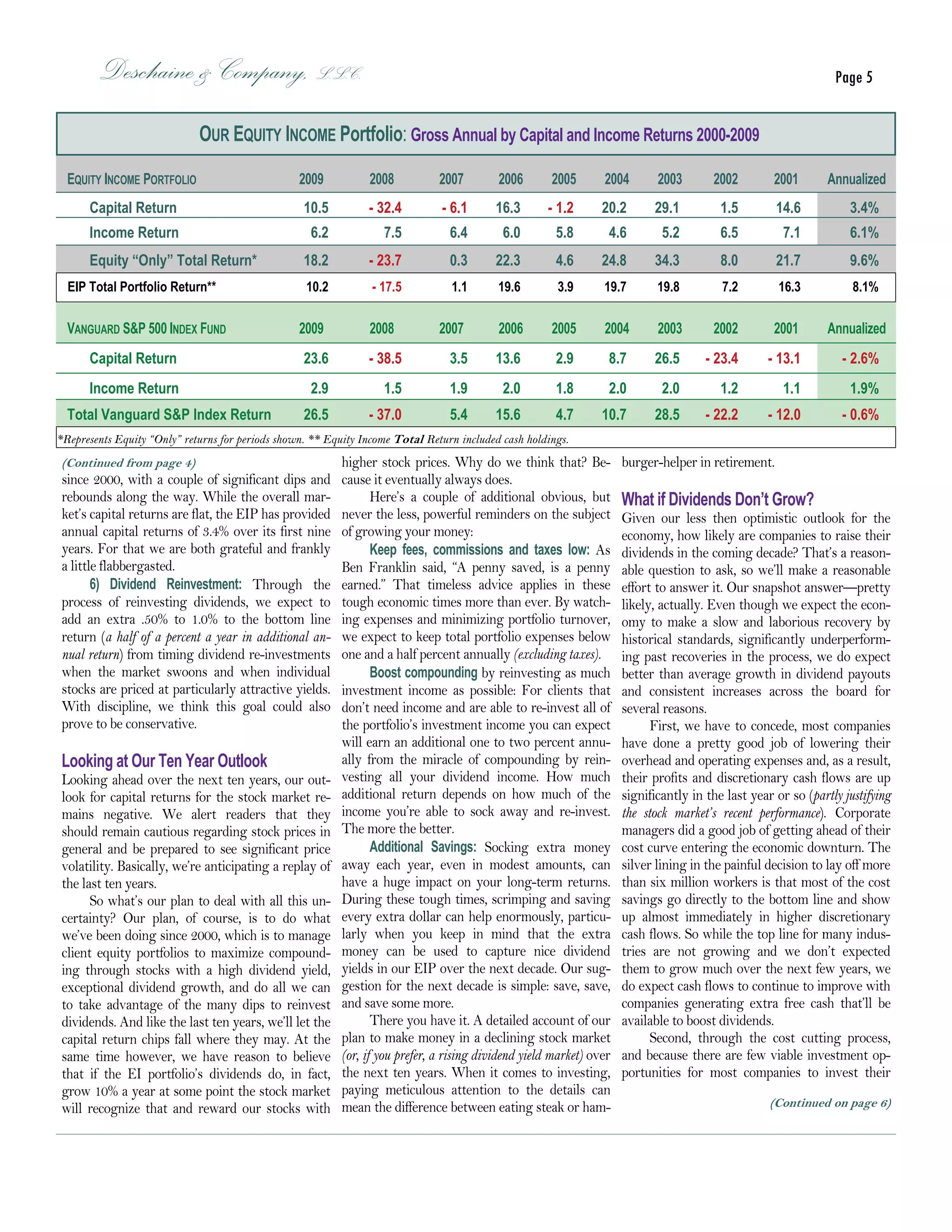

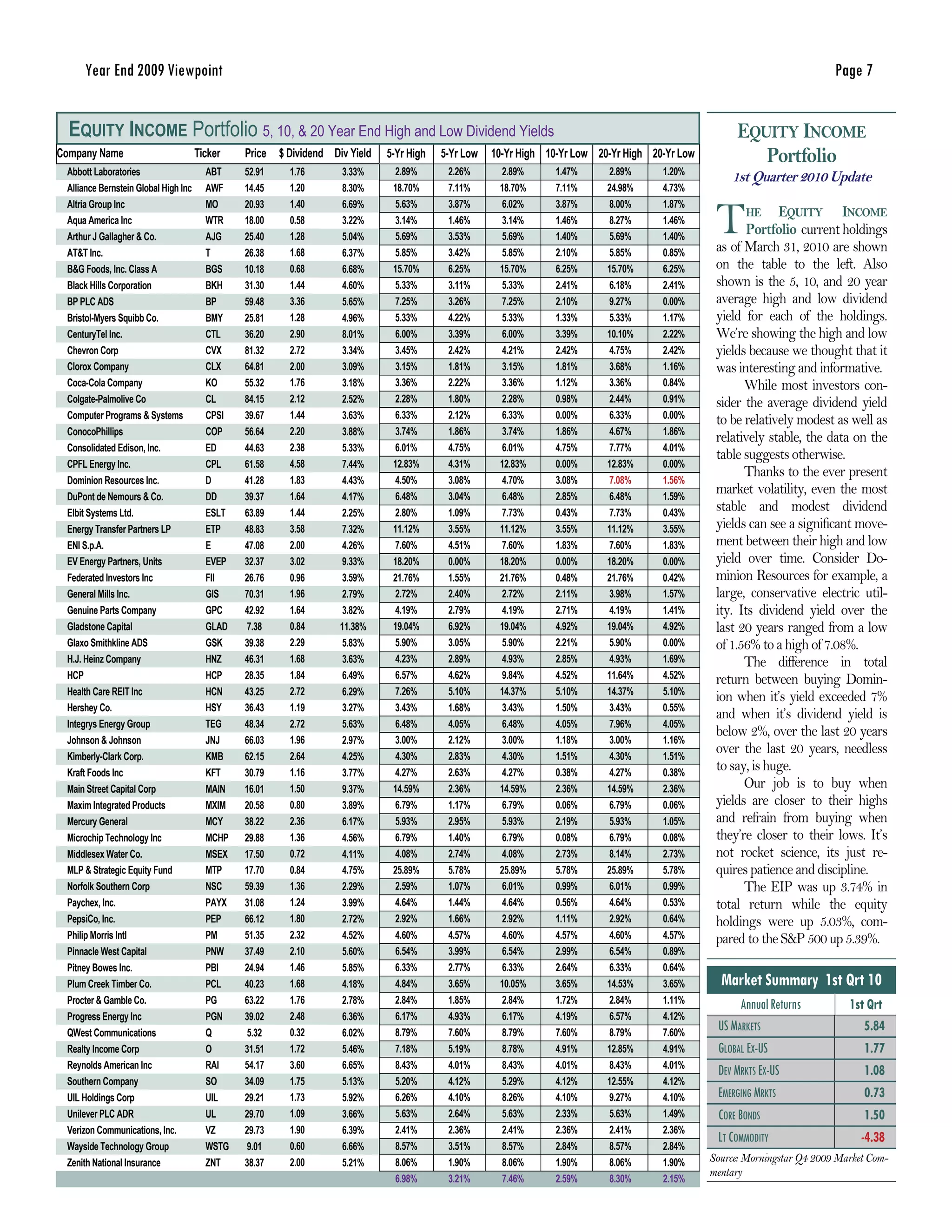

This document discusses strategies for generating income from dividend stocks in uncertain markets. It provides details on Deschaine & Company's Equity Income Portfolio, which focuses on high-yield stocks with a history of growing dividends. The portfolio has outperformed the S&P 500 index since 2001 due to strong dividend income. Lower stock prices allow investors to accumulate more shares and build dividend income faster over the long run. Price volatility should be embraced as an opportunity rather than feared.

![Wsj Reprint Back To Basics[1]](https://cdn.slidesharecdn.com/ss_thumbnails/wsjreprintbacktobasics1-12840545627925-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)