Bank of Baroda (BoB) is one of the largest public sector banks in India with over 5000 branches globally. It was founded in 1908 in Baroda, Gujarat by the Maharaja of Baroda. Over the years, BoB has expanded both within India and internationally. In 1969, it was nationalized along with 13 other major banks. Today, BoB offers a wide range of banking products and services to corporate and retail customers. It has received several awards recognizing its leadership and customer service. BoB has a strong presence both within India and globally across over 20 countries.

![ Profitability

Efficiency

ADVANTAGES OR USES OF RATIO ANALYSIS:-

Ratios are worked out to analyze the following aspects of business organization-

Simplifies the financial statements

Helps in trend analysis

Judging Efficiency and Locating Weakness

Formulating plans

LIMITATION OF RATIO ANALYSIS:-

False accounting data gives false ratios

Comparisons not possible if different firms adopt different accounting policies or operate in

different environmental conditions

Ratio analysis becomes less effective in dynamic environment.

Ratios may be misleading in the absence of absolute data.

CLASSIFICATION OF RATIOS:-

BASED ON FINANCIAL STATEMENT:-

1] Balance sheet ratio.

2] Revenue ratio.

3] Composite ratio.

BASED ON FUNCTION:-

1] Liquidity ratios.

2] Leverage ratios.

21](https://image.slidesharecdn.com/project-bob-150102233407-conversion-gate01/85/Project-on-Bank-of-Baroda-21-320.jpg)

![3] Activity ratios.

4] Profitability ratios.

5] Coverage ratios.

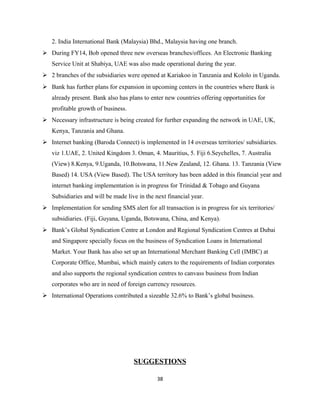

RATIO ANALYSIS OF BoB(Consolidated)

PER SHARE RATIOS

Adjusted EPS (Rs.) 114.84

Adjusted Cash EPS (Rs.) 123.41

Reported EPS (Rs.) 116.45

Reported Cash EPS (Rs.) 125.03

Dividend Per Share 0

Operating Profit Per Share (Rs.) 131.21

Book Value (Excl Rev Res) Per Share (Rs.) 881.36

Book Value (Incl. Rev Res) Per Share (Rs.) 881.36

Net Operating Income Per Share (Rs.) 942.28

Free Reserves Per Share (Rs.) 0

PROFITABILITY RATIOS

Operating Margin (%) 13.92

Gross Profit Margin (%) 13.01

Net Profit Margin (%) 10.86

Adjusted Cash Margin (%) 11.51

Adjusted Return On Net Worth (%) 13.02

22](https://image.slidesharecdn.com/project-bob-150102233407-conversion-gate01/85/Project-on-Bank-of-Baroda-22-320.jpg)

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)