Downloaded 37 times

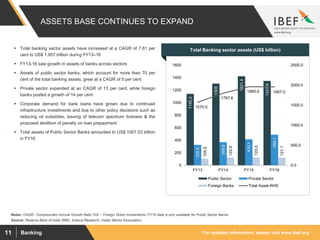

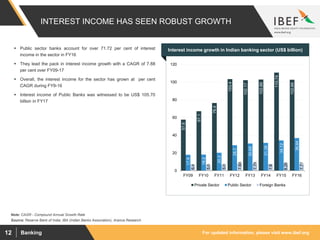

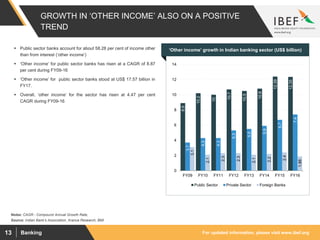

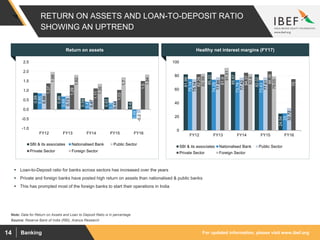

1) The Indian banking sector has grown at a healthy pace, with total assets reaching US$ 1.97 trillion in FY17 and credit off-take and deposits increasing at a CAGR of 12.38% and 10.08% respectively between FY07-17. 2) Interest income and other income have also seen robust growth for public sector, private sector, and foreign banks. Return on assets and loan-to-deposit ratios have also been trending upward across bank categories. 3) Notable trends in the banking industry include improved risk management practices, a continued