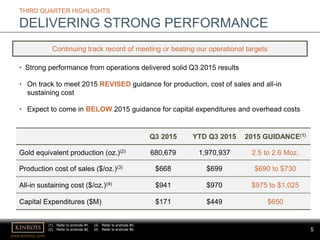

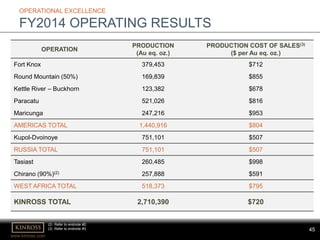

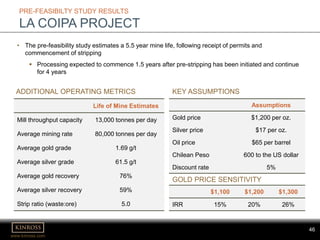

This document summarizes Kinross Gold Corporation's presentation at the CIBC Whistler Institutional Investor Conference in January 2016. Key points include: Kinross is focused on operational excellence, quality over quantity, disciplined capital allocation, and maintaining a strong balance sheet. For 2015, Kinross expects gold equivalent production of 2.5-2.6 million ounces at a production cost of sales of $690-730 per ounce and all-in sustaining costs of $975-1,025 per ounce, and capital expenditures of $650 million. Over 50% of Kinross' estimated 2015 production is from mines in the Americas.