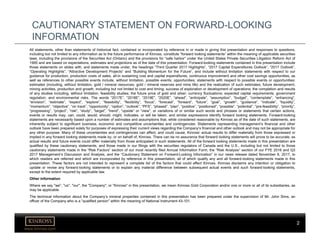

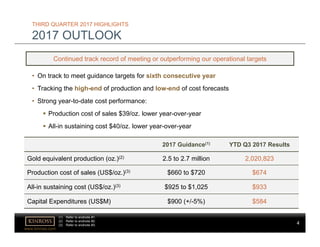

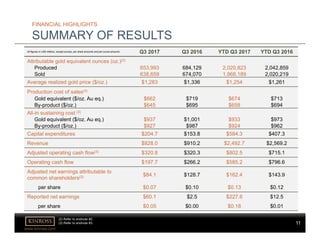

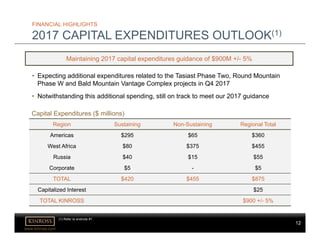

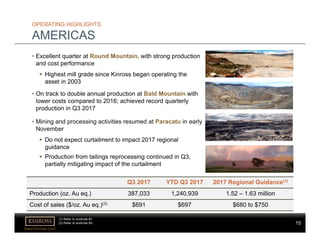

Kinross Gold Corporation reported its third quarter 2017 results. Key highlights included meeting production guidance for the sixth consecutive year and tracking at the high-end of production and low-end of cost forecasts. Strong year-to-date cost performance included production cost of sales $39/oz lower and all-in sustaining costs $40/oz lower than the previous year. Kinross is advancing the Tasiast Phase Two and Round Mountain Phase W projects following positive feasibility studies.