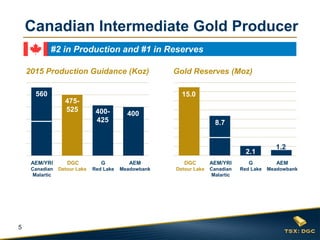

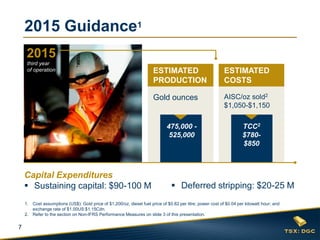

Detour Gold Corporation is a Canadian intermediate gold producer that presented at the 21st Annual Canada Mining Conference. In 2015, Detour Gold expects to produce between 475,000-525,000 ounces of gold at total cash costs of $780-$850 per ounce and all-in sustaining costs of $1,050-$1,150 per ounce. The company will focus on optimizing operations at its Detour Lake Mine in northern Ontario through initiatives like plant optimization and the development of the Block A zone. Detour Gold also plans to update its life of mine plan and continues exploring regional targets around its 630 square kilometer land package.