Kotlin Multiplatform & Compose Multiplatform - Starter kit for pragmatics

קבר הצדיק

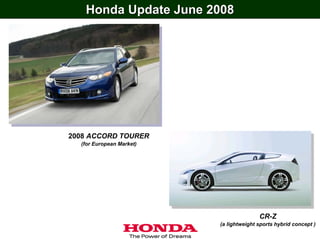

1. Honda Update June 2008

2008 ACCORD TOURER

(for European Market)

CR-Z

(a lightweight sports hybrid concept )

2. Outline

Highlights of Honda’s Business Growth Strategy

• US Operations (Automobile) P 2- 8

• Brazil Operations (Automobile & Motorcycle) P 9- 11

• Asia Operations (Automobile & Motorcycle) P 12- 18

• Europe Operations (Automobile) P 19- 20

• Production Capacity (Automobile) P 21

• Growth Potential of Motorcycle Business P 22

• Hybrid Vehicle Business Strategy P 23

Financial Highlights

• FY 08 Results

• Outline P 24- 25

• Segment Information P 26- 32

• Profit Analysis P 33- 36

• FY 09 Forecasts P 37- 40

• Dividend per Share P 41- 42

3. Honda’s Business Growth Strategy

Major Key Drivers

US Operations : Automobile

Brazil Operations : Automobile and Motorcycle

Asia Operations : Automobile and Motorcycle

Europe Operations : Automobile

Growth Potential of Motorcycle Business

Hybrid Vehicle Business Strategy

1

4. Operation in North America

Operating income in North America compressed

by higher yen and weak model mix

Yen

(billions)

150 12%

9.5% 10%

7.8%

7.7%

100 7.5% 8%

7.2% 7.3%

6.5% 6.7%

6.1%

5.8%

5.4% 6%

4.3%

50 4%

2%

72.7 68.5 106.7 105.8 114.4 95.7 118.2 128.4 97.0 116.0 156.3 63.1

0 0%

FY06 1Q 2Q 3Q 4Q FY07 1Q 2Q 3Q 4Q FY08 1Q 2Q 3Q 4Q

2

5. Update on Honda’s U.S. Automobile Business

Honda’s steady growth despite weak SAAR

Industry Demand Honda’s Retail Unit Sales

Unit

Unit (thousands)

(thousands) (aggregate numbers of Honda brand and Acura brand)

20,000 Passenger Cars Passenger Cars

Light Trucks Light Trucks 1,570

1,552

16,884 16,965 1,509

16,556 1,500 1,462

16,149

1,394

15,300

15,000

1,000

10,000

500

5,000

0 0

CY 04 '05 '06 '07 08(P)

CY 04 '05 '06 '07 08(E)

Source: Honda

3

6. U.S. Light Vehicle Retail Sales YoY Changes by manufacturers

January – April, 2008 vs 2007

Ho n da

Sm ar t USA

Mazda

Me r c e de s- Be n z

Vo lkswage n

Su zu ki

Kia

BMW

Nissan

Mit su bish i

Hyu n dai

T o yo t a

Fo r d

C h r ysle r

Ge n e r al M o t o r s

T OTAL

Unit

-250

(thousands) -200

-400 -150 -100 -50 0 50

4

7. U.S. Passenger Car Retail Sales YoY Changes by manufacturers

January – April, 2008 vs 2007

Honda

Nissan

Smart USA

Kia

Chrysler

Volkswagen

Hyundai

Mercedes-Benz

Mitsubishi

BMW

Mazda

Toyota

Suzuki

TOTAL

General Motors

Ford

Unit

-25

(thousands) -20 -15 -10 -5 0 5 10 15 20

5

8. U.S. Light Truck Retail Sales YoY Changes by manufacturers

January – April, 2008 vs 2007

Suzuki

Mazda

Mercedes-Benz

BMW

Volkswagen

Mitsubishi

Kia

Hyundai

Honda

Nissan

Toyota

Ford

General Motors

Chrysler

TOTAL

Unit

-200

(thousands) -150

-350 -100 -50 0 50

6

9. Update on Honda’s U.S. Automobile Business

Honda’s fuel efficient vehicles are well received in the U.S.

Unit demonstrates solid passenger car sales

(thousands)

Fit

1800

R dgeline

1600

Fit MDX

1400

Element

1200 CR-V CR-V

1000 Odyssey

800 Pilot

600

TSX

400

Civic RDX

TL

200

Accord Legend/RL

0

Civic

1999

2000

2001

2002

2003

2004

2005

2006

2007

CY 1998

2008(P)

Accord

7

10. Product pipeline and production flexibility in North America

Total Annual Production Capacity: 1,420,000 (current) ⇒ 1,620,000 (fall of 2008)

Passenger cars Light Trucks

Annual

location Capacity

Small Middle Luxury Crossover Pickup Van

Line 1

Line 1

Civic CSX

195

195

Canada

Canada Ontario

Ontario Alliston

Alliston

Line 2

Line 2

195

Civic MD-X Pilot Ridgeline Odyssey

195

Marysville

Marysville 440

440 Accord TL RDX

Ohio

Ohio

East

East

Liberty

Liberty

240

240 Civic CR-V Element

U.S.

U.S. Indiana

Indiana Greensburg

Greensburg 200

200 Civic

Line 1

Line 1

Ridgeline Odyssey

150

150

Alabama

Alabama Lincoln

Lincoln

Line 2

Line 2

150

Pilot Odyssey

150

Mexico

Mexico El Salto

El Salto 50

50 Accord CR-V

Import

Import New model in 2008

from Japan

from Japan

Accord CR-V

8

11. Operation in South America

Operating income in Other region

centered in Brazil to grow

Yen

(billions)

50

13%

11.7%

40

11.4%

11.3% 11.2%

10.9%

10.3% 10.4% 11%

30

9.6%

8.6% 9%

8.3% 8.4%

20

7.2%

7%

10

13.6 15.1 16.6 11.6 15.2 21.4 16.0 19.5 21.7 30.1 31.7 32.7

0 5%

FY06 1Q 2Q 3Q 4Q FY07 1Q 2Q 3Q 4Q FY08 1Q 2Q 3Q 4Q

9

12. Honda’s Automobile Business Growth in South America

Industry Demand Honda’s Unit Sales

(including commercial vehicles) Good sales of FFV models continue to

Unit Unit

(thousands) (thousands) contribute to growth in 2008.

5,000

160

Brazil Argentina Venezuela Chile

4,500 Flexible Fuel Vehicles (currently marketed in Brazil)

Colombia Ecuador Peru

140 Petrol Engine Vehicles

4,000

3,500 120

108

South America

3,000 100 Brazil only

84

2,500

80 86

68

2,000

60 57 67

1,500 57

50

40

1,000

500 20

0 0

CY 04 05 06 07 08(E) CY 04 05 06 07

Source: Global Insight Source: Honda

Honda’s Progress in South America Flexible Fuel Vehicles introduced in Brazil

1. Features of Honda FFV models in Brazil (Civic &Fit) Civic FFV Fit FFV

- Adapt to ethanol-to-gasoline ratios of between 20% and 100%

2. Further acceleration of production capacity in Brazil

100,000→ 120,000 within 2008

3. New plant in Argentina

Capacity:30,000 units, to start operation in 2009

Introduced in Nov. 2006 Introduced in Dec. 2006

10

13. Honda’s Motorcycle Business in Brazil

Solid operation as the market leader in the growing Brazil market

Industry: Other brands Further expansion of capacity is planned in 2009

Unit (thousands) (1,500 2,000 thousand units)

Honda

2,000

1,800

1,600

1,400

1,200

1,000

800

600

400 Expansion of production capacity Dec.2007

(1,350 → 1,500 thousand units per year)

200

0

CY 04 05 06 07 08(E)

Source:

Principal models Honda

CG 150 Titan CG 125 FAN Biz 125

11

14. Operation in Asia

Operating income in Asia exceed 100 billion in FY08

with higher auto and motorcycle growth

Yen

(billions)

50 14%

12%

40

9.4% 9.3% 10%

8.3% 8.0%

30

8%

6.8% 6.9% 6.8% 6.7%

5.8%

6%

20

5.2% 5.3%

4.5% 4%

10

2%

19.1 15.8 17.2 12.7 19.4 18.2 20.2 19.2 36.9 33.4 38.3 21.9

0 0%

1Q 2Q 3Q FY06 4Q 1Q 2Q 3Q FY07 4Q 1Q 2Q 3Q FY08 4Q

12

15. Update on Honda’s Automobile Business in India

Unit

Industry Demand Unit

Honda’s Unit Sales

(thousands) (excluding commercial vehicles, (thousands)

1,400 80

SUV and MUV)

Category

1,200

70

Premium

60

"A" 60 CR-V

1,000 55

800cc

50 Civic

800

40

40

35

600

30

400 City

20

200 10

Accord

0

0

CY 04 05 06 07 08(E) CY 04 05 06 07

Source: Global Insight Source: Honda

Honda model line up in India

Honda’s Progress in India

1. Enhancing dealer network

- Number of Dealer outlets: 34 (Mar. 2003) → 80 (Mar. 2008)

2. Further Accelerating production capacity expansion

Civic (July 2006-)

City (Oct 2003-)

Existing Plant Second Plant

50,000 →100,000 units 60,000 units

(2008 Jan. completed) (Operation starts toward

the end of 2009 to 2010)

CR-V (Nov 2006-) Accord (May 2008-) 13

16. Honda’s Motorcycle Business in India

Solid business foundation with 2 companies in rapidly growing market

Industry:

Unit (thousands) Expansion of annual production capacity

HHML 500 thou. Increase from April 2008

10,000 Other brands (India total 4,900 → 5,400 thousand units)

Hero Honda

Honda Motorcycle & Scooter India

8,000

6,000

4,000

2,000

0

Source :

CY 04 05 06 07 08(E) Honda

Principal models of

Principal models of Hero Honda Motors Limited Honda Motorcycle & Scooter India

Splendor+ CD Deluxe Passion+ Activa Shine

14

17. Growth of HMSI in India

Steady Growth of Honda Motorcycle & Scooter India, subsidiary of Honda

Industry: Expansion of production capacity by the end of 2010

Unit (thousands)

1,000 (1,000 → 1,200 thousand units per year)

800

600

400

200

0

Source :

CY 04 05 06 07 Honda

Principal models of Honda Motorcycle & Scooter India HMSI Dealer

Activa Shine Unicorn (Sep 2004-) Aviator (Mar 2008-)

15

18. Honda’s Motorcycle Business in Vietnam

Honda to enhance product pipeline for growing market,

Further expansion of production capacity

Industry: Expansion of production capacity in Aug 2008

Unit (thousands) Other brands

(1,000 → 1,500 thousand units per year)

Honda

3,000

2,500

2,000

1,500

1,000

500

0

CY 04 05 06 07 08(E)

Source:

Principal models Honda

Wave S Future Neo FI Click* (Oct 2006-) Air Blade* (Apr 2007-)

(May 2007-) (Apr 2007-) * AT model: Motorcycles equipped with automatic transmission

16

19. Honda’s Motorcycle Business in Indonesia

Honda to enhance product pipeline to go with the momentum of the market

Industry: Other brands

Unit (thousands)

Honda

6,000

5,000

4,000

3,000

2,000

1,000 Added annual production capacity in Sep. 2005

(2,000 → 3,000 thousand units)

0

CY 04 05 06 07 08(E) Source:

Honda

Principal models Coming in 2008

Revo Vario* Supra X 125

* AT model: Motorcycles equipped with automatic transmission 17

20. Update on Honda’s Automobile Business in China

Industry Demand Honda’s Unit Sales

Unit

(thousands)

(excluding commercial vehicles) Unit

(thousands)

7,000 500 Over 490

450

6,000 424

WDHAC models

400

Civic

5,000

350

323

CR-V

4,000

300

257 Fit

250

3,000 214

200 City GHAC models

2,000 150

Odyssey

100

1,000

50 Accord

0 0

CY 04 05 06 07 CY 04 05 06 07 08(P)

Source: CAAM Source: Honda

Honda’s Progress in China GHAC model line up

1 Enhancing model lineup and dealer network

- New Accord introduced in Jan. 2008, New Fit to be introduced within 2008

- Number of Dealer outlets: GHAC 361, WDHAC 189, Acura 8(Mar.2008)

Total 700 outlets within a year Fit City Accord Odyssey

- Introduction of Acura (RL/TL/MDX) WDHAC model line up

2 Progress in Manufacturing Operation

GHAC*1 : Capacity 360 thou. units *1 GHAC: Guangzhou Honda Automobile Co., Ltd.

WDHAC*2 : Capacity 120 thou. units--> 240 thou. units within 2yrs *2 WDHAC: Dongfeng Honda Automobile Co., Ltd.

CHAC*3 : Added 2nd shift from Apr. 2007, capacity 50 thou. units *3 CHAC: Honda Automobile (China) Co., Ltd.

3 GHAC begin selling products under its own brand in 2010 Civic CR-V

18

21. Operation in Europe

Operating income in Europe (including Russia) to grow,

expecting higher sales in Russia

Yen

(billions)

30 5%

4.3% 4.3%

4.2%

4%

20

2.9% 2.9%

2.8% 2.6% 3%

2%

2.0%

10

1.6%

1.4%

1%

1.1%

12.7 0.3%

0.8 2.8 9.8 6.4 9.0 3.7 12.6 10.3 16.7 5.8 18.6

0 0%

FY06 1Q 2Q 3Q 4Q FY07 1Q 2Q 3Q 4Q FY08 1Q 2Q 3Q 4Q

19

22. Update on Honda’s Automobile Business in Russia

Unit Industry Demand Unit

(thousands)

Honda’s Unit Sales

(thousands) (excluding commercial vehicles) 60

3,000

Foreign brands

Domestic brands

2,500

2,000

40 38.6

Jazz

CR-V

1,500

1,000 20

Civic

15.7

500 8.9

6.0 Accord

0 0

CY 04 05 06 07 CY 04 05 06 07

Source: AEB (The Association of European Businesses) Source: Honda

Honda model line up in Russia

Honda’s Progress in Russia

1 Starting business

- Established subsidiary company (HMR) in Feb. 2004

Jazz Civic 5D Civic 4D

2 Enhancing dealer network

- Number of Dealer outlets:

15 (2004 end) → 43 (Mar. 2008)

expand mainly in large cities,

total 70 outlets in a few years

CR-V Accord Pilot (coming in 2008)

20

23. Expansion of Production Capacity (Automobiles)

High value added model at Yorii Auto Plant

Next generation high efficiency engine at Ogawa Engine Plant

Unit

(thousands)

Yorii

India

Japan

Argentina +60

Indiana +200

+30

+200

Thailand

+120

Brazil

+20

4,055 WDHAC

China

+120 within 2yrs

Current 2008 2009 2010

21

24. Growth Potential of Motorcycle Business in Emerging Markets

GDP per capita Penetration Rate (% of population) of Motorcycles

(U.S.$)

(JETRO 2006) 10% 20% 30% 40% 50% 60%

$15,482 Taiwan 59.5%

Population (millions)

$5,718 Malaysia 28.3% Units in operation (millions)

*Indonesia data as of 2004

$3,136 Thailand 23.8% *India data as 2004 provisional

$723 Vietnam 20.5%

$1,640 Indonesia* 10.8%

$5,714 Brazil 5.1%

$796 India*

4.6%

100 mil 200 mil 1,100 mil

Motorcycle penetration is still low in Honda’s principal markets

Industry: Vietnam

● Honda wholesales unit (thousands) 12,000 Honda wholesales:

( thousands ) Thailand ( thousands )

20,000 Brazil

Indonesia 10,000

India

8,000

6,000

10,000

4,000

2,000

Source: Honda

0 0

CY 04 05 06 07 08(E)

Honda has strong position in such markets 22

25. Hybrid Vehicle Business Strategy

Hybrid Car in the U.S. market

Unit

(thousands)

Hybrid technology is about to hit the “growth” stage,

350 Honda aims wider market penetration with

Other Brand

300

Honda

new dedicated hybrid model

250

200

150

Introduction of Honda Insight

100

50

Insight, 2006 Civic Hybrid,

0 first hybrid vehicle in the U.S. won the “World Car of the Year Award”

for Greenest Car

CY99 00 01 02 03 04 05 06 07

-Compact Control Unit / Battery

Cost down on Next Hybrid System -Thin Hybrid Motor

-Efficient manufacturing processes

Hybrid models with affordable price: 500,000 annual global sales beyond 2010

New Hybrid Model Compact, 5 door/5 passenger, to be marketed in early 2009

Hybrid Sports

CR-Z, Concept model

Honda annual

global sales New Civic Hybrid

beyond 2010

Fit Hybrid

23

26. Financial Highlights

•FY 08 Results

•Outline

•Segment Information

•Profit Analysis

•FY 09 Forecasts

•Dividend per Share

27. Outline of 4th Quarter Financial Results (Consolidated)

4Q Results Business environment

Unit Sales US economy slow down, ongoing subprime loan impact

FY07 FY08 Change Declining personal consumption in European economy

Unit (thousands)

Continued growth of Asian economy

Motorcycles 2,408 2,368 - 1.7% Signs of weakness in Japan economy

Continued high prices for crude oil and raw materials

Automobiles 957 1,051 + 9.8% Yen appreciation against U.S. dollar, depreciation against

other currencies

Power Products 2,128 2,092 -1.7% Motorcycle Market

Growth in Vietnam and Brazil continued

Declining market in North America

4Q Results Automobile Market

Growth of emerging markets such as BRICs

Financial results Strong demand for fuel-efficient cars in the U.S.

Yen (billions) FY07 FY08 Change

Japan automobile market remain stagnant

Net sales & other

3,087.8 3,055.5 - 1.0% Review of financial results

operating revenue

Operating margin decreased due to factors including

Operating income 250.2 168.8 - 32.5% significant yen appreciation against U.S. dollar despite the

increased automobile unit sales achieved in the toughening

Income before business environment such as in the U.S.

239.0 146.8 - 38.6%

income taxes Unit Sales

Equity in income Motorcycles: Strong sales in South America, etc.

19.9 24.3 * + 22.1% Decreased unit sales of component parts for Asia

of affiliates

Automobiles: Unit sales increased in all regions

Net income 176.1 25.4 - 85.6% Power Products:Increased unit sales in Europe, Asia, Other Regions

Decreased unit sales in North America

EPS (Yen) 96.70 14.01 - 82.69 Net sales & other operating revenue

Increased unit sales in automobile segments

Note : Shares which are based approx. approx.

* Record high Net sales decreased due to currency translation effects

on calculation of EPS 1,821,994,000 shares 1,814,587,000 shares for 4Q

(weighted average number of shares outstanding ) Operating income

<Increase Factors>

Continuing cost reduction effects

Average Rates (Yen) Increased profit from increased automobile unit sales

stronger by <Decrease Factors>

U.S. Dollar 120 106 14 yen Currency effect of yen appreciation against U.S. dollar

weaker by Increase in sales incentives in North America

Euro 157 158 Increased raw material costs

1 yen 24

28. Outline of 4th Quarter & Twelve Months Financial Results (Consolidated)

4Q Results Twelve Months Results

Unit Sales

FY07 FY08 Change FY07 FY08 Change

Unit (thousands)

Motorcycles 2,408 2,368 - 1.7% 10,369 9,320 - 10.1%

Automobiles 957 1,051 + 9.8% 3,652 3,925 + 7.5%

Power Products 2,128 2,092 -1.7% 6,421 6,057 - 5.7%

4Q Results Twelve Months Results

Financial results

Yen (billions) FY07 FY08 Change FY07 FY08 Change

Net sales & other

operating revenue

3,087.8 3,055.5 - 1.0% 11,087.1 12,002.8 * + 8.3%

Operating income 250.2 168.8 - 32.5% 851.8 953.1 * + 11.9%

Income before

income taxes

239.0 146.8 - 38.6% 792.8 895.8 * + 13.0%

Equity in income

19.9 24.3* + 22.1% 103.4 118.9* + 15.0%

of affiliates

Net income 176.1 25.4 - 85.6% 592.3 600.0 * + 1.3%

EPS (Yen) 96.70 14.01 - 82.69 324.62 330.54* + 5.92

Note : Shares which are based approx. approx. * Record high approx. approx.

* Record high for

on calculation of EPS 1,821,994,000 shares 1,814,587,000 shares for 4Q 1,824,675,000 shares 1,815,356,000 shares twelve months

(weighted average number of shares outstanding ) (weighted average number of shares outstanding )

Average Rates (Yen)

stronger by stronger by

U.S. Dollar 120 106 14 yen 117 114 3 yen

weaker by weaker by

Euro 157 158 1 yen 151 162 11 yen

25

29. Motorcycle Unit Sales (Motorcycles + All-Terrain Vehicles, etc.)

Change - 1,049

Unit FY08 4Q from FY 07 4Q

Major increase / decrease factors ( - 10.1% ) Approx.4,580

(thousands)

Approx.2,860

13,000

13,000 Japan 66 - 13 ・Decrease of Dio etc.

North ・Decrease of CBR600RR, VT750

150 -14 Wave S (Vietnam)

12,000

12,000 America ・ Decrease of ATV such as Four Trax Foreman

11,000

Europe 89 -8 ・Decrease of CBR600RR in Italy

11,000

・Decrease of component parts for Indonesia 10,369

Asia 1,617 - 89 ・Increase of Wave S and AT models such as Air Blade in

10,000

10,000 Vietnam

1,305

Other ・Introduction of POP100 in Brazil CG125 FAN (Brazil) 9,320

Regions

446 + 84 ・Increase of CG125, NXR150 in Brazil

9,000

9,000

Unit sales of Honda-brand

Other

Total 2,368 - 40 motorcycle products that 1,610 Regions

8,000

8,000 are manufactured and sold

by overseas affiliates

accounted for under the

7,000

7,000 equity method, but do not

use any parts supplied by

Honda and its subsidiaries

6,000 - 40

6,000

( - 1.7% )

7,895 6,633 Asia

5,000

5,000

4,000

4,000

Approx.560 Approx.640 Approx.1,150 Approx.1,100 Approx.1,160 Approx.1,280

Approx.1,020

3,000

3,000 Approx.500 2,816 2,765

2,380 341 314 2,408 2,253 2,333 2,366 2,368

288 362 392 401

2,000

2,000 371 446

2,163 2,217

1,809 1,706

1,000

1,000 1,623 1,645 1,748 1,617 329 Europe

313

105 71 56 97 95 68 61 89 North

143 107 164 121 102 150 503 453 America

89 80

89 98 71 79 84 107 54 66 337 311 Japan

00

1Q

第1四半期 2Q 3Q

第2四半期 第3四半期

第3四半期 4Q

第4四半期 1Q

第1四半期 2Q 3Q

第2四半期 第3四半期 4Q

第3四半期 第4四半期

第4四半期 12ヶ月間通算 12ヶ月間通算

第1四半期 第2四半期 第4四半期 第1四半期 第2四半期 12ヶ月間通算 12ヶ月間通算

Twelve Months Twelve Months

FY07 FY08 FY07 FY08

Unit sales is the total of sales of completed products of Honda and its consolidated subsidiaries and sales of parts for Honda’s affiliates accounted for under the equity method. 26

31. Automobile Unit Sales

Unit Change

FY08 4Q from FY 07 4Q

Major increase / decrease factors

(thousands) + 273

・Increase of FIT and Inspire ( + 7.5% )

Japan 191 +2 ・Decrease of That’s FIT (Japan)

4,000 North ・Increase of Accord and CR-V

3,925

America

459 +9 ・ Decrease of Pilot

3,652 314 Other

Regions

Europe 109 +7 ・Increase of Civic and CR-V in Russia, Ukraine

3,500 248

・Increase of component parts for China (CR-V and Fit etc ) Civic (Russia)

Asia 203 + 54 ・Increase of CR-V in ASEAN countries such as Indonesia 755 Asia

620

Other ・Increase of Civic FFV in Brazil

3,000 89 + 22 ・Increase of Accord in Middle East countries such as

Regions Saudi Arabia and UAE

Total 1,051 + 94 324 391 Europe

2,500 CR-V (Indonesia)

2,000

+ 94

1,850 North

( + 9.8% ) 1,788 America

1,500

991 1,051

1,000 896 884 915 957 946 937 89

67 72 87

61 66

60 60 188 203

155 149 187 177

153 163

102 109

71 79 72 92 100 90

500

456 411 471 450 465 445 481 459 672 615 Japan

156 171 156 189 136 143 145 191

0

1Q

第1四半期 2Q

第2四半期 3Q

第3四半期 4Q

第4四半期 1Q

第1四半期 2Q

第2四半期 3Q

第3四半期 4Q

第4四半期 累計 累計

Twelve Months Twelve Months

FY07 FY08 FY07 FY08

Unit sales is the total of sales of completed products of Honda and its consolidated subsidiaries and sales of parts for Honda’s affiliates accounted for under the equity method. 28

33. Power Products Unit Sales

Change

Unit FY08 4Q Major increase / decrease factors

(thousands)

from FY 07 4Q - 364

(- 5.7%)

Japan 151 + 12 ・Increase of general purpose engines for OEM GX35T

(general purpose engine)

6,421

6,500 North ・Decrease of general purpose engines for OEM, generators in

America

888 -135 the U.S.

406 6,057

6,000 Europe 671 + 47 ・Increase of general purpose engines for OEM Other

484 Regions

・Increase of general purpose engines for OEM, water pumps in GCV160 760

5,500 Asia 251 + 21 Thailand, Indonesia (general purpose engine)

・Decrease of general purpose engines

・Increase of lawn mowers in Australia

915 Asia

5,000 Other

Regions

131 + 19 ・Increase of generators in South Africa

4,500 1,625

Total 2,092 - 36

4,000 HRU19D1 Buffalo Buck 1,693 Europe

(lawn mower)

3,500

- 36

(- 1.7%)

3,000

2,500

2,128 2,092

112 3,103

2,000 131

1,724 230 251 2,415 North

72 1,529 America

1,500 162 1,382 624 97

1,187 117 220

1,258 1,178 671

382

105 161 116

140

1,000 207 365

390 242

202

254 1,023 280

971 352 888

500 494 615 687

479 361 527 550 Japan

137 127 124 139 135 141 123 151

0

1Q

第1四半期 2Q

第2四半期 3Q

第3四半期 4Q

第4四半期 1Q

第1四半期 2Q

第2四半期 3Q

第3四半期 4Q

第4四半期 Twelve累計 累計

Months Twelve Months

FY07 FY08 FY07 FY08

Unit sales is the total of sales of completed products of Honda and its consolidated subsidiaries and sales of parts for Honda’s affiliates accounted for under the equity method. 30

36. Change in Income Before Income Taxes < FY08 4th Quarter >

Income before Income taxes Yen (billions)

- 92.2 bn. yen ( - 38.6 % )

Other Income

Operating Income - 81.3 bn. yen ( - 32.5 %) & Expenses

- 10.8 bn. yen

<Increase Factors> <Decrease Factors>

- Continuing cost reduction effects, etc. - Increase in provision for the allowance for

<Decrease Factors> credit losses

- Increased raw material costs - Increase in quality related expenses

- Increase in depreciation expenses, etc. - Increased logistics expenses due to the

increase in unit sales, etc.

- 28.3 + 31.6 - 46.2

Revenue,

+ 4.4

Cost Reduction,

model mix, the effect of raw

Increase Decrease

etc. material cost

in SG&A - 42.8

fluctuations, etc. in R&D

Currency - 27.0 + 16.1

Effect

<Decrease Factors> Fair value of Others

derivative

- Increase in sales incentives in North America instruments

- Change in model mix, etc. ( Exhibit 2)

<Increase Factors>

- Increased profit from increased automobile unit sales - Currency effect due to difference between average

rates and transaction rates: + 28.1 bn. yen

- Change in sales prices, etc.

- Gain and loss from valuation of the balance of

receivable and debt: - 12.0 bn. yen

239.0 146.8

FY07 4Q FY08 4Q

【Currency Effect 】

<Impact on Operating income> - 42.8 bn. yen (due to difference of average rates & translation effects)

<Impact on Other income & expenses> + 28.1 bn. yen (due to difference between average rates and transaction rates)

<Impact on Income before income taxes> - 14.6 bn. yen (see also Exhibit 1) 33

37. FY08 4th Quarter & Twelve Months Change in Income Before Income Taxes

- Currency effects (effects associated with sales transactions and translation effects) - (Exhibit 1)

Yen (billions)

FY08 4Q Average Rates (Yen)

FY08

Twelve months

Effects in Yen Effects in Yen

(billions) FY07 4Q FY08 4Q Change (billions)

stronger

JPY / USD - 44.5 120 106

by 14 yen

- 34.5

weaker

JPY / Euro + 0.5 157 158

by 1 yen

+ 15.2

JPY / Others - 0.2 ― ― ― + 23.6

between other currencies + 11.8 ― ― ― + 8.6

Due to difference of average rates *1: Impact of YOY difference of FOREX to be used for

(Impact on Operating income)

*1 - 32.3 booking revenue of foreign currency transactions + 13.0

Due to difference between average *2: Impact of YOY difference between average FOREX and

*2

rates and transaction rates + 28.1 hedge rates during the period

+ 53.6

(Impact on Other income & expenses)

Currency effect associated with

sales transactions - 4.1 + 66.7

*3: Effect due to the difference of the rate used for

Currency effect from translation translating Honda’s overseas subsidiaries’ financial

of foreign financial statements

*3 - 10.4 statements denominated in foreign currencies into + 24.6

Japanese yen with the corresponding period of the

(Impact on Operating income) fiscal year

Total - 14.6 + 91.3

34

38. FY08 4th Quarter & Twelve Months Change in Income Before Income Taxes

- Gain and loss on derivative instruments - (Exhibit 2)

Yen (billions)

4Q Twelve Months

FY07 FY08 Change FY07 FY08 Change

Gain and loss on fair value

adjustments for foreign

currency exchange contracts

+ 14.2 + 21.8 + 7.6 - 0.8 + 14.5 + 15.4

Interest rate swap - 6.6 - 41.0 - 34.3 - 28.7 - 84.2 - 55.5

Others - 0.7 - 1.0 - 0.3 - 27.2 - 0.5 + 26.6

Total + 6.7 - 20.2 - 27.0 - 56.8 - 70.2 - 13.4

Reference: (4Q) (Twelve Months)

<Swap interest rate> <Swap interest rate>

At the end of Dec, 2006 5.16% At the end of Dec, 2007 3.92% At the end of Mar, 2006 5.23% At the end of Mar, 2007 5.04%

At the end of Mar, 2007 5.04% At the end of Mar, 2008 2.53% At the end of Mar, 2007 5.04% At the end of Mar, 2008 2.53%

Difference (-0.12%) Difference (-1.39%) Difference (-0.19%) Difference (-2.51%)

35

39. Asia Equity in income of affiliates

Yen + 7.6 + 13.4

(billions)

( + 114.3% ) ( + 18.5% )

86.1

80

72.6

70

60

50

40

30 26.8

22.6 23.2 22.2 22.6

20.1

20 14.3

10 6.6

0

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q Twelve Months Twelve Months

FY07 FY08 FY07 FY08

Reference:

Operating income & Net income of affiliates accounted for under the equity method in Asia

Operating

income 58.0 55.7 49.9 30.1 61.2 56.3 55.7 38.0 193.8 211.4

Net income 51.8 50.2 44.2 27.6 57.2 50.0 49.7 31.0 174.0 188.0

Affiliates accounted for under the equity method

Motorcycle Business Automobile Business:

China Sundiro Honda Motorcycle Co., Ltd.* China Guangzhou Honda Automobile Co., Ltd.*

Wuyang-Honda Motors (Guangzhou) Co., Ltd.* Dongfeng Honda Engine Co., Ltd.*

India Hero Honda Motors Ltd. Dongfeng Honda Automobile Co., Ltd.*

Indonesia P.T. Astra Honda Motor*

Malaysia Hicom-Honda MFG. Malaysia SDN. BHD.

Pakistan Atlas Honda Limited* Others 37, Total 47 companies

Thailand A.P. Honda Co., Ltd.

As of the end of March, 2008

* Indicates fiscal term of companies differs from that of Honda Motor Co., Ltd. 36