Downloaded 10 times

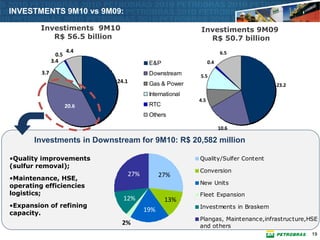

Petrobras reported financial results for the third quarter of 2010. Net income increased 10% compared to the same period last year to R$8.566 billion. Domestic oil and gas production grew 2% while refinery output increased due to a plant restart. Investments totaled R$56.5 billion year-to-date, 11% higher than the first nine months of 2009. Average oil prices remained stable in Brazil despite declines in international markets.