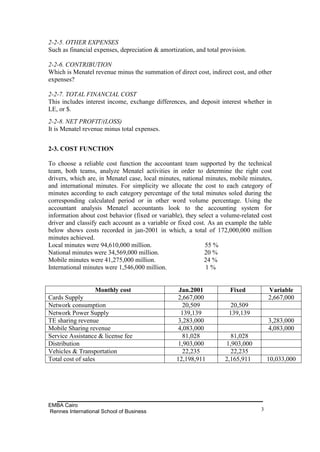

This cost function will help Menatel to predict the total cost for any level of activity and to make better decisions. 2-4. COST CONTROL To control costs Menatel apply the following: - Rational consumption policy for all expenses. - Review all contracts with suppliers to reduce discounts and get best prices. - Freeze investments in new fixed assets and optimize use of current assets. - Review all resources to achieve optimum productivity. - Standard costing system to set standards and monitor variances from standards. - Budgeting to set targets and monitor performance against budget. - Variance analysis to identify reasons for variances and take corrective actions.