Tutorial 3 question

•Download as DOCX, PDF•

0 likes•467 views

This document contains 3 questions regarding accounting for financial instruments. Question 1 asks about foreign exchange gains and losses from an unhedged transaction and reporting a forward contract. Question 2 asks about journal entries for cash flow and fair value hedges of a foreign currency receivable. Question 3 asks for journal entries applying cash flow hedge accounting to a forward contract hedging a foreign currency payable and discusses fair value hedge accounting.

Recommended

More Related Content

Similar to Tutorial 3 question

Similar to Tutorial 3 question (9)

More from kim rae KI

Recently uploaded

Recently uploaded (20)

Tutorial 3 question

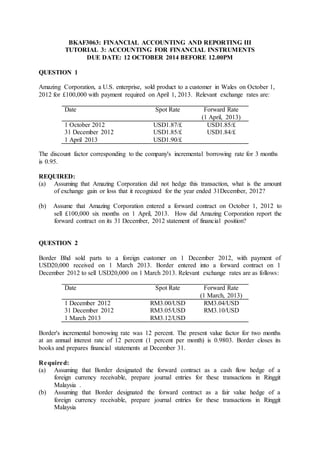

- 1. BKAF3063: FINANCIAL ACCOUNTING AND REPORTING III TUTORIAL 3: ACCOUNTING FOR FINANCIAL INSTRUMENTS DUE DATE: 12 OCTOBER 2014 BEFORE 12.00PM QUESTION 1 Amazing Corporation, a U.S. enterprise, sold product to a customer in Wales on October 1, 2012 for £100,000 with payment required on April 1, 2013. Relevant exchange rates are: Date Spot Rate Forward Rate (1 April, 2013) 1 October 2012 USD1.87/£ USD1.85/£ 31 December 2012 USD1.85/£ USD1.84/£ 1 April 2013 USD1.90/£ The discount factor corresponding to the company's incremental borrowing rate for 3 months is 0.95. REQUIRED: (a) Assuming that Amazing Corporation did not hedge this transaction, what is the amount of exchange gain or loss that it recognized for the year ended 31December, 2012? (b) Assume that Amazing Corporation entered a forward contract on October 1, 2012 to sell £100,000 six months on 1 April, 2013. How did Amazing Corporation report the forward contract on its 31 December, 2012 statement of financial position? QUESTION 2 Border Bhd sold parts to a foreign customer on 1 December 2012, with payment of USD20,000 received on 1 March 2013. Border entered into a forward contract on 1 December 2012 to sell USD20,000 on 1 March 2013. Relevant exchange rates are as follows: Date Spot Rate Forward Rate (1 March, 2013) 1 December 2012 RM3.00/USD RM3.04/USD 31 December 2012 RM3.05/USD RM3.10/USD 1 March 2013 RM3.12/USD Border's incremental borrowing rate was 12 percent. The present value factor for two months at an annual interest rate of 12 percent (1 percent per month) is 0.9803. Border closes its books and prepares financial statements at December 31. Required: (a) Assuming that Border designated the forward contract as a cash flow hedge of a foreign currency receivable, prepare journal entries for these transactions in Ringgit Malaysia . (b) Assuming that Border designated the forward contract as a fair value hedge of a foreign currency receivable, prepare journal entries for these transactions in Ringgit Malaysia

- 2. QUESTION 3 Emas Bhd is a manufacturer of hi-tech equipments used in telecommunication industry. On 1 November 2013, it purchased parts from its supplier in the USA for USD100,000. Payment was to be made in USA dollar on 31 January 2014. To hedge risk exposure to changes in foreign exchange rate, Emas Bhd entered into a forward contract on 1 November 2013 to purchase USD100,000 on 31 January 2014 in exchange for RM298,500. The relevant exchange rates for the USA dollar are as follows: Date Spot Rate (RM/USD) Forward Rate (RM/USD) (31 January 2014) 1 November 2013 RM3.000/USD RM2.985/USD 31 December 2013 RM3.009/USD RM2.995/USD 31 January 2014 RM2.980/USD The present value factor for one month at an annual interest rate of 12 percent is 0.990. Emas Bhd prepared financial statements at 31 December. REQUIRED: (a) Prepare the journal entries for the above transactions. Emas Bhd applied a cash flow hedge accounting. (b) Discuss the accounting treatment for a forward contract used as a fair value hedge of a foreign-currency-denominated asset or liability.