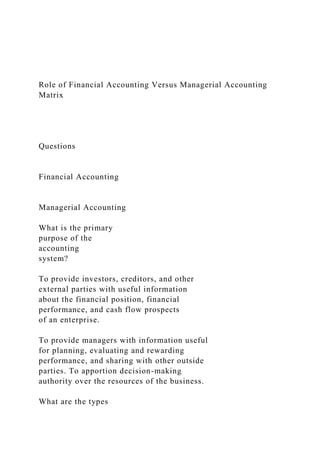

Role of Financial Accounting Versus Managerial Accounting Matrix

Questions

Financial Accounting

Managerial Accounting

What is the primary

purpose of the

accounting

system?

To provide investors, creditors, and other

external parties with useful information

about the financial position, financial

performance, and cash flow prospects

of an enterprise.

To provide managers with information useful

for planning, evaluating and rewarding

performance, and sharing with other outside

parties. To apportion decision-making

authority over the resources of the business.

What are the types

of reports

produced?

Primarily financial statements (statement

of financial position or balance sheet,

incomestatement, statement of cash

flows) and related notes and supplemental

disclosuresthat provide investors,

creditors, and otherusers information to

support externaldecision-making

processes.

Many different types of reports, depending

on the nature of the business and the

specific information needs of management.

Examples include budgets, financial

projections, benchmark studies, activitybased

cost reports, and cost-of-quality

assessment.

Who are the

primary users?

Outsiders as well as managers.

For financial statements, these

outsiders include stockholders,

creditors, prospective investors,

regulatory authorities, and the

general public

Management (different

reports to different

managers), customers,

auditors, suppliers, and

others involved in an

organization’s value chain.

What portion of the

company is the

primary focus?

Usually the company viewed as a whole.

A component of the company’s value

chain, such as a business segment, supplier,

customer, product line, department, or

product.

What time periods

are included?

Usually a year, quarter, or month. Most

reports focus on completed periods.

Emphasis is placed on the current (latest)

period, with prior periods often shown for

comparison.

Any period–year, quarter, month, week,

day, even a work shift. Some reports

are historical in nature; others focus on

estimates of results expected in future

periods.

Are there any

requirements for

the standards of

report

presentation?

Generally accepted accounting principles,

including those formally established in the

authoritative accounting literature and

standard industry practice.

Rules are set within each organization

to produce information most relevant to

the needs of management. Management

needs include reporting to both external

constituents and internal users.

Source: Weygandt, J.J., Kieso, D.E. y Kimmel, P.D. (2015). Accounting principles. (12th Ed.). John Wiley & Sons. New York.

...

Incoming and Outgoing Shipments in 1 STEP Using Odoo 17

Role of Financial Accounting Versus Managerial Accounting Matr.docx

1. Role of Financial Accounting Versus Managerial Accounting

Matrix

Questions

Financial Accounting

Managerial Accounting

What is the primary

purpose of the

accounting

system?

To provide investors, creditors, and other

external parties with useful information

about the financial position, financial

performance, and cash flow prospects

of an enterprise.

To provide managers with information useful

for planning, evaluating and rewarding

performance, and sharing with other outside

parties. To apportion decision-making

authority over the resources of the business.

What are the types

2. of reports

produced?

Primarily financial statements (statement

of financial position or balance sheet,

incomestatement, statement of cash

flows) and related notes and supplemental

disclosuresthat provide investors,

creditors, and otherusers information to

support externaldecision-making

processes.

Many different types of reports, depending

on the nature of the business and the

specific information needs of management.

Examples include budgets, financial

projections, benchmark studies, activitybased

cost reports, and cost-of-quality

assessment.

Who are the

primary users?

Outsiders as well as managers.

For financial statements, these

outsiders include stockholders,

creditors, prospective investors,

regulatory authorities, and the

general public

Management (different

reports to different

managers), customers,

auditors, suppliers, and

others involved in an

organization’s value chain.

3. What portion of the

company is the

primary focus?

Usually the company viewed as a whole.

A component of the company’s value

chain, such as a business segment, supplier,

customer, product line, department, or

product.

What time periods

are included?

Usually a year, quarter, or month. Most

reports focus on completed periods.

Emphasis is placed on the current (latest)

period, with prior periods often shown for

comparison.

Any period–year, quarter, month, week,

day, even a work shift. Some reports

are historical in nature; others focus on

estimates of results expected in future

periods.

Are there any

requirements for

the standards of

report

presentation?

Generally accepted accounting principles,

including those formally established in the

4. authoritative accounting literature and

standard industry practice.

Rules are set within each organization

to produce information most relevant to

the needs of management. Management

needs include reporting to both external

constituents and internal users.

Source: Weygandt, J.J., Kieso, D.E. y Kimmel, P.D. (2015).

Accounting principles. (12th Ed.). John Wiley & Sons. New

York.