This document outlines the agenda for a two-day workshop on market policy and value chain analysis in Ethiopia. Day 1 will focus on agricultural and livestock markets, including discussions of theory of market policies, cereal markets, and livestock markets. Day 2 will cover food system transformation concepts and the case of Ethiopia. The final theme will be on value chain analysis, exploring the teff and dairy value chains in Ethiopia through case studies and readings. The workshop aims to provide participants with knowledge on market policies and tools for value chain analysis to inform agricultural development in Ethiopia.

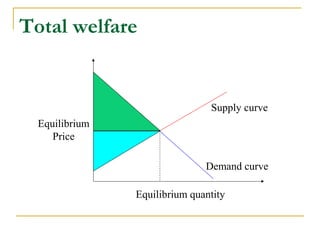

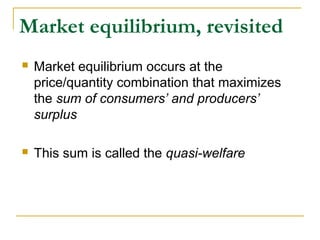

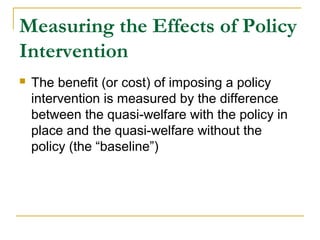

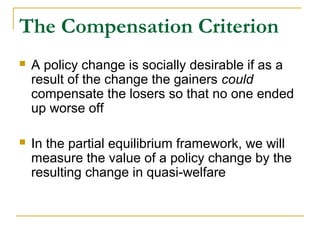

![Lesson 8--equilibrium[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lesson-8-equilibrium1-130409201835-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)