Applied Math 40S Slides May 11, 2007

•

0 likes•343 views

A conclusion of the case study on buying versus renting a home.

Recommended

More Related Content

What's hot

What's hot (18)

Viewers also liked

Viewers also liked (12)

Similar to Applied Math 40S Slides May 11, 2007

Similar to Applied Math 40S Slides May 11, 2007 (20)

More from Darren Kuropatwa

More from Darren Kuropatwa (20)

Recently uploaded

Recently uploaded (20)

Applied Math 40S Slides May 11, 2007

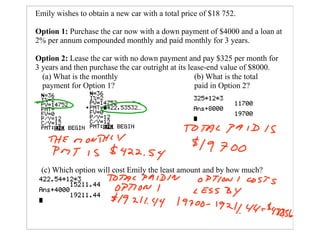

- 1. Emily wishes to obtain a new car with a total price of $18 752. Option 1: Purchase the car now with a down payment of $4000 and a loan at 2% per annum compounded monthly and paid monthly for 3 years. Option 2: Lease the car with no down payment and pay $325 per month for 3 years and then purchase the car outright at its lease-end value of $8000. (a) What is the monthly (b) What is the total payment for Option 1? paid in Option 2? (c) Which option will cost Emily the least amount and by how much?

- 2. A farmer buys a tractor for $60 000. If this tractor depreciates at a rate of 8% per year, how much will it be worth after 6 years? Answer to the nearest $100.

- 3. Bill puts $500 into an account at the beginning of every three months. If the account earns 4% per annum, compounded monthly, how much will he have after 8 years?

- 4. Rent or Buy? A Case Study ... The Browns have an opportunity to buy a home valued at $50 000 with a down payment of $5000 and a mortgage of $45 000, or rent the home for $525 per month. If they buy, they will get a 15-year mortgage at 7.5%. Annual property taxes are approximately 1.5% of the market value (i.e. the sale price) of the home. They expect their home to appreciate in value by about 2% per year. (That is, it will become 2% MORE VALUABLE each year. If it is worth $100 this year, next year it will be worth $102 and the year after that it would be worth $104.04.) If they rent, their rental payments will increase by 3% each year, and they expect to get a 7% annual return on their investment of the $5000 they did not use as a down payment.

- 6. (a) What is the size of the monthly mortgage payment? (b) What will their equity be in the home after two years of ownership? (c) After one year, how does the cost of payments plus property taxes compare with the cost of rental payments? (d) After 10 years, how does the annual cost of payments plus property taxes compare with the annual cost of rental payments?

- 7. (d) After 10 years, how does the annual cost of payments plus property taxes compare with the annual cost of rental payments?

- 8. (e) What might be some reasons for the Brown family to rent instead of buy - even though renting seems to be more expensive in the long run?

- 9. Mr. T’s family has decided to buy a larger home, and the date of possession is April 1. The following expenses are related to the purchase of the home: The price of the home is $135 000, and he has $45 000 as a down payment. He will buy homeowners insurance on the new home for $425, but will receive a refund of $300 from his previous home insurance policy. He has the new home appraised by a real estate agent, and the fee is $250. The bank requires a land survey which costs $550. His legal fees, including land transfer taxes and disbursements, are $875.The movers charged $1200 for moving his furniture and other belongings, and the company he works for paid half of this. The family decided to install new carpets into part of the house at a cost of $2400 plus PST and GST (7% each). He did the installation himself, and so there were no installation charges. They also bought a new fridge for $940 plus PST and GST (7% each) to replace the old one that did not fit into the new kitchen. The previous owner had paid the property taxes of $2350 for the period January 1 to December 31, and he had to pay for his share of the taxes. The cost of hooking up telephone and TV are $45. Determine the additional costs of moving for Mr. T and his family.