Unveiling Falcon Invoice Discounting: Leading the Way as India's Premier Bill...

6. irmd (24 july 2019)

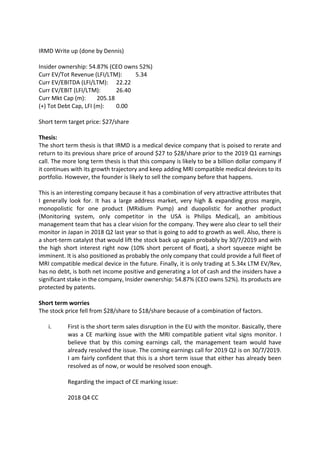

1. IRMD Write up (done by Dennis)

Insider ownership: 54.87% (CEO owns 52%)

Curr EV/Tot Revenue (LFI/LTM): 5.34

Curr EV/EBITDA (LFI/LTM): 22.22

Curr EV/EBIT (LFI/LTM): 26.40

Curr Mkt Cap (m): 205.18

(+) Tot Debt Cap, LFI (m): 0.00

Short term target price: $27/share

Thesis:

The short term thesis is that IRMD is a medical device company that is poised to rerate and

return to its previous share price of around $27 to $28/share prior to the 2019 Q1 earnings

call. The more long term thesis is that this company is likely to be a billion dollar company if

it continues with its growth trajectory and keep adding MRI compatible medical devices to its

portfolio. However, the founder is likely to sell the company before that happens.

This is an interesting company because it has a combination of very attractive attributes that

I generally look for. It has a large address market, very high & expanding gross margin,

monopolistic for one product (MRidium Pump) and duopolistic for another product

(Monitoring system, only competitor in the USA is Philips Medical), an ambitious

management team that has a clear vision for the company. They were also clear to sell their

monitor in Japan in 2018 Q2 last year so that is going to add to growth as well. Also, there is

a short-term catalyst that would lift the stock back up again probably by 30/7/2019 and with

the high short interest right now (10% short percent of float), a short squeeze might be

imminent. It is also positioned as probably the only company that could provide a full fleet of

MRI compatible medical device in the future. Finally, it is only trading at 5.34x LTM EV/Rev,

has no debt, is both net income positive and generating a lot of cash and the insiders have a

significant stake in the company, Insider ownership: 54.87% (CEO owns 52%). Its products are

protected by patents.

Short term worries

The stock price fell from $28/share to $18/share because of a combination of factors.

i. First is the short term sales disruption in the EU with the monitor. Basically, there

was a CE marking issue with the MRI compatible patient vital signs monitor. I

believe that by this coming earnings call, the management team would have

already resolved the issue. The coming earnings call for 2019 Q2 is on 30/7/2019.

I am fairly confident that this is a short term issue that either has already been

resolved as of now, or would be resolved soon enough.

Regarding the impact of CE marking issue:

2018 Q4 CC

Date of publish: 24 July 2019

2. “And Larry, I think if you look at it, of course, Q1 is going to be greatly impacted

because -- more impacted than the rest of the year because that's when the issue

is affecting us in the CE Mark area. So we expect that to, as Roger said, mediate

in the second quarter. And so, yeah, I mean any effect of that you're looking at

front-end loaded, so that really, most of that is just the effect of that and

otherwise, would be a pretty balanced approached to the year.”

2019 Q1 CC

“Our full year and second quarter guidance includes the impact of the CE Mark

issue I just mentioned, which we believe will negatively impact the full calendar

year revenue by less than 2%”

“So at this point, we completely anticipate exactly what we announced back in

January, that before the end of Q2, we'll be shipping our monitors back into

Europe with the CE Mark restored.”

This has likely resulted in lower growth in 2019 Q1 as compared to 2018 Q1-Q4,

which could be one of the reasons that the market was upset with IRMD’s

performance

ii. The market does not understand the one time windfall IRMD due to bayer (as

pointed out by Mr Sergio Heiber)

Mr Segio Heiber is a specialist in microcap stocks and has been at it for a very long

time (~10 years), as such, I believe that his insights are much better than my own

and I decided to quote him directly and I recommend reading his article as he

covers IRMD from a totally different angle & is very insightful. I have provided the

link to his article below. He also covered extensively on the FDA warning letter that

IRMD got back in 2014.

Sergio’s article:

https://seekingalpha.com/article/4276476-iradimed-corporation-oversold-

monopoly

From our conversation

“People don't understand that IRMD had a one time windfall from Bayer dropping

out. IRMD scooped up the Bayer clients and then had a lapse in growth which now

exceeds anything in their history but the windfall created the slide in earnings and

is now proof that this company is hitting it right as revenues are at record levels.”

3. From his article on seeking alpha:

“The only competitor, Bayer (OTCPK:BAYRY) stopped production of its non-

magnetic MRI compatible device in 2012 and seized servicing existing systems in

2015 due to many recalls and FDA warnings. IRMD is enjoying a monopoly in its

product niche. No one else is offering non-magnetic MRI compatible medical

devices.”

Why is it mispriced?

I went to the stock message boards that I normally frequent only to find out that nobody has

talked about it, the last stock post on seeking alpha was done Mr Sergio Heiber a few days

ago, if not the last post was done by me 2 years ago. My guess is that this story remains

relatively unknown.

Business model & products

Basically, because the nature of how the MRI machine works (strong magnetic fields), lots of

medical equipment can’t be used along with it. The company capitalized on this fact and

started their own product lines that would be compatible with the MRI machine. The current

Product portfolio currently composed of:

i. MRidium IV Pump and accessories (FDA approved in 2005) and

ii. 3880 MR Patient Vital Signs Monitoring System and accessories (FDA approved in

October 2017).

Value proposition: IRMD’s products are necessary & crucial

Critically-ill patients cannot be removed from IV medications to undergo an MRI scan

Many patients, particularly children, require continuous sedation to remain immobile during

a scan. Many patients from critical care and those under sedation require continuous vital

signs monitoring.

Razor and blade model

IRMD is able to generate revenue through several ways

i. Sale of medical devices (Pump & Monitoring system)

ii. Recurring revenue from service contracts

iii. Sale of disposable products used with the devices

Actual products

I. MRidium IV Pump

The MRidium 3860+ is the only MRI compatible IV infusion pump system on the

market today. The patent for their infusion pump will last for ~10 years which means that

their core business is pretty much protected from the siege of other companies. Right now,

there is pretty much no real alternatives for this product. There are five general methods that

are used to deal with patients undergoing an MRI who require IV medications during their

imaging procedure. All of these approaches have drawbacks, introduce safety risks and may

4. result in deficient patient care. The 10k has a very detailed discussion on each of the risk of

the methods above. From what I understand from other investors in the medical field, IRMD

is truly the only player in this niche.

Alternatives to the Pump (Taken from 2018 10k)

• do not offer MRI treatment to patients requiring IV delivered medications or sedation;

• use standard (magnetic) pumps with long IV lines that extend outside the MRI scanner

room;

• proceed and accept patients for an MRI procedure but stop the flow of IV fluids during

the procedure;

• allow the gravity controlled free drip of IV fluids; and

• attempt to shield a conventional IV infusion pump.

II. Monitoring system

The monitoring system is also compatible with the MRI machine. Unlike the Pump, this

product has got some serious competitor. However, this doesn’t really matter and I will

explain why in detail.

In terms of technical superiority, IRMD’s monitor is compact and lightweight, overcoming

many of the workflow issues created by other larger and heavier MRI compatible monitors

currently in the market. Since the CEO invented the first monitoring system, I believe that he

knows of the flaws of the monitors sold by their competitors. The only competitor that is

selling similar product in the USA right now is Philips medical and it is through a company

called Invivo, and before IRMD entered the market, they were effectively a monopoly. Invivo

was founded by Roger Susi, the founder and CEO of IRMD. The original MRI compatible

patient monitoring system was also developed by Roger Susi.

In the 2019 Q2 CC, the CEO, Roger Susi also explained how they have been stealing market

share away from Philips.

“Q: When you look at the patient monitoring sales, are these new customers that haven't

had patient monitoring equipment before? Or are they orders that you're winning from the

competitor?

CEO: Larry, these are almost all replacement market products, right? I mean, this is a mature

market. This is a market that's behind these products for years and years. You have a pretty

low growth rate -- a bit of your growth rate is new MRI coming -- being sold in the market.

What our opportunity here, the market share play, obviously, and taking market share from

our competitors. So every one of these sales is competitive and every one of these deals,

we're really taking from our competitor, Philips Medical Systems, is basically the only one

that's actually selling in the U.S.”

To understand how effective they are at stealing market share away from Philips, I will just

let the numbers speak for itself.

5. The incumbent firm, Philips, did try to lower its prices and basically that is all that they ever

do. The CEO has addressed this matter pretty much every single conference call since 2018

Q1, and Philips is still doing the same thing, to little or no avail of course, and I feel that it is

pretty clear from the growth rate we are seeing. Also, the CEO stated that they did not have

to further discount the price of their monitor despite the incumbent firm’s attempt.

III. Bundling

So…This company sounds really good so far right? Here’s where it gets even better. While

speaking to their customers, the company realized that there is a possibility where they could

bundle up the 2 products that they have right now and sell it to the Intensive Care Unit (“ICU”),

Emergency Room (“ER”), and other critical care departments within the hospital where there

is a high probability that MRI procedures will need to be performed on patients. By doing so,

the number of MRI patient monitors and MRI IV pumps sold per scanner will increase resulting

in a larger overall market for these two devices.

To sum it up, this company’s technology is far superior to the existing incumbents and has

also been able to bundle them up into a total different product offering that no one else can

be in. Personally, I feel that this moat is pretty much impenetrable.

Near term expansion strategy

As mentioned above, in the past, the company used to only market their infusion pump to

the MRI departments of the hospitals. However, they are now focusing on a strategy called

critical care strategy where they market their products to the ICU and ER departments and

also to the radiology and anesthesiology departments. They are also expanding their sales

team quickly and is optimistic of higher sale in 2019.

6. Long term expansion strategy

Markets and distribution channels

IRMD sells its products both in the USA and internationally, I will go through each of them in

details.

i. US market

Since 2012, the company has been selling using direct sales in the USA. As of 2019 Q1 their

direct sales force consisted of 26 sales representatives, 3 regional sales directors and

supplemented by 5 clinical support representatives. Their plan for 2019 is to expand our U.S.

sales force to between 30 and 32 field sales representatives and 6 clinical support

representatives by the end of 2019. The company also has agreements with healthcare supply

contracting companies known as group purchasing organisations (GPOs). This enables them

to sell and distribute IRMD’s products to their member hospitals. IRMD typically pay a fee of

3% of the sales of our products to their member hospitals. IRMD’s current GPO contracts gives

them the ability to sell to more than 95% of all U.S. hospitals and acute care facilities.

7. According to Mordor intelligence, the North American MRI systems market is estimated to

increase from the current $1.38 billion in 2016 to $1.63 billion by 2021 with a CAGR of 2.9%

between 2016 and 2021.

ii. International market (japan in particular)

The company has distribution agreements with independent distributors in order to sell their

products in the international market. A majority of our international sales originate from

Europe and Japan, and but they also sell also in Canada, Hong Kong, Australia, Mexico and

certain parts of the Middle East. The most notable international market right now is the

Japanese market as they just received clearance to sell their patient monitor in Japan in 2018

Q2. This essentially opens up 2 market segments for them in Japan; the monitor market & the

bundled products market. They did not mention how big the market in Japan is, but the

increase in international sales should probably be attributed to sales in japan.

With regards to the Japanese market, these are the comments from the management team

in the 2018 Q3 CC.

“From the regulatory standpoint, as announced in September, we received clearance to

begin sales and importation of our patient monitor to Japan. This is a very important event

for us as Japan is a strong and growing market, and since receiving this clearance, we have

already received a sizable monitor system order…

Japan is a new market for it us, it's a new market on the patient monitor, the established

market for us on pumps. And we're pretty well established in most significant countries in

the world with distribution, I am hiring more sales managers on that side of the business to

help drive the business with those distributors…

How many? There's the - I guess we can do by comparison, they're moving by way of having

thousands of just MRI pulse oximeters located in their MRI systems to where now the

recommendations are to have multiparameter units. So there's a void there of several

thousand monitors that should be filled. How fast? It's probably - right now it's looking like

it's just starting to take hold, it's on the order of a couple of hundred per year.”

According to Mordor intelligence, the Japanese diagnostic imaging market (which consists of

MRI machines) is expected to register a CAGR of 6.8% during the forecast period of 2018–

2023. MRI is anticipated to dominate the market during the forecast period owing to the

growing application of MRI in diagnosis. So, in addition to the existing void in the current

market (as explained above), there is also a pretty strong tailwind in Japan.

8. Product segmentation

Why did infusion pump revenue go down in 2017

The decrease in infusion pump revenue from 2016 Q3 to 2017 Q3 is because they were trying

to finish up backlog work from previous years, stabilize the revenue and begin using a new

sales strategy. So it is really a strategic decision rather than a slow down in growth. The reason

for doing so is so that they can establish their multi pump strategy (which, if I understand

correctly refers to selling multiple pumps together instead of selling one at a time).

The CEO stated this during the 2016 Q2 CC

“the multi pump sales have kicked off of seven, eight months ago. We started to really move

the sales force into – instead of just going into radiology and trying to selling that one pump

per MRI machine, slow down a bit and cover the ancillary department…If you understand,

we talked always about having the multiplier that where it’s more than one pump for MRI

scanner and we want to keep that ratio moving northward and eight months ago we really

put a strategy in our sales team to go after that.”

9. Valuation:

Based on the sector comparables taken from reuters.

IRMD’s valuation seems fair on the surface, but given that it is likely to growth rate (projected

26% to 28% revenue growth according to management estimate) is much higher than the

medical equipment industry in the USA and globally, it should be valued at a much higher

valuation. According to Evaluate Ltd, the medtech industry is projected to grow at a

compound annual rate of 5.6% worldwide from 2017 through 2024, reaching $595 billion.

While the U.S. medical device manufacturers market size was valued at USD 154.0 billion in

2017 and is anticipated to exhibit a CAGR of 5.0% over the forecast period (2019 to 2025),

according to Grand View Research. Thus, a rerating might be imminent, even if it doesn’t, the

long term trajectory still looks very attractive.

*word of caution: management’s estimates might be a little too optimistic.

Using management team’s predictions

Base case

Rerating occurs. The valuation below is done by assuming that revenue in 2018 (30.44 mil)

increases by 26% in FY 2019. Also, cash, debt and etc remains constant.

10. Bluesky

In the investor’s presentation, it is stated that the unconstrained addressable market is $4.6bil

and they also eluded to the fact that it could be much higher in the future.

While this is possible, it might be a little too optimistic as it assumes that there is no

executional mishap. However, their only real constraint is the speed at which the distributors

and sales force in the company could sell the products, and while the addressable market

might be too optimistic, I believe that the growth rate certainly is not. As such, I’ve modelled

that Rev would grow at 26% and assume that no rerating happens.

Worse case

I don’t really see a scenario where this fails to take off in the long run, but in the near term it

might fail to rerate. Although pump sales growth might be levelling off as evident from the 7%

growth in FY2018. I don’t believe this to be a big issue as growth in monitor sales is catching

up to it.

11. Catalyst:

i. Rerating once the temporarily issue surround the CE marking is resolved

ii. Continued growth of the company through organic growth, new product offering

and acquisition of compatible companies.

iii. Sale of the company. The motivations of the founder is pretty obvious, he is going

to transform this company into a full fleet MRI compatible medical device

company. Roger Susi, the founder, has not sold a single share since 2015, even

when the stock price reached as high as $37/share. I have not met him personally,

so I have to rely on secondary accounts of how he is like.

I took this excerpt from valueinvestorsclub by member mm202:

“The founder/owner of 60% of the stock is a smart guy, I've met with him a

couple of times and I thought he was legit. He has a history of selling his

companies before and he was pretty clear that his goal is to sell this company in

the intermediate term.”

Risks:

i. Overly optimistic projections, especially in the investors presentation

ii. Insiders have sold at the 28/share range (just 1 person recently), but notably CEO

hasn’t sold at all since 2015 which is aligned with what mm202 from

valueinvestorsclub claimed.

iii. FDA warning letter in 2014

Mr Sergio Heiber covered extensively on this topic, so I would recommend reading

his article instead, but if you’re just looking to have a brief understanding of the

situation, I’ve quoted his article below.

Mr Sergio heiber:

“The company received a warning letter from the FDA in 2014 pursuant to a

routine inspection that identified eight areas of concern. IRMD has worked with

the FDA and incrementally resumed sales where the FDA had cited issues. The

warning letter has not been closed, which means that there will be another

inspection to determine if all issues have been resolved and if there are any new

issues.

While the E.U. setback appears to be minor and only temporary, the FDA

warning letter is potentially more problematic. IRMD has experienced an FDA

product recall in 2012, a voluntary recall in 2013 and appears to have complied

with FDA requirements as there are no sales restrictions on any of their products

at this time.”