Di 4 pro

•

0 likes•155 views

Control & enjoy strong income -even in event of disability. Group disability is cheap but pays out too little. If you can qualify, here's what you want professional Disability insurance to do for you. >>> See also at Amazon, "A Lifetime Of Wealth -- And How Not To Lose It"

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Di 4 pro

Similar to Di 4 pro (20)

More from Brian Weatherdon

More from Brian Weatherdon (10)

Recently uploaded

Recently uploaded (20)

Di 4 pro

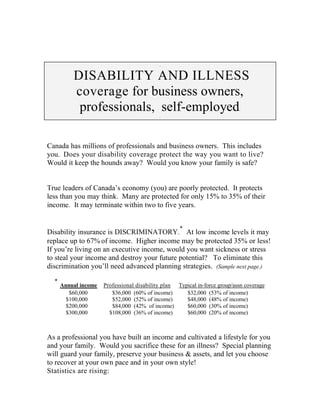

- 1. . DISABILITY AND ILLNESS coverage for business owners, professionals, self-employed . . Canada has millions of professionals and business owners. This includes you. Does your disability coverage protect the way you want to live? Would it keep the hounds away? Would you know your family is safe? True leaders of Canada’s economy (you) are poorly protected. It protects less than you may think. Many are protected for only 15% to 35% of their income. It may terminate within two to five years. * Disability insurance is DISCRIMINATORY. At low income levels it may replace up to 67% of income. Higher income may be protected 35% or less! If you’re living on an executive income, would you want sickness or stress to steal your income and destroy your future potential? To eliminate this discrimination you’ll need advanced planning strategies. (Sample next page.) * Annual income Professional disability plan Typical in-force group/assn coverage $60,000 $36,000 (60% of income) $32,000 (53% of income) $100,000 $52,000 (52% of income) $48,000 (48% of income) $200,000 $84,000 (42% of income) $60,000 (30% of income) $300,000 $108,000 (36% of income) $60,000 (20% of income) As a professional you have built an income and cultivated a lifestyle for you and your family. Would you sacrifice these for an illness? Special planning will guard your family, preserve your business & assets, and let you choose to recover at your own pace and in your own style! Statistics are rising:

- 2. § One out of three are disabled during their working years. § One out of nine are disabled permanently & won’t return to work. § One out of two get illnesses which threaten business or other assets. X Group or assocation coverage based on income $100,000/year. Disability coverage near $48,000 tax-free per annum. Cost rises. § pays after consecutive days of disability § pays if disability prevents all job-related duties § pays for 2-years if you cannot do your present job § pays to age 65 if you cannot perform any job § stops if you return to work part-time § sick mindset – you must keep proving total disability § obligates you to rehabilitation, regardless how suitable to you ü For you as a Professional, based on $100,000/year. Disability coverage: $52,000 tax-free per annum. Cost stays level. § pays after accumulated days of disability § pays to age 65 even if you take alternative work § pays you if partially or proportionately disabled § continues compensation during a trial-return to work § continues cash-flow benefit for 2 months after returning to work § voluntary participation in work rehab programs if you are willing § guarantees you can bump up your dis. plan even if you are disabled § invests extra $1500/month into a retirement trust for your later security § covers $5000/m for your existing/ongoing business expenses/contracts § pays a lump-sum $250,000 at diagnosis of a life-threatening illness § 50% to 75% of your total cost is refundable to you at age 55 or age 65 What is your lifestyle worth? People get ill. Disabilities happen. Surviving is a plus. But more important: still being able to protect your lifestyle, and manage your business interests and other investments, and protecting your family: what are these worth to you? Brian Brian Weatherdon, BA, MA, CFP, CLU, MDRT (905) 637-3500 x 223 www.sovereignwealth.ca . brian@sovereignwealth.ca