Downloaded 631 times

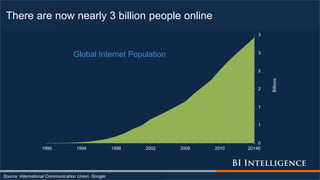

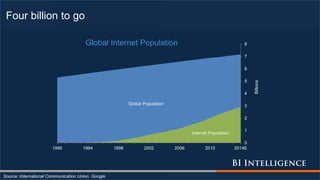

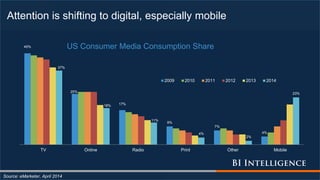

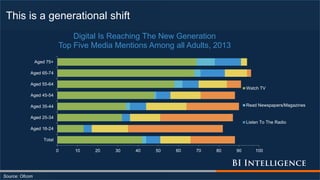

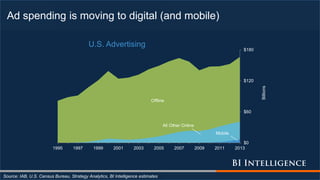

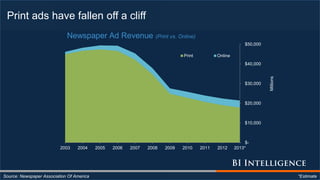

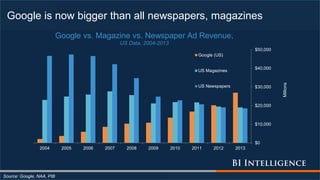

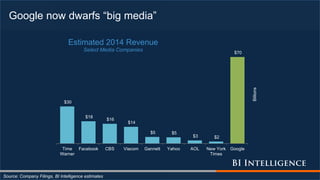

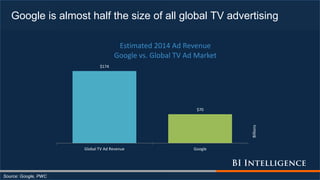

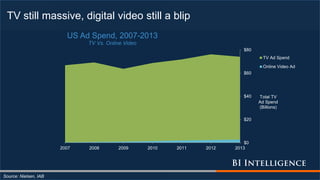

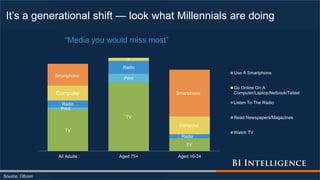

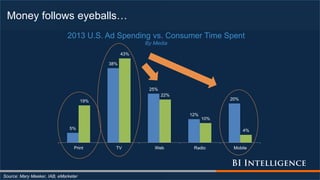

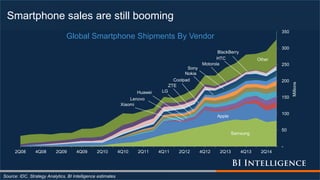

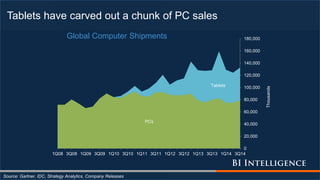

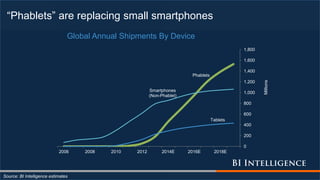

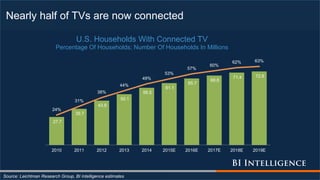

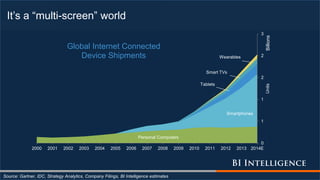

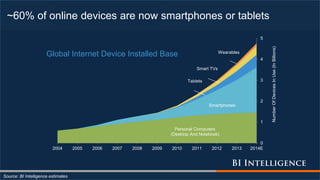

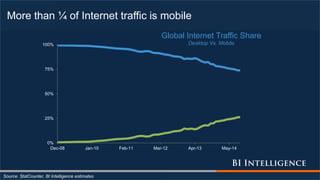

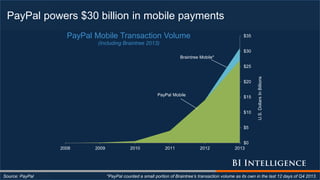

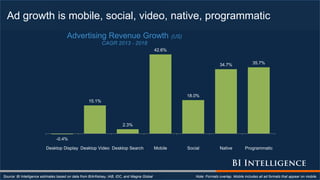

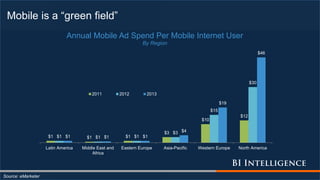

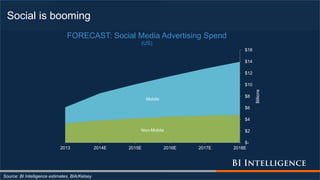

The document discusses the rapid shift in media consumption from traditional outlets to digital platforms, especially mobile, highlighting how nearly 3 billion people are online. It details significant changes in advertising spend, with digital and mobile ad revenues growing, while print and television ad revenues decline. The document also emphasizes the importance of adapting to new technologies and trends, such as smartphone use and connected devices, to remain competitive in the evolving media landscape.

![5G Explained! A High Level Overview [Introduction]](https://cdn.slidesharecdn.com/ss_thumbnails/5gexplainedahighleveloverview-260119165306-cc137a3e-thumbnail.jpg?width=640&height=640&fit=bounds)